Click on the images to view our comments on each topic.

Switzerland

No recession

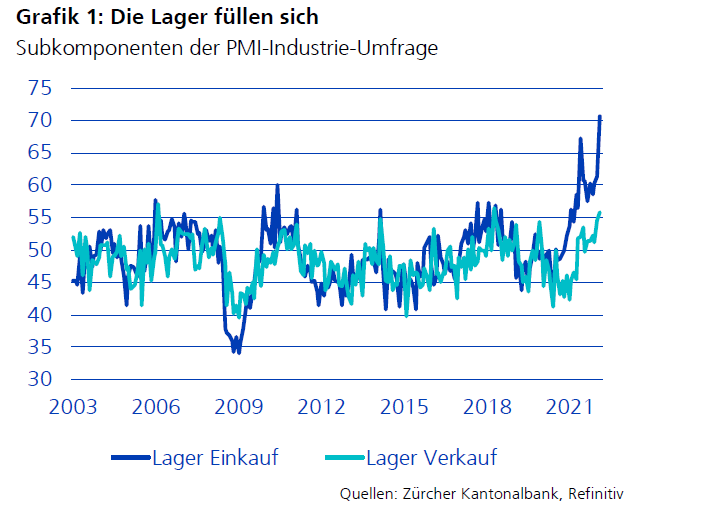

At first glance, the geopolitical uncertainties did little to harm the Swiss economy. Many companies are producing at the limits of their capacity and the demand for labour remains high. However, according to the latest SECO survey, consumer sentiment has clouded over considerably. Households assess their future financial situation as difficult, as they are burdened by higher prices. An export slowdown expected by most economists also now seems to be materialising; industrial companies' purchasing volumes are falling and inventories are increasing. Consequently, production could decline in the coming months. SECO is lowering its growth forecast significantly to 2%. Provided an energy crisis can be averted in the coming winter, however, a recession still seems unlikely. One important reason for this is that the labour market is extremely robust. Unemployment has continued to fall and immigration has risen again to record levels, which is supporting domestic demand.

SECO Economic Forecast

GDP 2022 +2.0%

Inflation +3%

SARON 3 mt. 0.50%

Source: Seco and ZKB

Our conclusion: Swiss companies are increasingly passing on the price increases and are thus able to maintain profit margins. SMI shares are currently trading below the historical average price and offer long-term potential. With inflation rates above the SNB's targeted inflation band for an extended period of time, the rate hike cycle is likely to continue even after the recent sharp rate hike of 0.75%, which will unsettle the equity markets. Volatility will remain high.

European Union

High inflation with lower growth

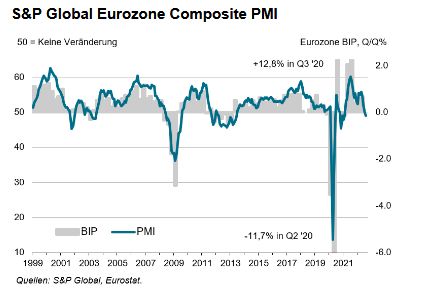

In the second quarter of 2022, the euro area economy grew surprisingly strong by 0.8%. This was mainly due to high consumer spending on services, as well as investment and the increase in travel following the lifting of pandemic-related restrictions, which particularly benefited countries with a significant tourism sector. However, persistent supply bottlenecks and high energy costs are having a negative impact on businesses.

On a positive note, the labour market continues to be robust. The number of employed persons increased by more than 600,000 in the second quarter and the unemployment rate was at a historic low of 6.6% in July.

The overall inflation rate in the Eurozone cracked the nine percent mark in August, reaching a new record high of 9.1% (July 8.9%). The August rate is the highest since the introduction of the euro as a book currency in 1999. Inflation was driven in particular by the sharp rise in energy prices (up 38.3% year-on-year). In addition, the price increase for food and beverages as well as industrial goods and services accelerated. Core inflation rose from 4.0 to 4.3% in August.

Economic growth in the Eurozone recorded its second consecutive decline in August. Industrial production contracted at an accelerated rate for the third month in a row and the service sector recorded slight business losses for the first time since March 2021. The S&P Global Flash Eurozone Composite PMI fell 1 point to 48.9 over the month, marking the second consecutive month it has been below the 50-point mark above which growth is indicated.

Current inflation (ECB/HICP) +9.1% (08.22)

Current 3 months libor +1.063%

GDP growth 2022 +3.1% (E)

Source: S&P Global and Eurostat

Daniel Beck, Member of the Executive Board

Our conclusion: At its September meeting, the European Central Bank (ECB) sent a clear signal with the largest interest rate hike in its history. It raised the key interest rates by 75 basis points (bp) each. The deposit rate is now 0.75% and the main refinancing rate, at which commercial banks can borrow fresh money from the ECB, is 1.25%. ECB chief Lagarde held out the prospect of further interest rate hikes in the coming months, as inflation is expected to remain high over the longer term, according to the ECB. She stressed that given the continued pressure on energy prices, inflation is expected to reach double digits in the coming months.

Most economists believe that the neutral interest rate, which neither boosts nor slows down an economy, will be reached at around 1.5 to 2.0% in the euro area. Stock markets expect the ECB to raise interest rates to over 2.5% by next spring.

The ECB expects a further increase in the inflation rate in the Eurozone. For the current year, it now forecasts an inflation rate of 8.1%, after anticipating 6.8% in June. Inflation is then expected to fall to an average of 5.5% next year (June forecast: 3.5%) and to 2.3% in 2024 (June forecast: 2.1%).

After a recovery of economic growth in the euro area in the first half of the year, recent data point to a significant slowdown. Uncertainty in the euro area remains high and confidence has fallen. The fight against inflation and withdrawal from ultra-loose monetary policy, Ukraine war and the energy crisis are huge challenges for Europe. The ECB expects economic stagnation for the rest of the year and the first quarter of 2023. ECB experts expect growth of +3.1% for the current year (June forecast: +2.8%). In the following two years, however, a clearly weaker GDP growth rate of +0.9% (previously +2.1%) and +1.9% (previously +2.1%) is expected.

United Kingdom

USA

The Fed's monetary policy turns restrictive

In August, the S&P overall purchasing managers' index (composite PMI) for the US fell further to 44.6 points from 47.7 in July. While the manufacturing sub-index increased from 51.5 to 52.2 in the period, the services sub-index fell from 47.3 to 43.7. The index reading suggests that a stagnant to contracting economy can be expected in 6 months. Technically, the US was already in recession in the first half of 2022 (GDP 1st quarter 2022 = -1.6% and 2nd quarter 2022 = -0.6%). However, given the strength in various sectors of the economy and the labour market, it cannot be assumed that this is already the case. This is also the view of 'The Conference Board' in its report of September 14, 2022, which expects US economic growth of 1.4% this year and 0.3% next year.

US inflation fell to 8.3% in August. While it was down 0.2% from July and down 0.8% from June, it missed market expectations by 8.1%. In addition, the core inflation rate (excluding energy and food prices) increased by 0.4% to 6.3% in August.

Based on this development, a further 0.75% increase in the Fed Fund Rate in the run-up to the Fed meeting on 21 September 2022 from 2.50% to 3.25% was already considered a foregone conclusion in the market. With the August inflation numbers, market expectations have also risen on how high the Fed Fund Rate will rise in this rate cycle. On September 21, the central bank announced its assessment, based on today's data, that it will raise the Fed Fund Rate to 4.25 to 4.5 by the end of the year. This puts monetary policy into a restrictive mode. For next year, the Fed members' average forecast for the Fed Fund Rate is as high as 4.6%, suggesting an end to the rate hike cycle in 2023.

At least the labour market report for August shows some easing: although 315,000 non-farm jobs were created, 15,000 more than expected, the labour force participation rate rose from 62.1% to 62.4% and the unemployment rate from 3.5% to 3.7%. Compared to the previous month, wages stagnated in August.

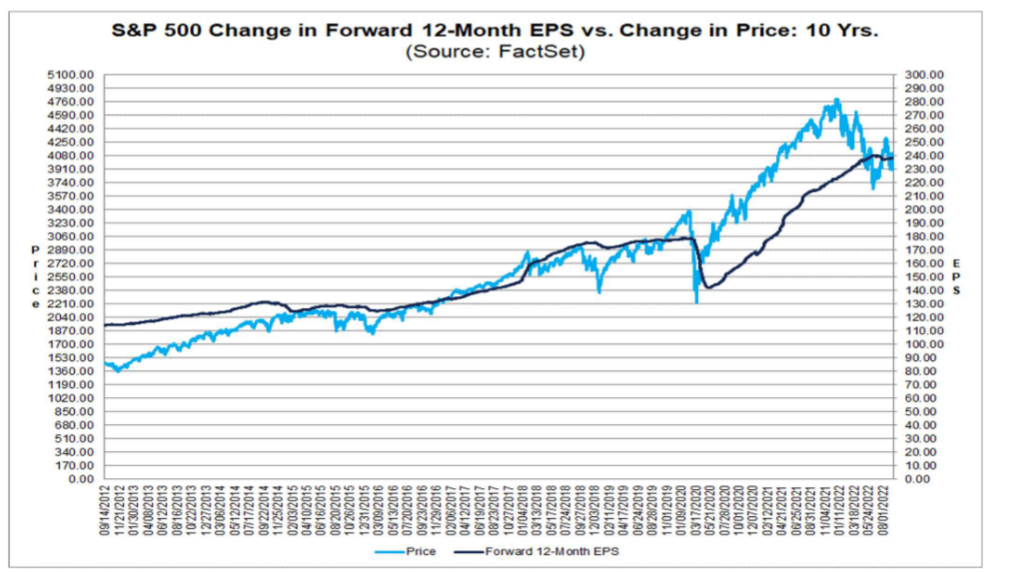

In the second quarter of 2022, 75% of S&P 500 companies beat earnings expectations and 70% beat revenue expectations, according to FactSet. Profits thus grew 6.7% and sales 13.6% compared to the same quarter last year. For the third quarter of 2022, earnings growth is expected to be just 3.5% (down from 9.8% expected at the end of June). As a result, the price/earnings ratio of the S&P 500 based on expected earnings for the next 12 months has risen to 16.4, which is still 12% below the five-year average of 18.6 and 3.5% below the 10-year average of 17.

GDP 2022 +1.4%

Inflation +8.3%

Fed Fund Rate +3.2%

Source: FactSet

Our conclusion: The market is already anticipating a mild recession in 2023. We expect that with the economic slowdown next year, inflation figures will also fall substantially and the Fed will start to ease its restrictive monetary policy again in the course of Q2. Due to the current inflation and growth uncertainties, markets are likely to remain volatile in the coming weeks. However, a strong market recovery is expected as soon as the inflation figures start to come down significantly.

China

Clear elections

Economic data from China for the month of August came in slightly better than expected. Retail sales increased. Industrial production also listed better, even though companies struggled with a power shortage due to the heat wave. The ailing real estate sector continues to cause turmoil and weigh on economic growth. In recent months, numerous real estate developers have had to suspend construction projects due to liquidity shortages. Banks are holding back on new loans, and the increased default rates are making it more difficult to obtain liquidity on the capital market. The central bank is now making financial resources available to commercial banks for loans to real estate developers, in order to solve the credit crunch. To this end, the central bank is trying to stimulate demand by lowering interest rates. Important policy decisions will be made in the coming weeks. The 20th National Congress of the Communist Party of China will be held in Beijing and will open on October 16, 2022. 2'300 delegates will represent the estimated 95 million members of the Chinese Communist Party. XI is expected to be elected for a third term. It would be surprising if there was a change in the general direction. In addition to focusing on per capita economic growth, national security, technological self-sufficiency and long-term decarbonisation targets are likely to be set.

GDP 3.3%

Inflation 2.1%

Shibor 3mth 1.61%

Source: IMF

Our conclusion: At present, there is little to suggest a rapid economic recovery. The stock markets are not expensive after the sharp declines. But the internationally tense political situation and the unclear economic development call for caution.

Japan

Land of the Rising Sun?

Japan is one of the three largest economies in the world, along with the United States and China. It should be noted that the country with its approximately 126 million inhabitants is not exactly one of the most populous countries in the world, is this an advantage in the future? Neither does Japan have abundant mineral resources nor great agricultural potential (only 15% of the land can be used for agriculture). Nevertheless, it is an economy with potential thanks to modern technology and industrial goods. In 2021 alone, around $756 billion worth of goods were exported from Japan. This represents an increase of around $115 billion compared to the previous year. Motor vehicles accounted for 18% of the total, while machinery, electrical equipment and appliances accounted for 14%. Japan exports most of its products to Asia and the USA. However, since the free trade agreement with the EU in 2019, the importance of the European market is also growing. The Japanese central bank has a different monetary policy than other comparable economies in the world and the yen has bottomed out against the USD. A low yen is good for the domestic economy as half of the revenue is generated outside of Japan.

GDP change 2021 2.7%

Inflation July 2022 2.6%

Japan Key Interest Rate -0.1%

Sources: IMF and Bloomberg

Mimi Haas, Lic. Rer.pol. HSG, M.A. in Banking and Finance HSG, Partner

Our conclusion: For investors who want to invest in the short or medium term, Japanese equities may well be worthwhile, but the market environment may also lead to higher volatility. The upward trend in the stock market is likely to continue over the next few years. Here the market is to buy, for example, via an ETF. However, anyone planning to invest in the Japanese stock market for the long term should first consider the challenges facing the country (age pyramid and impact on the economy and a high level of government debt).

Emerging Markets

Strong interest rate hikes?

The available data for the 2nd quarter show that economic momentum has weakened in most economies. High inflation is dampening household consumption and high interest rates are reducing corporate investment. In the wake of the global economic slowdown, export activity is also weakening. Many central banks have raised key interest rates sharply in recent months to reduce pressure on inflation and the USD exchange rate. While the Latin American and Eastern European countries are well advanced in raising interest rates, the Asian central banks are planning several rate hikes.

Quelle Bloomberg, Refinitiv and ZKB

Our conclusion: The weaker global economic outlook, high domestic inflation rates combined with weak domestic currencies are weighing on emerging markets. At present, there is little to be said for new investments.

Stocks

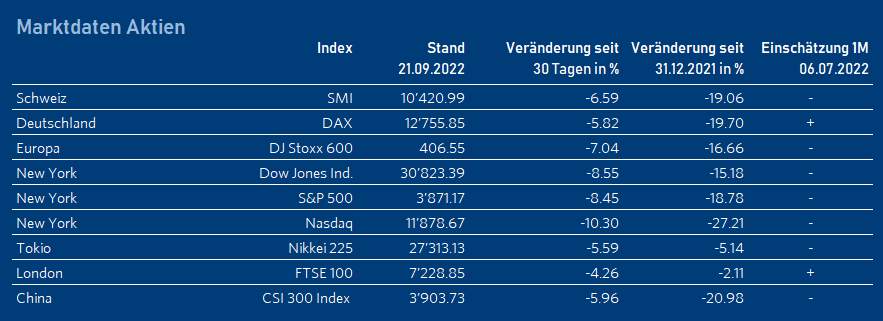

The FED plays the blues

Financial markets have performed exceptionally poor in recent weeks.

On Tuesday September 13, 2022, it was announced that the US consumer price index rose 0.1% in August instead of falling 0.1% as expected. Core inflation readings rose 0.6% month-on-month, while expectations were for half that. The market response was harsh and international. Why would such a small positive change in the consumer price index cause such a sharp market decline?

No doubt a mix of possible US recession with a global reach of indeterminate scope, the impact of higher energy prices on European households and businesses, the evolution of the Chinese economy after the Party Congress and the outcome of the Ukraine war are partly responsible for these market distortions. But the equity and bond markets are most worried by the Fed itself. With inflation in the US seemingly almost unstoppable, the Fed's interest rate and balance sheet measures are both sharp and unprecedented, radiating around the world. The crucial question here seems to be: How much tightening can the economy withstand before borrowing costs rise so far and the availability of credit falls dangerously? In any case, the Federal Reserve is determined to fight inflation urgently. Other central banks are following suit. They have two major tools at their disposal to do so. The first is a conventional tool, raising short-term interest rates. A second tool is the tightening of the Fed's or central banks' balance sheets. This Quantitative Tightening (QT) is the opposite of QE. The Fed sells its bonds or lets them mature, which reduces the Fed's lending to the economy. This tempts investors to park money for as short a time as possible.

The course of the markets is indeed considered a leading indicator for the gains in the economy in the following year (2023). However, this sharp correction contradicts the rosy EPS forecasts of analysts and strategists for profits in 2023. Also, the actual decline in profits and employment has not yet begun. At present, the timing of the next economic recovery is indeed difficult to predict, as the extent of the current downturn is hard to gauge. Given this outlook and the declines in equity markets so far, investors are avoiding cyclical stocks until the recession has started. In the meantime, many investors are parking their capital in the increased interest rates or in value stocks.

Source: FED

Our conclusion: The markets have already corrected strongly and have a rather low valuation due to the high forecast uncertainty. Nevertheless, we continue to believe that it is premature to buy cyclical stocks based on the recovery outlook as long as interest rate stabilisation has not yet started. We continue to favour high dividend paying quality stocks with a business model that generates high cash flows for the companies.

Interest

Revival: Traditional role as diversifier?

In the current phase, which rarely occurs, where yields of equities and bonds fall at the same time, this is usually followed by a good performance.

Government bonds: The yield curve of US Treasuries has inverted sharply since the beginning of the second half of the year. Inflation remains high and recession risks have increased. Given the Fed's determination to restore price stability, monetary tightening is likely to be the focus at the moment. Both nominal and real yields are likely to trend upwards in the short term, albeit at a slower pace than in S1 2022, as financing conditions in general have already become much tighter. Europe presents a similar but gloomier picture here. The risk of a recession, rising key interest rates, the growth crises and political uncertainties are leading to higher spreads between Italian and German bonds.

Our conclusion: We see government bonds as rather neutral.

Investment grade bonds (IG): For investors who want to take advantage of the attractiveness of European corporate bonds, these can be an interesting solution in USD. In IG, we prefer non-cyclical sectors and senior US financials given the persistently high inflation and recession risks. Furthermore, higher potential returns can be found in short maturities.

Our conclusion: We are cautious on investment grade (IG) bonds at the moment.

High yield bonds (HY): Solid credit data, especially for US HY energy stocks, should offset recent macroeconomic uncertainties. However, the extreme risk of an abrupt widening of spreads, especially in longer-dated areas, is increasing. Geopolitical tensions complicate the already precarious balance of the domestic economic outlook, significant corporate pricing power and the withdrawal of expansionary monetary policy by central banks to curb inflation.

Our conclusion: We continue to believe that high-quality HY corporate bonds can provide good diversification in a bond portfolio. One should look for higher quality in the segment and shorter duration.

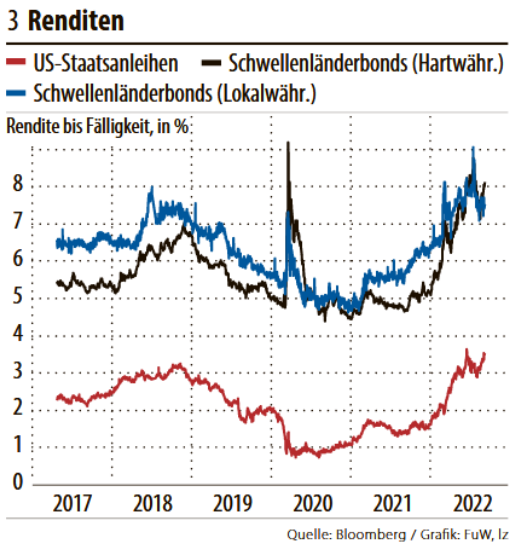

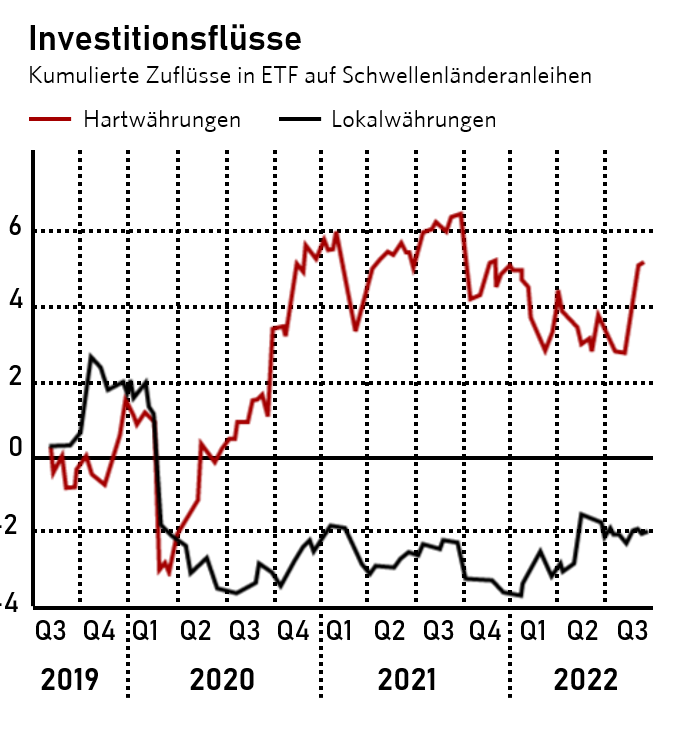

Emerging Markets bonds (EM): EM offer a yield premium for higher default and currency risk. Economic data are still better than expected. An expiring interest rate hike by Western central banks, which may take place in 2023, is also positive for these bonds. With a yield of 8%, EM in hard currencies (exchange rate risk minimised) are interesting for investors who are prepared to take the risk.

Our conclusion: We consider it interesting for riskier investors to invest in EM in hard currencies. ETFs should be considered to reduce the risk of default.

Source: F&W, Bloomberg and Financial Times

Mimi Haas, Lic. rer.pol. HSG, M.A. in Banking and Finance HSG, Partner

Currencies

Safe haven, central banks and interest rates have influenced currencies since the beginning of the year.

EUR/USD (22.09.2022 0.98)

The euro continues to fall against the greenback, which is considered as a safe haven. Even if the ECB raises interest rates and the interest rate differentials will not widen much further, the interest rate advantage in the USD will remain.

Our conclusion: The existing interest rate differential and the geopolitical situation continue to strengthen the dollar, and the trend we have seen since the beginning of the year is unbroken.

EUR/CHF (22.09.2022 0.97)

The economic slowdown in the euro zone will continue. No factor such as war in Ukraine or supply chain problems has been solved. The Swiss National Bank has a greater potential to raise interest rates, growth prospects are better in Switzerland and Switzerland has a more solid current account surplus. The deteriorating environment further strengthens the franc as a safe haven investment.

Our conclusion: As long as the above scenario persists, the franc will remain strong and may even rise slightly in the coming months.

USD/CHF (22.09.2022 0.98)

The USD continues to be strong against the CHF. The persistent and high inflation in the USA is visibly forcing the US Federal Reserve to tighten monetary policy earlier and more strongly. If the interest rate in Switzerland is still slightly negative, despite the first interest rate hike in many years, the picture in the USA is different. The interest rate differential leads to a strong dollar.

Our conclusion: This will remain the case.

Source: Market Map und Financial Times

Mimi Haas, Lic. rer.pol. HSG, M.A. in Banking and Finance HSG, Partner

Oil

Consolidation of the oil price at a lower level

The price of a barrel of Brent crude returned below USD 90 in September. The price peaked at USD 139 per barrel in March 2022. At the last OPEC+ meeting on September 5, 2022, a rather symbolic cut of 100,000 barrels of oil per day for October was decided. This was done as a precautionary measure to counteract oversupply as early as possible and out of uncertainty about the further development of demand due to the emerging cooling of the global economy. However, demand in the northern hemisphere could pick up again over the winter months.

Our conclusion: We expect that the foreseeable global decline in demand for black gold will lead to further declining oil prices in the course of next year, but that prices will trend sideways in the coming months due to the upcoming winter season.

Precious Metals

US real yields and strong dollar weigh down

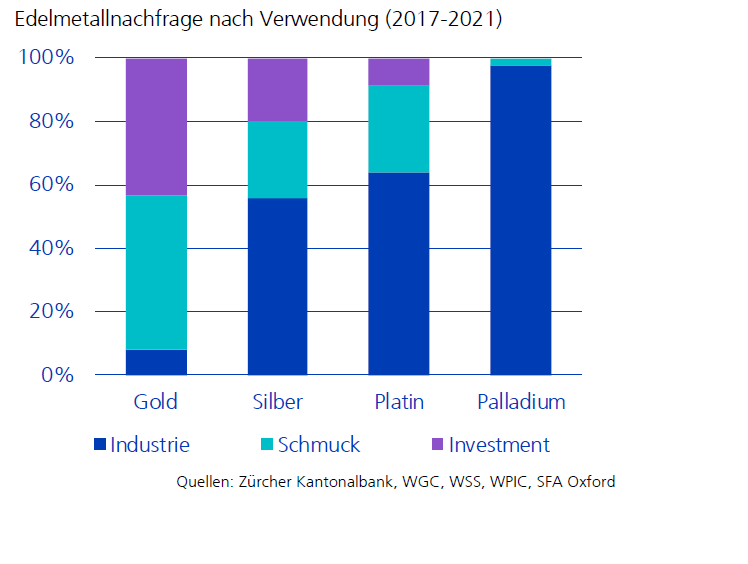

The ongoing tightening of US monetary policy is putting pressure on gold (current price at USD 1,670 per ounce) and other precious metals. But gold in particular remains in demand for diversification in the geopolitically uncertain environment. Supporting this are buyers who are currently taking advantage of the lower prices to get into gold. The big gold consumers India and China have increased imports, as have the central banks. Due to the gloomy global economic outlook and sluggish growth in China and the US, the industry's demand for platinum (current price at USD 922 per ounce) is currently lower.

The ongoing tightening of US monetary policy is putting pressure on gold (current price at USD 1,670 per ounce) and other precious metals. But gold in particular remains in demand for diversification in the geopolitically uncertain environment. Supporting this are buyers who are currently taking advantage of the lower prices to get into gold. The big gold consumers India and China have increased imports, as have the central banks. Due to the gloomy global economic outlook and sluggish growth in China and the US, the industry's demand for platinum (current price at USD 922 per ounce) is currently lower.SoS

Source: ZKB

Andreas Betschart, Business Manager

Our conclusion: In the medium term, gold will have opportunities as soon as the Fed rate hike cycle is completed. Platinum will continue to recover as the economy improves. Price range Gold from USD 1,650 to 1,800 per ounce and platinum from USD 900 to 1,050 per ounce.

Abbreviations and explanations

bbl: 1 Barrell = 158,987294928 Litre

Bp: Basis points

GDP: Gross domestic products

BIZ: the Bank for International Settlements is an international financial organization. Membership is reserved for central banks or similar institutions.

EM-Bonds: Emerging market bonds. An emerging market is a country that is traditionally still counted as a developing country but no longer has its typical characteristics.

HY-Bonds: Fixed-income securities of poorer credit quality. They are rated BB+ or worse by the rating agencies.

IG-Bonds: Investment grade bonds are all bonds with a good to very good credit rating (Ra-ting). The investment grade range is defined as the rating classes AAA to BBB-.

IHS Markit: Listed data information services company

IWF: The International Monetary Fund (also known as the International Monetary Fund) is a legally, organiza-tionally, and financially independent specialized agency of the United Nations headquartered in the United States of America.

KOF: Business Cycle Research Centre at ETH Zurich

LIBOR: London Interbank Offered Rate is a reference interest rate determined in London on all banking days under certain conditions, which is used, among other things, as the basis for calculating the interest rate on loans.

OPEC: Organization of the Petroleum Exporting Countries

OPEC+: Cooperation with non-OPEC countries such as Russia, Kazakhstan, Mexico and Oman.

oz: the troy ounce is used for precious metals as a unit of measurement and is equal to 31.1034768 grams

Saron: The Swiss Average Rate Overnight is a reference interest rate for the Swiss franc

Seco: Swiss State Secretariat for Economic Affairs

Spread: Difference between two comparable economic variables

WTI: West Texas Intermediate. High-quality US crude oil grade with a low sulfur content.

Disclaimer:

The information and opinions have been produced by Chefinvest AG and are subject to change. The report is published for information purposes only and is neither an offer nor a solicitation to buy or sell any securities or a specific trading strategy in any jurisdiction. It has been prepared without regard to the objectives, financial situations or needs of any particular investor. Although the information is derived from sources that Chefinvest AG believes to be reliable, no representation is made that such information is accurate or complete. Chefinvest AG does not assume any liability for losses resulting from the use of this report. The prices and values of the investments described and the returns that may be received will fluctuate, rise or fall. Nothing in this report is legal, accounting or tax advice or a representation that any investment or strategy is appropriate to personal circumstances or a personal recommendation for specific investors. Foreign exchange rates and foreign currencies may adversely affect value, price or yield. Investments in emerging markets are speculative and involve considerably greater risk than investments in established markets. The risks are not necessarily limited to: Political and economic risks, as well as credit, currency and market risks. Chefinvest AG recommends investors to make an independent assessment of the specific financial risks as well as the legal, credit, tax and accounting consequences. Neither this document nor a copy of it may be sent in the United States and/or in Japan and they may not be handed over or shown to any American citizen. This document may not be reproduced in whole or in part without the permission of Chefinvest AG.