Click on the images to view our comments on each topic.

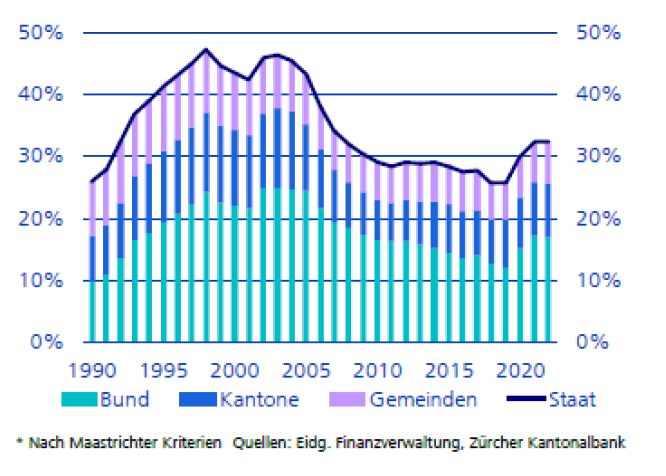

Switzerland

The economy shows muscles

The latest available GDP growth figures were ex-tremely positive, leaving GDP only slightly below the pre-crisis level. Both the consumer sentiment index and the PMI index for industry and services were at all-time highs this summer. The September data are also at a very high level. The pandemic-related supports of Swiss economic policy continue to work. Short-time work compensation is still running for a few months and the repayment of the Covid loans has not yet started. Although the supply constraints in the global economy and the leading indicators for the 4th quarter point to a flattening of growth momentum, an economic slump is not expected. The SNB's new inflation forecasts of 0.5% for this year and 0.7% for next year are slightly higher than the June data. The main reason for this is higher prices for oil products, electricity and goods affected by supply bottlenecks. In the longer term, the inflation forecast remains unchanged at 0.6% for 2023.

Our Conclusion: Leading indicators point to a slight slowdown in economic momentum. According to the SNB, inflationary pressure is limited and unemployment should soon return to pre-crisis levels. Government debt has risen as a result of the support measures, but the absolute figures are very low by international standards. Many listed Swiss companies have solid balance sheets and benefit from their leading position in the international market. We remain positive for the Swiss stock market.

European Union

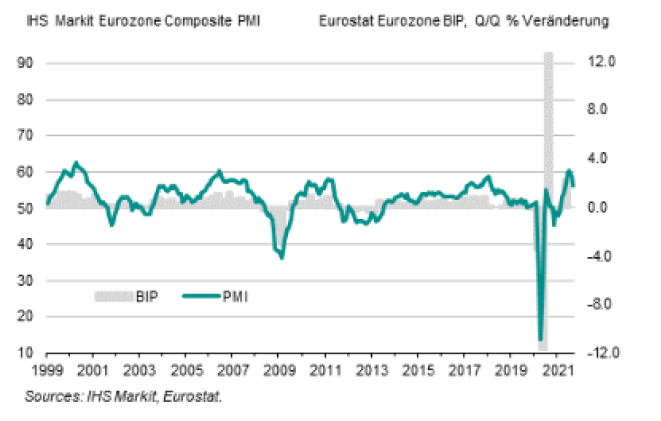

Continuation of high growth momentum

The IMF has again raised its economic forecast for the Eurozone for the current year 2021. Instead of the 4.6% forecast in July, the economy in the monetary union will grow by 5.0%. The reason for the better forecast is higher than expected growth in France and Italy. For 2022, the IMF has left its forecast at 4.3% growth in the Eurozone. After a very strong 2nd quarter, growth momentum has recently slowed somewhat due to persistent supply bottlenecks and sharp rises in energy prices. However, the leading indicators continue to signal above-average growth for the coming months. Following a previous rate of 3.0%, inflation rose to 3.4% in September. This is the highest increase in 13 years. The increase was driven by both core inflation and the continued momentum of energy prices. Almost half of the annual rate is attributable to higher energy prices. The ECB expects inflation rates to exceed 3.0% until the end of the year, followed by a gradual decline. The final IHS Market Eurozone Composite Index (PMI) fell to 56.2. For the first time since the outbreak of the Corona pandemic in early 2020, the service sector grew faster than industrial production.

Our Conclusion: The economy in the Euro area has clearly recovered. The rapid economic rise is largely attributable to the resolute support measures taken by the central bank and sovereigns. As expected, the ECB Council decided at its September meeting to moderately reduce monthly purchases under the current Corona Emergency Program (PEPP). A decision on the detailed implementation of the reduction will be taken on December 16, 2021. Interest rates will remain unchanged. ECB chief Christine Lagarde has already signaled that a decision on the future of these purchases will be made at the December meeting. Even with a less loose monetary policy, financial conditions remain expansionary. The current surge in inflation in the Euro area is not forcing the ECB to act. In the ECB's view, much of the current upward pressure on prices is only temporary.

United Kingdom

USA

Congress needs to show leadership

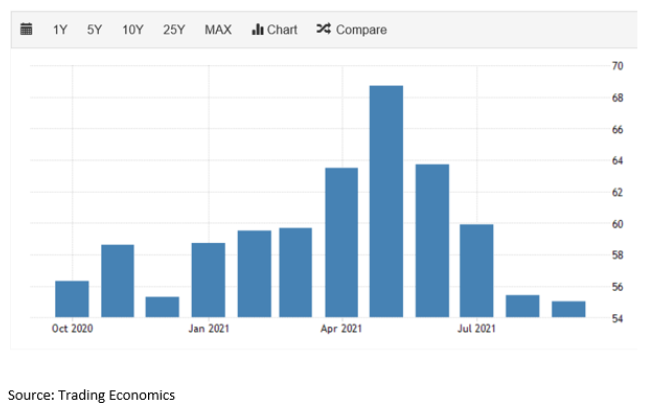

In Congress, the infrastructure package of USD 1 trillion and the much larger social and health package of USD 3.5 trillion are still being debated. The Democrats in the House of Representatives want to combine the two fiscal packages, with internal wing wars dragging out the compromise process. The Purchasing Managers Index (PMI US Compo-site) weakened to 55 index points in September (60.7 for manufacturing and 54.9 for services). However, this value still signals appealing economic growth in the next 3 to 6 months. For 2021, the IMF expects GDP growth in the U.S. of 6.0% and for 2022 of 5.2%. The labor market report for September 2021 disappointed, with only 194,000 new nonfarm jobs created (after all, the August numbers were revised up from 235,000 to 366,000 new jobs). On the other hand, the unemployment rate has fallen from 5.2% to 4.8% during this period, which, combined with a declining employment rate, is already beginning to partially result in a labour shortage. For the corporate profits in the third quarter of 2021 of the companies listed in the S&P 500 Index, analysts expect an average increase of 27% compared to the previous year. The start has been successful with the already released earnings reports with an average of +30 %. Due to ongoing international supply constraints and the related price pressure, the Chairman of the Fed (US Federal Reserve), Jerome Powell, has concretised the Fed's expectations to the effect that the currently higher monthly inflation figures (September +5.4%) will probably not decline before spring 2022 instead of by the end of 2021. Furthermore, the Fed is expected to start tapering (the reduction of monthly bond purchases) in November and to stop purchases altogether by the summer of 2022, beginning to raise short-term interest rates as early as the end of 2022.

Our Conclusion: As long as the economy is booming and medium- to long-term inflation expectations remain low, corporate sales and earnings figures, and thus also the stock markets, should perform positively.

China

Real estate risk?

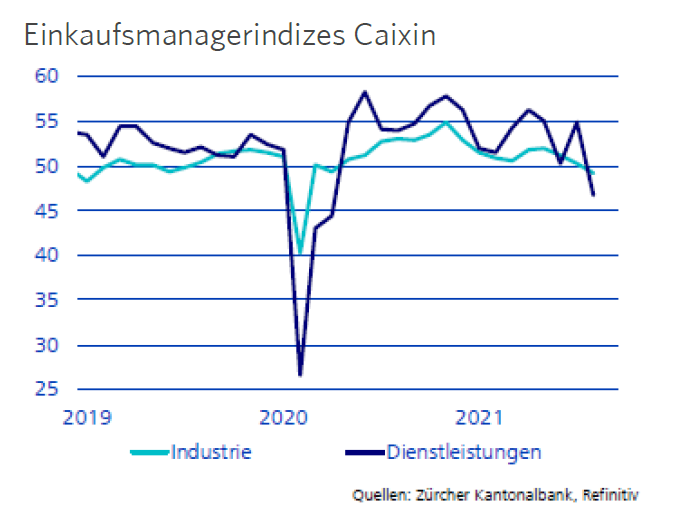

In the third quarter, the economy developed weaker than expected. Unfavorable weather conditions, local virus outbreaks with corresponding restrictions and supply constraints were responsible for this. In addition, the Chinese government has intervened strongly in economic activity in recent months with comprehensive regulatory initiatives. The aim is to limit the market power of certain companies, and similar concerns also preoccupy Western governments. The topics are the abuse of market power, consumer rights, data protection, national security, small business protection and equality of opportunity. The decisive actions of Chinese officials and the lack of communication surprised stock market participants, resulting in sharp declines in share prices. The Internet sector and private education providers were particularly hard hit. In addition, the collapse of the real estate giant Evergrande became known in September. The government is expected to wind down the company in a controlled manner under state supervision, to avoid chain reactions in the financial system. The protection of domestic private investors is the top priority, ahead of international bond investors. In terms of the economy as a whole, the Evergrande case is likely to have only a limited impact on the liquidity system.

Our Conclusion: Growth expectations for the national economy have fallen slightly this year to around 8% for the year as a whole. China continues to offer an attractive environment for well-positioned companies in forward-looking sectors. However, political intervention in the economy calls for caution in new investments.

Japan

Positive Impulse and changes?

Japanese Prime Minister Yoshihide Suga unexpectedly stepped down from the race for the ruling LDP (Liberal Democratic Party) leadership last month, making way for younger and more electable LDP leadership. Fumio Kishida has taken over the regime, attacked his own party and distanced himself from the famous Abenomics program. He wants to reform his country in the coming years and return to growth, stability and an efficient economy and is ready to embrace change. During the Olympic and Paraolympic Games, the Delta variant burdened the Japanese with a fifth wave. In the weeks that followed, the country was able to increase the rate of vaccination. The domestic economy improved as a result of the accelerated vaccination strategy, positive political stimulus and better-than-expected quarterly corporate results. This was followed by a rally on the Japanese stock market and the Nikkei index is hovering around 30,000 points.

Our Conclusion: Due to the positive factors, the stock market has recovered disproportionately in recent weeks. Nevertheless, it lags behind the global indices. This is unlikely to change in the short term.

Emerging Markets

Growth shift

In Latin America and Eastern Europe, catch-up effects in the 3rd quarter supported the progress of the economy. However, these are expected to gradually diminish as monetary policy headwinds strengthen. In Asia, however, growth is beginning to accelerate as many countries ease viral containment measures. India is recovering at a remarkable pace and mobility recently even rose above pre-crisis levels. Unfortunately, however, Prime Minister Modi's government has postponed unpopular reforms to deregulate the agricultural sector and make the labor market more flexible. The purchasing managers' indices of the ASEAN countries also indicate a clear recovery of the economy. By contrast, the inflation rate in most countries has continued to rise sharply, and de-spite interest rate hikes by the various central banks, inflationary pressure remains high. Most economists expect significant interest rate hikes at the end of the year and by mid-2022.

Our Conclusion: The economic development of the emerging markets is encouraging. High inflation rates and rising government debt are unsettling investors and have led to currency losses against the currencies of the industrialized nations. The central banks are trying to curb inflation and stabilize the currencies with further interest rate hikes. We do not recommend new investments in these markets.

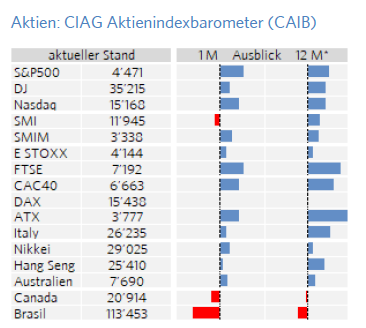

Stocks

Energy stocks step on the gas

After the considerable price corrections on the Chinese and Hong Kong stock exchanges, calm has returned, and Japan even gained. The French, Canadian and German stock markets performed disappointingly. While the American markets remained virtually unchanged, the prices of Swiss and Austrian stocks continued to rise. At the sector level, energy stocks recorded a fulminant rise, gaining an average of 20%. This euphoria is likely to continue and we continue to favor this sector along with financials and healthcare stocks. On the other hand, we are negative on mining stocks. Expectations have changed in line with the sharp decline of over 40% in the iron ore price over the last 3 months. In general, the CAIB shows an unchanged positive expectation for the next months with an opportunity value of +0.13. The long-term value is even higher at +0.24. We recommend investors with an investment view of more than 12 months to buy shares. Preferred Trend: Semiconductors are an important factor in the entire electronic value chain. In an increasingly technology-driven global economy, this role will only grow. The ongoing global chip shortage has highlighted this key role.

Interest

Interest rate shock in China

Government bonds

As expected, this asset class recorded significant losses at the long end. While interest rates on government bonds in EUR, CHF and JPY are still in negative territory, GBP and USD are offering positive interest rates.

Our Conclusion: While the US Federal Reserve has greater room for maneuver, the ECB is not yet in a position to throttle the economy's liquidity engine. In our view, interest rates in CHF and EUR will therefore remain negative for the next reporting period. Underweight.

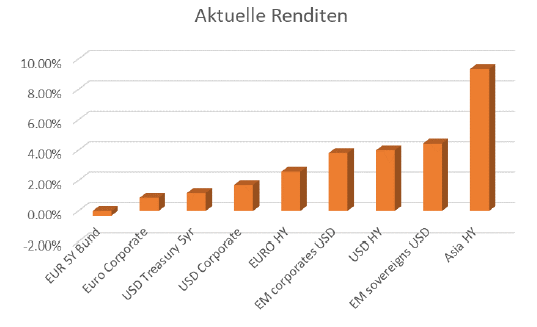

Investment-grade-bonds (IG)

The spreads remained unchanged and therefore this category consequently also showed a negative return (USD approx. -1.0%, EUR -0.6%). While the IG investments in USD now offer over 2.0% interest, the interest rates in the EUR area are still at an average of 0.4%.

Our Conclusion: Inflation concerns seem more weighted than the turbulence in the high yield market. While we are becoming neutral on US bonds, we remain cautious on EUR and CHF. We continue to prefer inflation protected IG bonds at this interest rate level.

High Yield bonds (HY)

The scandal surrounding the Chinese real estate company Evergrande and the resulting uncertainties, also with regard to the economic development in China, continue to drive up spreads. We currently have a spread for Asian HY of 849 points. The USD and EUR HY bonds were able to escape this trend somewhat. Interestingly, the spreads on USD HYs fell by the same level that they rose on EUR HYs.

Emerging Markets bonds (EM) Sovereigns

This asset class saw little increase in spreads, indicating unshaken investor confidence. Following IG and government bonds, this category also recorded losses mainly due to inflation concerns.

Our Conclusion: Despite the high yield, we currently refrain from investing in high-yield bonds in Asia. Due to the good riskreturn ratio, we are positive on HY EUR and USD, but also on short-term EM investments in USD.

Currencies

All under the sign of US taper?

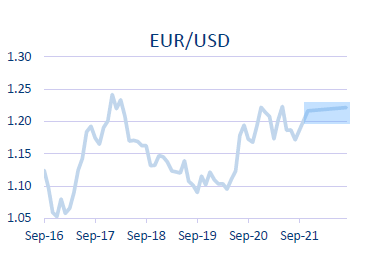

EUR/USD (Current 1.1582)

Positive for the USD could be the start of tapering by the Fed. Negatives, on the other hand, are inflation, rising energy costs and global economic development. The week of 18.10.2021 will be important for the development, as several speakers of the FED will speak. Chartwise, resistance levels are at 1.1750, 1.1650 and 1.1590 and support levels are at 1.1500, 1.1425 and 1.1350.

Our Conclusion: We expect the USD to strengthen in the short term. For the longer-term trend, it will be important how the FED positions itself.

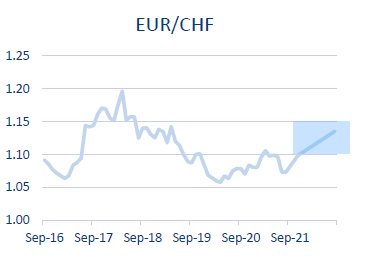

EUR/CHF (Current 1.0729)

The CHF strengthened against the EUR in Octo-ber following an interview by the SNB's vice president. Inflation fears in the eurozone and stagflation in the global economic recovery are causing the CHF to strengthen further. From a chart perspective, the resistance levels are at 1.1020, 1.0910 and 1.0860 and the support levels are at 1.0710, 1.0690 and 1.0630.

Our Conclusion: We expect a positive impulse for the CHF in the short term.

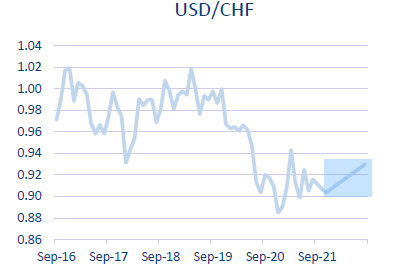

USD/CHF (Current 0.9260)

The same interview by the SNB has caused the USD to appreciate against the CHF. For a continuation of this trend, however, further catalysts are needed, such as the FED's behavior with regard to interest rates and tapering. Chart-technically, the resistance levels are at 0.9475, 0.9370 and 0.9330 and the support levels are at 0.9240, 0.9180 and 0.9150.

Our Conclusion: We expect the USD to move sideways against the CHF in the short and medium term

Oil

In OPEC+ the hardliners retain the upper hand

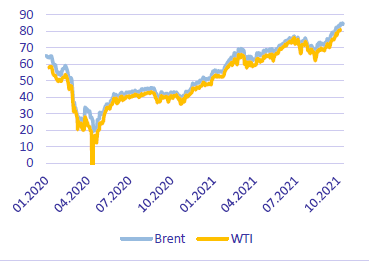

The WTI oil price has risen sharply in recent weeks to a multi-year high of USD 84 per barrel. On the demand side, the gradual recovery of the global economy from the Covid-19-related economic slump in 2020 is making itself felt. On the supply side, OPEC+'s decision in early October to maintain only gradual monthly increases of 400,000 bbl of oil per day is having an impact. However, the oil-producing countries know from experience that oil price overheating has a negative impact on demand and thus also on prices in the medium term.

Our Conclusion: Should the global economic recovery continue in line with expectations, a stronger increase in oil production by OPEC+ is to be assumed. We slightly adjust our 12-month forecast for WTI oil to USD 75 bbl.

Precious Metals

No Golden Autumn

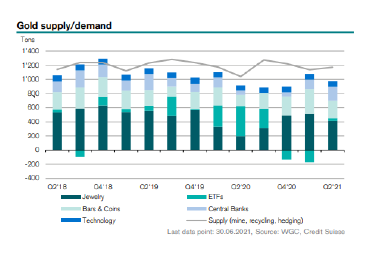

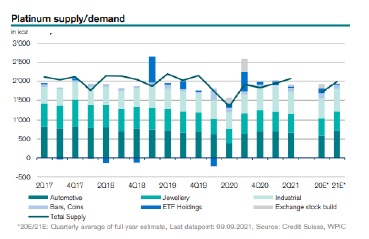

Ongoing strong U.S. economic data and short-term inflation fears are a negative combination for gold and continue to cause the gold price to fluctuate between USD 1,720 and USD 1,800. Currently the gold price is around USD 1'777 per ounce, which is favorable for the largest gold buyer, the jewelry industry. Platinum is currently quoted around USD 1,047 per ounce. The largest consumer of platinum is the automotive industry, especially in Europe due to the large number of diesel vehicles. Gold and platinum continue to be a good means of diversification, and if inflation fears persist, gold should also increase in value again.

Our Conclusion: At present, we expect the gold price to move sideways. In the coming months, we continue to expect the gold price to move in a range of USD 1,700 to 1,850 per ounce. For platin, we forecast a range of USD 1,000 to 1,100 per ounce.

Abbreviations and explanations

bbl: 1 Barrell = 158,987294928 Litre

Bp: Basis points

GDP: Gross domestic products

BIZ: the Bank for International Settlements is an international financial organization. Membership is reserved for central banks or similar institutions.

EM-Bonds: Emerging market bonds. An emerging market is a country that is traditionally still counted as a developing country but no longer has its typical characteristics.

HY-Bonds: Fixed-income securities of poorer credit quality. They are rated BB+ or worse by the rating agencies.

IG-Bonds: Investment grade bonds are all bonds with a good to very good credit rating (Ra-ting). The investment grade range is defined as the rating classes AAA to BBB-.

IHS Markit: Listed data information services company

IWF: The International Monetary Fund (also known as the International Monetary Fund) is a legally, organiza-tionally, and financially independent specialized agency of the United Nations headquartered in the United States of America.

KOF: Business Cycle Research Centre at ETH Zurich

LIBOR: London Interbank Offered Rate is a reference interest rate determined in London on all banking days under certain conditions, which is used, among other things, as the basis for calculating the interest rate on loans.

OPEC: Organization of the Petroleum Exporting Countries

OPEC+: Cooperation with non-OPEC countries such as Russia, Kazakhstan, Mexico and Oman.

oz: the troy ounce is used for precious metals as a unit of measurement and is equal to 31.1034768 grams

Saron: The Swiss Average Rate Overnight is a reference interest rate for the Swiss franc

Seco: Swiss State Secretariat for Economic Affairs

Spread: Difference between two comparable economic variables

WTI: West Texas Intermediate. High-quality US crude oil grade with a low sulfur content.

Disclaimer:

The information and opinions have been produced by Chefinvest AG and are subject to change. The report is published for information purposes only and is neither an offer nor a solicitation to buy or sell any securities or a specific trading strategy in any jurisdiction. It has been prepared without regard to the objectives, financial situations or needs of any particular investor. Although the information is derived from sources that Chefinvest AG believes to be reliable, no representation is made that such information is accurate or complete. Chefinvest AG does not assume any liability for losses resulting from the use of this report. The prices and values of the investments described and the returns that may be received will fluctuate, rise or fall. Nothing in this report is legal, accounting or tax advice or a representation that any investment or strategy is appropriate to personal circumstances or a personal recommendation for specific investors. Foreign exchange rates and foreign currencies may adversely affect value, price or yield. Investments in emerging markets are speculative and involve considerably greater risk than investments in established markets. The risks are not necessarily limited to: Political and economic risks, as well as credit, currency and market risks. Chefinvest AG recommends investors to make an independent assessment of the specific financial risks as well as the legal, credit, tax and accounting consequences. Neither this document nor a copy of it may be sent in the United States and/or in Japan and they may not be handed over or shown to any American citizen. This document may not be reproduced in whole or in part without the permission of Chefinvest AG.