Click on the images to view our comments on each topic.

Switzerland

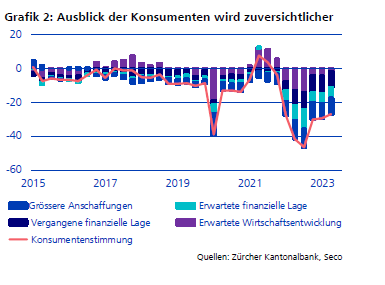

Cautious consumers

After a buoyant start to the year, the Swiss economy stagnated in the 2nd quarter. Private consumption again grew solidly and the service sector expanded on a broad basis. By contrast, investment and value added in the industrial sector declined. This is where the weakening of the economy in the euro zone is making itself felt. The mood of consumers in Switzerland is optimistic and the situation on the labor market is still very good and the unemployment rate at 2% except neatly low.

The low inflation rate has facilitated the decision of the SNB and removed pressure to act from the SNB. It decided at the September meeting to leave the key interest rate at 1.75%. An interest rate move in December is conceivable, because although inflation is within the target range of between 0.00% and 2.00%, inflation has not yet been defeated. The strong Swiss franc helps to keep imported inflation low.

SECO Economic Forecast

GDP 2023: +1.30% (E)

Inflation 2023: +2.20% (E)

SNB Key Interest Rate: +1.75%

Our conclusion:

According to SECO forecasts, GDP will grow by 1.30% this year after all. The local companies are well positioned to compete internationally. The Swiss stock market has so far underperformed other markets. In the current tense environment, the defensive orientation with heavyweights in the pharmaceutical and food sectors could once again become the focus of international investors. Corporate earnings expectations remain high and valuations are modest by international standards, which is why we view the Swiss equity market as attractive.

Sources: SECO, ZKB, IMF

As of 09/25/2023

European Union

Slowing Growth Momentum with Falling Inflation

Gross Domestic Product (GDP) in the Eurozone increased by 0.30% in the second quarter of 2023 compared to the previous quarter, according to Eurostat estimates, and remained unchanged in the EU. In the first quarter, GDP had increased by 0.20% in the Eurozone and remained unchanged in the EU.

In the labor market, the positive situation has continued and the unemployment rate remains at the all-time low in many places. Within the EU, the average unemployment rate in July 2023 was 5.90%, while in the eurozone it was 6.90%.

The annual inflation rate in the euro area fell to 5.20% in August 2023, down from 5.30% in July. A year earlier, it had been 9.10%. In the European Union, it was 5.90% in August 2023, down from 6.10% in July, and still well above the ECB's target of 2.00%. While the downward pressure of energy prices eased slightly, the momentum of food prices continued to decline. Core inflation also declined slightly for the first time in a while (from 5.50% to 5.30%).

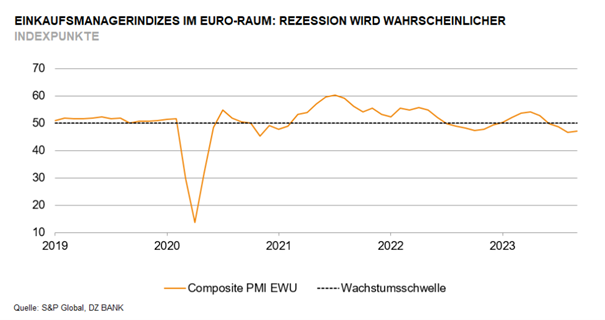

Due to the ongoing decline in demand, the eurozone economy continues to contract. After 46.7 points in August, the HCOB services index Eurozone in September increased slightly to 47.1 points, but well below the growth threshold of 50 points. The key factor was again the industrial sector, but the service sector also declined for the second time in a row, with new orders having been falling for three months. On the positive side, slightly more staff were hired in September than in August. Job growth is continuing, but it was weak given overcapacity and the less optimistic business outlook.

The eurozone's two largest economies, Germany and France, are mainly responsible for the fact that economic output also fell in September. Germany's economy declined for the third month in a row in September and France is in crisis. Economic output there contracted at the fastest rate since November 2020.

Inflation2023 +5.60% (E)

Current 3 Month Libor +3.96%

GDP Growth 2023 +0.80% (E)

Our conclusion:

In the EU, economic activity has been subdued in the first half of 2023. The economy continues to grow, but at a slower pace.

The conclusion from the current surveys is that the order situation is uniformly assessed as weak and declining. This is mainly due to the continued weakness of the industrial sector and the slowing momentum in the service sector - despite the successful tourism season in many parts of Europe. Since August, sentiment among service providers has unexpectedly weakened significantly.

An economic turnaround is currently not in sight in Europe in view of a weakening global economy and declining demand. In the third and fourth quarters, a slight decline in economic output is emerging, making a mild recession increasingly likely

The European Commission has lowered expectations in its summer forecast compared with the spring forecast. For 2023, it now expects economic growth in the EU of 0.80% (spring: 1.00%) and for 2024 growth of 1.40% (spring: 1.70%). Growth forecasts within the Eurozone have been lowered to 0.80% for 2023 (previously 1.10%) and to 1.30% for 2024 (previously 1.60%).

In September, the ECB raised interest rates for the tenth consecutive time since July 2022. The Governing Council decided to raise the ECB's three key interest rates by 25 basis points each. The central key rate for main refinancing rates thus rose to 4.50%. Despite persistently high inflation, we do not expect the ECB to raise interest rates further in the coming months due to falling leading indicators. Interest rates are likely to have peaked.

Inflation continues to fall, and ECB experts expect average inflation in the eurozone to be 5.60% in 2023, 3.20% in 2024 and 2.10% in 2025. This represents an upward correction for 2023 and 2024 and a downward correction for 2025. The upward revision for 2023 and 2024 primarily reflects a higher level of energy prices. Excluding energy and food, they have revised their forecast down slightly to 5.10% for 2023, 2.90% for 2024, and 2.20% for 2025. The ECB's rate hikes to date continue to have a strong impact.

Based on the outlook for the European economy, we remain confident in the European equity market.

Daniel Beck, Member of the Executive Board

Sources: European Commission, Statista, HCOB, S&P Global, DZ Bank

As of Sept. 25, 2023

.

United Kingdom

USA

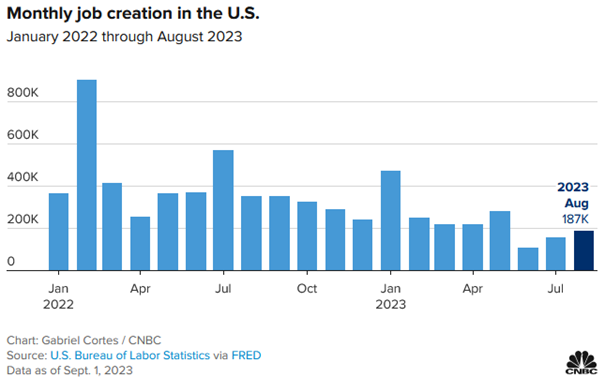

The labor market is cooling

According to the preliminary S&P Global Flash U.S. Composite PMI, this leading economic index falls slightly in September compared to August, from 50.2 to 50.1 points. Interestingly, the services sub-index falls from 50.5 to 50.2 month-on-month, while the trade sub-index rises from 47.9 to 48.9. Thus, the overall index is holding above the expansion threshold of 50 and the sub-index for trade is approaching this threshold again, which is positive.

Inflation rose again in August to 3.70% (July 3.20%). This is mainly because of higher energy prices. In contrast, the core rate (excluding energy and food), which is keenly watched by the Fed, fell to 4.30% in August (July 4.70%). Wage growth weakened to +0.20% in August (+4.30% annualized).

The labor market in the U.S. is slowly starting to respond to higher interest rates. For example, although the number of new nonfarm jobs created rose again in August to 187,000, this is well below the average of 271,000 jobs added over the past 12 months. In addition, new jobs created for June (from 185,000 to 105,000) and July (from 187,000 to 157,000) were revised significantly downward. The unemployment rate rose to 3.80% in August (July 3.50%, +514,000 to 6.40 million unemployed). Job openings also fell by 338,000 to 8.827 million in August from the previous month.

At the Sept. 20, 2023 meeting, the Fed paused again and left the target range for the Fed Fund Rate at 5.25 - 5.50%. However, since the interest rate forecasts (so-called 'dot plot') of the FOMC members still signal a rate hike of 0.25% by the end of the year, there is also talk of a hawkish pause here. For end of 2024, the FMOC members forecast an interest rate of 5.10%. The first interest rate cuts are now expected only for the 3rd quarter of 2024.

For the third quarter of 2023, according to Factset, analysts expect an average decline in profits of the companies represented in the S&P 500 Index of 'only' -0.20%. At the same time, 8 out of 11 sectors are expected to report earnings growth. Based on earnings estimates for the next 12 months, the S&P 500 Index reaches a price/earnings ratio of 18, just 4.00% below the 5-year average and just 3.00% above the 10-year average.

Gross Domestic Product grew 2.10% in the second quarter of 2023 according to the second reading. For the third quarter, it is expected to be as high as 4.80%, according to the Federal Reserve Bank of Atlanta's real-time GDPNow estimation model released Sept. 19.

The U.S. Congress once again appears to be failing to pass the 2023/2024 budget on time by the end of September. A partial shutdown of administrative activities is therefore foreseeable. However, the effect on the economy will only be temporary and will even be made up for later.

GDP 2023(IMF): +1.80% (E)

Inflation 2023(IMF): +4.50% (E)

Fed Fund Rate: +5.50%

Our conclusion:

The higher interest rate level provides as wanted by the Fed for economic headwinds and the labor market is starting to cool. On the other hand, however, the trillion-dollar post-pandemic fiscal packages are still having a supportive effect on the economy, and wage increases are maintaining consumer purchasing power. Further (slightly) falling inflation rates and rising corporate profits will positively influence the stock price development of the broad market as well.

Sources: Markit Economics, IMF World Economic Outlook September 2023, FactSet, Gabriel Cortes / CNBC FMOC

As of Sept. 25, 2023

.

China

Shaky real estate investors

China released August data on industrial activity, lending, inflation and trade in recent weeks. These improved slightly and were broadly better than the market expected. Inventories appear to be stabilizing, while fiscal stimulus through the issuance of special local government bonds (LGSBs) is increasing. At the same time, the summer travel season has helped to boost consumption. Overall, increasing policy support seems to be leading to a stabilization of economic data and maintaining hope that the economy is past the worst. Still, the real estate sector is not out of the woods yet. In August, payment difficulties at the country's largest real estate developer, Country Garden, fueled fears of a pending real estate and financial crisis in China. While there has been some recovery in property sales in individual cities since the easing of mortgage policy, this recovery is largely due to pent-up demand and is concentrated in the secondary rather than the primary market. Home prices declined in 66 of 70 cities in August.

IMF Economic Forecast

GDP 2023: +5.20% (E)

Inflation 2023: +2.00% (E)

3 Month Shibor: +2.26% (E)

Our conclusion:

We continue to expect a gradual announcement of policy support and stimulus, with targeted and measured resources mobilized. This should help prevent a further downturn in the economy, but there will also be no quick V-shaped recovery. Market confidence remains low and equity market volatility will persist until more concrete government support measures are implemented and have a positive impact on economic data. The current situation is too uncertain for equity investments.

Sources: Allianz, ZKB, IMF

As of 09/25/2023

Japan

Japanese stock market is getting more investor focus

The Japanese stock market was very popular in 2023. This is the first time since 2017 that we have seen higher inflows than into the Chinese stock market.

This year's rally in Japanese equities is due to the development of fundamental investment arguments. The macroeconomic outlook is positive for Japan. The country has finally emerged from deflation. Wage growth and the overcoming of deflation are having a positive impact on consumption and investment in the country. As mentioned in previous commentaries this year, company valuations have not risen proportionally with earnings growth, and we can talk about an undervaluation of equities. Japan is also characterized by an export-oriented industry, which is focused on technologies. This industry is further supported by the weak yen. However, it should be noted here that the Japanese central bank has announced a monetary policy review, which may take more than a year. Thus, we still have a negative interest rate in Japan at the moment. Last but not least, most companies benefit from high net liquidity, which is much higher than in comparable countries.

GDP 2023: +1.30%(E)

Inflation 2023: +2.70%(E)

3 Month Tona Rate: -0.03% m

Our conclusion: still positive

Japan is still undervalued, cheap and underrepresented in globally focused portfolios. The market offers a good opportunity for medium-term investors. Even if the potential is lower than at the beginning of 2023.

Mimi Haas, Lic.rer.pol. HSG, M.A. in Banking and Finance HSG, Partner

Sources: F&W, JP Morgan, Bloomberg

As of Sept. 25, 2023

.

Emerging Markets

Constrained economic development

After a good start to the year, growth lost momentum in the 2nd quarter. Restrictive financing conditions are hampering industrial companies' willingness to invest. Capital has also become more expensive for households, so that interest payments are increasingly weighing on the household budget. On a positive note, inflation is falling and some central banks in Latin America, for example Chile and Brazil, have cut key interest rates for the first time in three years. In Asia, policy rates have not been raised as dramatically in the past, so central banks have not yet changed rates.

Our Conclusion:

The economic outlook for emerging markets in South America and Asia is improving. The situation in Eastern Europe remains subdued. Equity market valuations are rather low, reflecting the current uncertainties due to the geopolitical situation in Ukraine as well as in China and Taiwan.

Sources: IMF, ZKB

As of Sept. 25, 2023

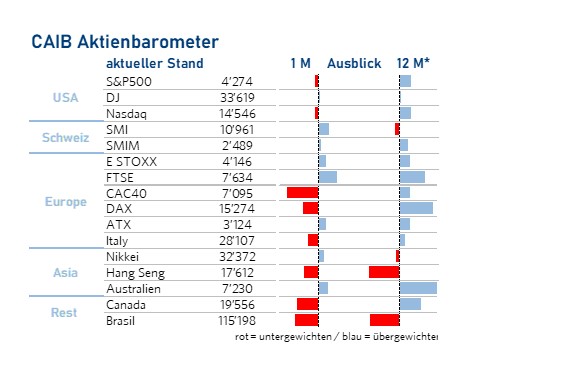

Stocks

State of Mind

Last week, the Federal Reserve more than doubled its forecast for U.S. economic growth in 2023 and also raised it for 2024. These upward revisions to the U.S. forecast were accompanied by downward revisions for China, so the global economy still isn't growing faster overall. Now that the U.S. has reached a record high with over 60% of the world's traded market capitalization, investors are asking themselves the question of sustainable performance in the future. The high relative valuations of U.S. companies on average (about a PE of 18) require above-average earnings growth internationally to justify their current valuation premium over non-U.S. equities.

To achieve this, it required an overall high level of innovation, continuously improving cost efficiency, and a multiplier effect. Here, the U.S. markets have a weighty advantage over Europe in the composition: for example, the share of highly innovative information technology in the U.S. market is about 28% compared to 6.70% in Europe (based on MSCI Europe). In addition to innovation, the U.S. also scores with the implementation of digitalization and automation: thanks to the deeper personal and data protection laws than in Europe. Therefore an efficiency advantages can be created for US Companies. Also, the asymmetric risk appetite of Europeans compared to U.S. companies, leads to a higher focus on risk than on profit in Europe. Thus, it seems unlikely that European but also Asian companies will suddenly show similar growth to their US counterparts.

On second look, we see favorable equity valuations in Europe and Asia, based on lower expectations. Especially when the Fed has peaked interest rates and a decline is imminent, this is a signal for the other central banks to take their foot off the "interest rate pedal".

Due to more traditional business models and coststructures, European companies than in particular are likely to be favored and potentially achieve higher returns. The companies that have been able to improve their efficiency in recent years will have the best opportunities for share profit. Citibank'srecently published observation also points in this direction: A selection was made of companies that were profitable in 2022 and expect EPS growth of 20% ormore in 2023 and 2024.76 Large cap companies were found worldwide that met these criteria. Of these, 46% were US companies. Surprisingly, the performance of the 10 fastest growing non-US companies exceeded that of the fastest growing US top 10 companies. Is the widespread bullishness for US equities not entirely true after all?

Our conclusion: buy selectively

Although higher short-term interest rates offer a good alternative to equity investments, we are again somewhat more positive than we were in our last publication. True, our CAIB index is negative in the short term at -0.03. But in the long term with 0.07 it shows a higher opportunity plus. We maintain our overweight in European equities. At the sector level, we favor companies in retail, hotels, oil equipment& services, soft drinks, reinsurance.

Sources: S&P, Citigroup, MarketMap, IMF, and Chefinvest

As of 09/25/2023

.

Interest

Government bonds

The nominal yield on global government bonds rose again in July and early August, driven largely by real interest rates and surprisingly solid economic data. Although we now expect a soft landing for the U.S. economy, growth is still likely to slow in the coming quarters as tighter lending and financing conditions begin to impact economic activity. Moreover, the expected persistence of inflation suggests that the central bank rate hike cycle is coming to an end.

Our conclusion: We are positive on global government bonds.

Investment grade (IG)

The rise in global IG bonds was supported by surprisingly good economic data. Spreads tightened to expensive levels while yields remained attractive. In our soft- landing scenario, global IG bonds should offer attractive returns going forward as economic growth and inflation slow while yields have settled at elevated levels.

Our conclusion: We remain positive on investment grade (IG) bonds and favor bonds with a good credit rating.

High yield bonds (HY)

We continue to expect returns like money market assets. Default risk on HY bonds has increased with market developments and there is a risk of further rating downgrades. The higher coupons do not compensate for this additional risk.

Our conclusion: We continue to recommend avoiding this segment in the coming months.

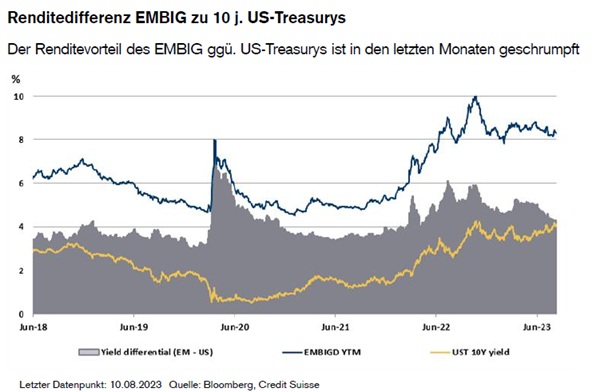

Emerging Markets bonds (EM)

EM offer a yield premium for higher default and currency risk. As a result of robust U.S. economic data, hard currency emerging market bonds posted another positive performance in July. However, the rise in U.S. Treasury yields, disappointing economic data from China and spread widening in August erased these gains.

Our conclusion: That is why we are neutral on this subclass in bonds.

Mimi Haas, Lic.rer.pol. HSG, M.A. in Banking and Finance HSG, Partner

Sources: MarketMap, Bloomberg and F&W

As of Sept. 25, 2023

.

Currencies

Inflation, interest rates and impact on the markets

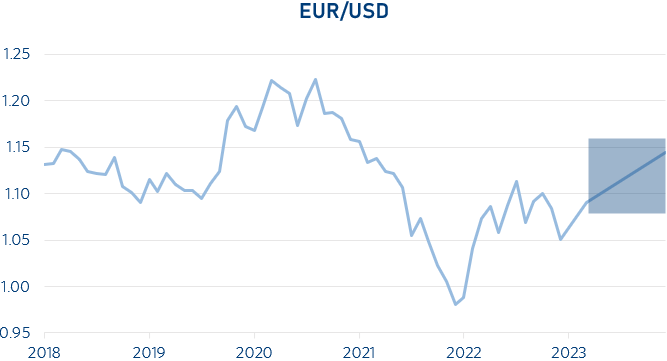

EUR/USD (09/29/2023: 1.055)

The movement of the currency pair was very volatile in 2023. Currently, we are just at 1.055, almost the same exchange rate as at the beginning of the year. Central to the further development of the currency pair is how the interest rate differential shapes up over the next few months.

Our conclusion: We expect the currency pair to move sideways.

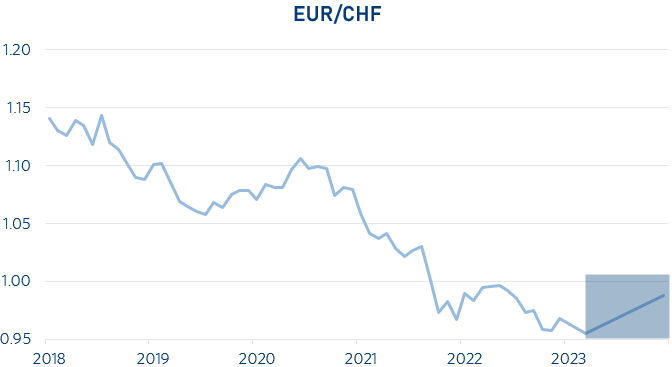

EUR/CHF (09/29/2023: 0.968)

The swiss franc has beaten all leading currencies in 2023. The main reason for this is the SNB's restrictive monetary policy. The Swiss central bank uses this, to prevent that the much higher inflation from abroad, via imports, comes into Switzerland. It has succeeded well in this, as Switzerland has the lowest inflation in the world with the current inflation of 1.60%. The country was able to stop inflation the fastest. The SNB will keep the interest rate differential large to keep the franc stable.

Our conclusion: We continue to expect a positive impulse for the CHF.

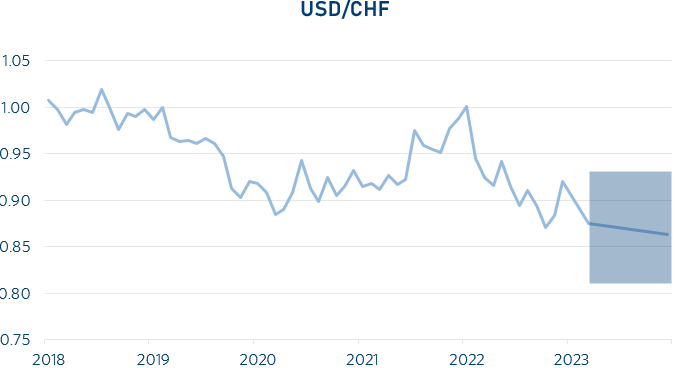

USD/CHF (09/29/2023: 0.915)

The interest rate differential of the two currencies is huge, both central banks decided in September not to raise interest rates. The central question is who will be the first to lower interest rates again. The U.S. has an advantage, the economy is doing better than abroad, they have greater scope to lower interest rates, the key question is when this will happen.

Our conclusion: We expect a sideways movement of the USD against the CHF.

Mimi Haas, Lic.rer.pol. HSG, M.A. in Banking and Finance HSG, Partner

Sources: F&W, Market Map and Bloomberg

As of Sept. 27, 2023

.

Oil

The Oil suppply remains curbed

The reduction of production quotas of OPEC+ (mainly Saudi Arabia and Russia) of 1.3 million barrels of oil per day and speculative long positions have driven the WTI oil price to 90 USD per barrel. This has already impacted US inflation in August (see commentary USA). Despite the lull in demand from China, there is a gap in supply: According to the IEA forecast, global demand reaches 102.20 million barrels per day and supply only 100.90 million barrels per day. A price above USD 100 would give inflation a boost again. It would be unwise for OPEC+ to allow prices to rise further, as the resulting provoked weakness in demand could eventually put massive pressure on prices again.

Our conclusion:

We expect WTI oil to move in a new range with prices between $80.00 and $100.00 per barrel.

Sources: F&W, MarketMap, International Energy Agency (IEA)

As of Sept. 25, 2023

.

Precious Metals

Gold benefits from central bank demand, platinum from undersupply

Gold prices (at USD 1,915/oz. on 9/26/2023) as well as platinum prices (at USD 911/oz. on 9/26/2023) are weakening due to the currently stronger US dollar and yield increases in fixed-income investments. In parallel, demand for gold from central banks has increased, especially from China, which wants to increase its gold reserves over the coming years. Demand for platinum in the auto sector continues to rise, leading to an undersupply and shortage of about 16% so far. The prospects for 2024 on lower U.S. interest rates and an associated weaker U.S. dollar, support the price of platinum.

Our conclusion: Neutral

Continued rising demand and expected interest rate cuts give the precious metals buoyancy and potential for rising prices. Thus, gold as well as platinum should continue to be booked in portfolios for diversification.

Andreas Betschart, Business Manager

Sources: UBS, ZKB

as of 09/25/2023

Abbreviations and explanations

bbl: 1 Barrell = 158,987294928 Litre

Bp: Basis points

GDP: Gross domestic products

BIZ: the Bank for International Settlements is an international financial organization. Membership is reserved for central banks or similar institutions.

EM-Bonds: Emerging market bonds. An emerging market is a country that is traditionally still counted as a developing country but no longer has its typical characteristics.

HY-Bonds: Fixed-income securities of poorer credit quality. They are rated BB+ or worse by the rating agencies.

IG-Bonds: Investment grade bonds are all bonds with a good to very good credit rating (Ra-ting). The investment grade range is defined as the rating classes AAA to BBB-.

IHS Markit: Listed data information services company

IWF: The International Monetary Fund (also known as the International Monetary Fund) is a legally, organiza-tionally, and financially independent specialized agency of the United Nations headquartered in the United States of America.

KOF: Business Cycle Research Centre at ETH Zurich

LIBOR: London Interbank Offered Rate is a reference interest rate determined in London on all banking days under certain conditions, which is used, among other things, as the basis for calculating the interest rate on loans.

OPEC: Organization of the Petroleum Exporting Countries

OPEC+: Cooperation with non-OPEC countries such as Russia, Kazakhstan, Mexico and Oman.

oz: the troy ounce is used for precious metals as a unit of measurement and is equal to 31.1034768 grams

Saron: The Swiss Average Rate Overnight is a reference interest rate for the Swiss franc

Seco: Swiss State Secretariat for Economic Affairs

Spread: Difference between two comparable economic variables

WTI: West Texas Intermediate. High-quality US crude oil grade with a low sulfur content.

Disclaimer:

The information and opinions have been produced by Chefinvest AG and are subject to change. The report is published for information purposes only and is neither an offer nor a solicitation to buy or sell any securities or a specific trading strategy in any jurisdiction. It has been prepared without regard to the objectives, financial situations or needs of any particular investor. Although the information is derived from sources that Chefinvest AG believes to be reliable, no representation is made that such information is accurate or complete. Chefinvest AG does not assume any liability for losses resulting from the use of this report. The prices and values of the investments described and the returns that may be received will fluctuate, rise or fall. Nothing in this report is legal, accounting or tax advice or a representation that any investment or strategy is appropriate to personal circumstances or a personal recommendation for specific investors. Foreign exchange rates and foreign currencies may adversely affect value, price or yield. Investments in emerging markets are speculative and involve considerably greater risk than investments in established markets. The risks are not necessarily limited to: Political and economic risks, as well as credit, currency and market risks. Chefinvest AG recommends investors to make an independent assessment of the specific financial risks as well as the legal, credit, tax and accounting consequences. Neither this document nor a copy of it may be sent in the United States and/or in Japan and they may not be handed over or shown to any American citizen. This document may not be reproduced in whole or in part without the permission of Chefinvest AG.