Click on the images to view our comments on each topic.

Switzerland

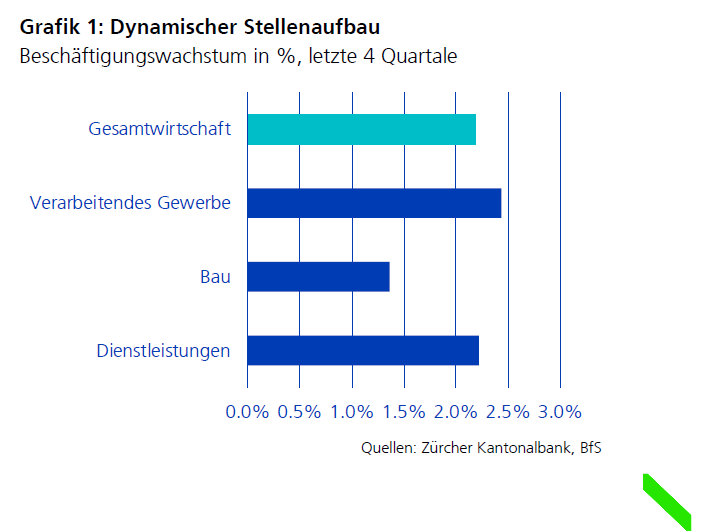

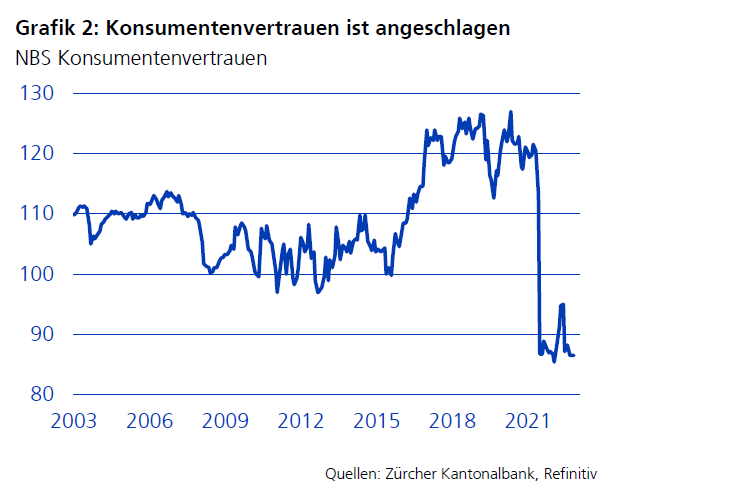

Private consumer demand provides support

Private consumption is proving to be a major pillar of the Swiss economy. Population growth is unabated and the local labor market is also robust. At the end of October, the authorities reported an unemployment rate of 2.00%. The labor market shows that over 100,000 new jobs were created in 2023, which corresponds to the growth of over 2.20%. This will also have an impact on private consumption in the coming quarters. By contrast, the industrial sector could feel the effects of the economic slowdown in the eurozone, particularly in Germany. Inflation has been falling for months and the probability of a final interest rate hike by the SNB in December is decreasing. Real estate prices are moving sideways. Residential real estate remains in high demand due to strong immigration coupled with low new construction activity. There is an oversupply of commercial real estate in peripheral locations.

SECO Economic Forecast

GDP 2023: 1.30%(E)

GDP 2024: 1.20%(E)

Inflation 2023: 2.20%(E)

Inflation 2024: 1.90%(E)

SNB key interest rate: 1.70%

Our conclusion:

The SECO forecasts are still positive for this year with GDP growth of 1.30%. For the coming year, economists are forecasting growth of 1.20% and slightly higher unemployment of 2.30%. The Swiss stock market has performed disappointingly so far. The defensive sector orientation, an expected average dividend yield of 3.50% and the historically moderate valuation should give equities a boost. We consider Swiss equities to be attractive.

Sources: SECO, ZKB, IMF

As of 14.11.2023

European Union

Weak economy continues - lower inflation

The eurozone's gross domestic product (GDP) fell by 0.10% in the third quarter of 2023 compared to the previous quarter due to weak consumption and low investments. At country level, Germany is primarily responsible for the ongoing economic weakness in the eurozone. Global trade in goods is still on a downward trend and Europe's largest economy (Germany) is suffering particularly badly as a result. In contrast, France and Spain are still recording slight growth, while Italy's GDP is stagnating.

The economy in the eurozone has so far benefited from the strength of the labor market. The seasonally adjusted unemployment rate in the eurozone was 6.50% in September, a slight increase from 6.40% in August. In the European Union (EU), the unemployment rate was 6.00% in September, unchanged from August. However, there are signs of a slight slowdown in the labor market. Fewer jobs are being created, including in service sector, which is in line with the gradual impact of the economic slowdown on employment.

The annual inflation rate in the eurozone fell significantly from 4.30% in September to 2.90% in October. This means that inflation has fallen below 3.00% for the first time since July 2021. At the same time, price pressure on food only eased slightly and recession fears increased. The core rate excluding the volatile prices for energy and food also fell - from 4.50% to 4.20%. Energy prices in the 20 eurozone countries fell by 11.10% compared to the same month last year.

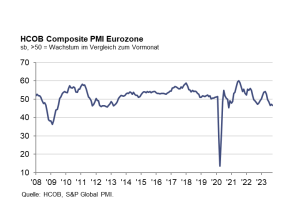

In October, the eurozone economy contracted more sharply than at any time in the past three years due to an accelerated decline in demand. The HCOB services index for the eurozone stood at 46.5 points, after 47.2 points in September, the fifth consecutive month below the growth mark of 50 points. The main reason for this was the accelerated downturn in the service sector. Industrial production fell just as sharply as in September. This was the third consecutive month of decline in both sectors.

GDP growth 2023 +0.70% (E)

EU Inflation 2023 +5.60% (E)

Current 3-month Libor +3.99%

Our conclusion:

The economic outlook for the eurozone remains subdued in the fourth quarter. The European economy is currently lacking decisive growth stimulus. Tensions in the Middle East are also influencing the global economy. It is to be hoped that the war in the Middle East will not escalate any further. Production in the manufacturing sector has continued to decline and the slowdown in industry is spreading to other sectors. Weak external economic stimuli and the high interest rate environment are weighing on the economy.

The sharp fall in inflation in October to 2.90% in the eurozone is a good sign. It is largely due to the high volatility of energy prices. A rapid and far-reaching recovery in consumption is not to be expected this year. Survey indicators (S&P Global purchasing managers' indices, business and consumer confidence from the EU Commission) do not point to an imminent economic recovery.

However, the economy should pick up over the next few years in anticipation of a further decline in the persistence inflation, a recovery in real household incomes and higher demand for eurozone exports. Consumption will benefit from an improvement in the real income situation of households and, in addition, global industry should recover at least slightly in the coming year after the almost two-year slowdown.

The European Central Bank (ECB) ended its cycle of interest rate hikes at its October meeting and left the three key interest rates unchanged after ten rate hikes in a row.

The interest rate for the main refinancing operations and the interest rates for the marginal lending facility and the deposit facility remain unchanged at 4.50 %, 4.75% and 4.00% respectively. The interest rate decision had already been largely priced in by the markets. The ECB reiterated its position that it should bring inflation back to its target of 2.00% in the medium term if it leaves interest rates at the current level for a sufficiently long period. However, the ECB has to deal with a weak economic environment and slow economic growth of just 0.70% for this year.

On the positive side, the Ukraine war is over or no longer relevant for the financial markets. Based on the outlook for the European economy, we maintain our optimistic assessment for the European stock market.

Daniel Beck, Member of the Executive Board

Sources: European Commission, Statista, HCOB, S&P Global

As of 13.11.2023

United Kingdom

USA

Strong economic and productivity growth

The gross domestic product of the USA grew by a strong 4.90% in the third quarter of 2023. The increase in productivity of 4.70% in this period was also very impressive. It could well be that the use of artificial intelligence in work processes is already starting to have a positive impact on efficiency gains.

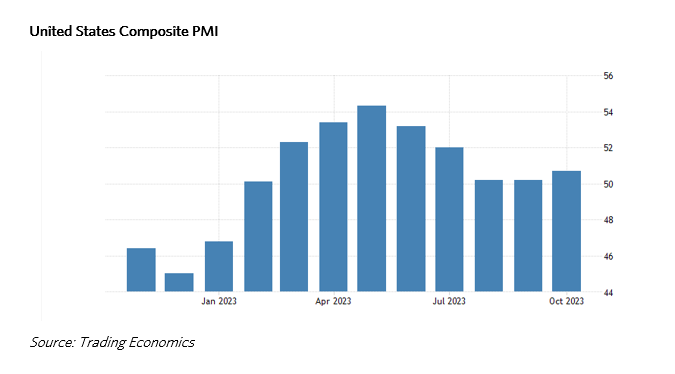

The S&P Global US Composite PMI improved in October from 50.2 to 50.7 index points compared to September. It is interesting to note that the sub-index for the manufacturing sector also rose from 49.8 to 50, which is positive.

The inflation rate fell significantly in October to 3.20% (September 3.70%). The core rate (excluding energy and food), which is important for the Fed, fell to 4.00% in October (September 4.10%).

The labor market continues to cool slowly, as intended by the central bank. Only 150,000 new non-farm jobs were created in October (180,000 were expected). This is well below the average of 258,000 new jobs created in the last 12 months. Unemployment rose accordingly to 3.90% in October (September 3.80%). However, at 1.5 job vacancies per jobseeker, this ratio remains high in historical terms. This ratio would probably have to fall below the 2019 level (1.2) in order to be able to speak of normalization. On the positive side, the voluntary dismissal rate is starting to fall significantly, which means that employers elsewhere are no longer tending to pay higher wages.

At its meeting on October 31 / November 1, 2023, the Fed paused again and left the target range for the Fed Fund Rate at 5.25 - 5.50%. Fed Chairman Jerome Powell's comment last week that he is not sure whether the current interest rate level is restrictive enough at least leaves the back door open for further rate hikes. Meanwhile, however, the market is assuming a 50.00% probability of a rate cut of 0.25% as early as May 2024.

Of the 92.00% of companies represented in the S&P 500 Index that have already disclosed their Q3 figures, 81.00% reported higher-than-expected earnings and 61.00% higher-than-expected sales. The average earnings growth in the 3rd quarter for these companies was therefore much higher than expected at +4.10%.

Based on earnings estimates for the next 12 months, the S&P 500 Index continues to achieve a price/earnings ratio of 18.0. The 5-year average is 18.7 and the 10-year average is 17.5.

GDP2023 (IMF): +2.10% (E)

Inflation2023 (IMF): +4.10% (E)

Fed Fund Rate: +5.50%

Our conclusion:

The labor market continues to cool, but is still robust. The trillion-USD post-pandemic fiscal packages continue to ensure solid economic growth. The high level of interest rates will have a dampening effect on the economy. However, the stock markets will be positively supported by further falling inflation rates and rising corporate profits.

Dr. Patrick Huser, CEO

Sources: Trading Economics, US Bureau of Labor Statistics, Statista, FuW, IMF World Economic Outlook October 2023, FactSet, FMOC

As of 14.11.2023

China

Acceleration in the 3rd quarter

Economic growth accelerated again in the 3rd quarter and improved by 1.30% compared to the previous quarter. It was not only government infrastructure spending that contributed to this. Foreign trade and private consumption also improved towards the end of the quarter. Domestic tourism is slowly recovering and the initial figures for October are encouraging. The central government has once again increased the budget deficit for the current year in order to support the economy in the face of continued weak consumer confidence. Over the years, the Chinese government has implemented various instruments and strategies to stimulate the economy and promote sustainable growth. Some key areas include promoting technological innovation, investing in infrastructure, green energy and its targeted foreign policy.

IMF Economic Forecast

GDP 2023: 5.00%

Inflation 2023: 0.70%

3 months shibor: 2.45%

Our conclusion:

An increase in infrastructure spending and selective monetary policy measures by the central bank could also help to achieve positive economic growth at the end of the year. However, the geopolitical situation is too uncertain to invest in the rather cheaply valued Chinese equity market.

Sources: Allianz, ZKB, IMF

As of 13.11.2023

Japan

Further gains possible in Japan

For a long time, the Japanese stock market was uninteresting for many investors, but this has changed over the course of the year and more and more institutional and private investors have rediscovered the market for themselves.

There was a price recovery after the pandemic, as in many other markets. However, this was followed by flat markets until a new upward trend followed this spring. This was facilitated by several factors. Firstly, loose monetary policy was responsible for this, even though some tightening measures were recently announced. Some analysts expect the negative interest rate to be abolished as early as the first few months of 2024. Inflation accelerated unexpectedly in October. Secondly, encouraging business results, often above expectations. At present, forecasts are being revised upwards rather than downwards. In addition, companies often have a good cash cushion and a lower debt ratio than in other countries. Finally, the economy is also very solid. The proximity of the Japanese market to China also has a favorable effect. However, Japan is exposed to less political risk. Geopolitical tensions make Japan a "safe haven" in Asia at the moment.

GDP 2023: +1.60%(E)

Inflation 2023: +1.60%(E)

3 Month Tona Rate: -0.03% m

Conclusion: Still positive

Japan is still undervalued, cheap and underrepresented in globally oriented portfolios. The market offers a good opportunity for medium-term investors. Even if the potential is lower than at the beginning of 2023. The currency must be taken into account when investing.

Mimi Haas, Lic. rer.pol. HSG, M.A. in Banking and Finance HSG, Partner

Sources: F&W, JP Morgan and Bloomberg

As of 14.11.2023

Emerging Markets

Opportunity and risks

The sharp rise in US government bonds has put emerging market currencies under pressure. Since late summer, most currencies have lost value against the USD. This has led to higher import prices, rising inflation and increased payment obligations for foreign debt. For this reason, the Indonesian and Philippine central banks have unexpectedly raised interest rates. The situation is different in Latin American emerging markets such as Mexico and Brazil: inflation rates have been falling for months, allowing central banks to lower interest rates and thus promote economic development. Structural reforms and efforts to improve the investment climate are at the heart of Brazil's political agenda in order to promote long-term growth and competitiveness. Mexico is benefiting from US industrial reshoring efforts by taking strategic measures to attract further investment and relocation of production. The favorable geographic location, a good trade agreement and low labor costs are the foundation for a solid economic starting position.

Our conclusion:

Emerging market equities are currently generally favorably valued. Due to the different economic starting positions and the increasing geopolitical risks worldwide, the markets of Mexico and Brazil appear particularly attractive compared to Asian countries. Brazil stands out as a major exporter of raw materials and agricultural goods, while Mexico is benefiting from extensive investment projects by US industry.

Sources: ZKB, IMF

As of 14.11.2023

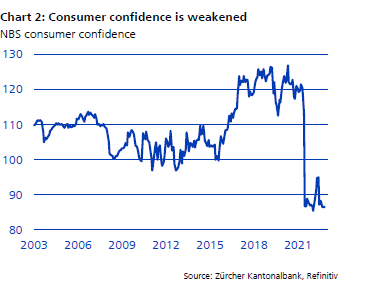

Stocks

Is this the turning point?

The latest estimates from the International Monetary Fund (IMF) in October showed that Europe is not expected to see any noticeable economic growth until 2024. In Asia too, outside of Japan, there is more of a lull compared to the previous economic momentum. Only in the USA is growth exceeding the modest expectations of April. On the other hand, inflation is forecast to fall globally, raising hopes of an imminent turnaround in interest rates and lending some optimism to the stock markets until the next cautionary words from central bank governors. In fact, the stock market seems to be so strongly influenced by interest rate developments that geopolitical issues play at most a secondary role.

The Federal Reserve's monetary policy tightening over the past 16 months will continue to have repercussions. While corporate profits in the US are recovering, the outlook for new hiring is weakening. US employment in October grew at only half the rate of September. More importantly, the average pace of hiring for the full year 2023 was only half that of 2022. The Fed typically eases when unemployment is low and inflation is above target. We therefore assume that the Fed's rate-cutting cycle will begin in early 2024. The European Central Bank (ECB) routinely lags behind the Fed in both rate cuts and rate hikes. This could be one reason why the valuation of European equities is significantly lower than that of US stocks. Some US brokers have recognized this as an opportunity and are recommending a higher weighting in European equities.

Our conclusion:

The last quarter was characterized by negative sentiment. We believe this pessimistic stance is exaggerated. Although we assume that the equity markets still have to contend with headwinds, equity markets tend to anticipate changes early on. The higher short-term interest rates still offer a good alternative to equity investments, but they will soon fall. Our CAIB index shows a narrow upside for equities of 53% in the short term and 57% in the long term (on a scale of 0-100%). We therefore recommend buying European and Swiss quality stocks.

Sources: S&P, Citigroup, MarketMap, IMF, and Chefinvest

As of 14.11.2023

Interest

Bonds bring balance and yield to your portfolio

The world's most important central banks held their interest rate meetings last September. The results were very different.

In the USA, the FED left its key interest rate at 5.5% at its meeting. Switzerland followed the same path a few weeks earlier, surprising the market. The key interest rate is 1.75%. With its monetary policy, Switzerland has so far been able to effectively prevent inflation from skyrocketing, as in other countries. However, it has indicated that further measures will be taken if necessary.

The ECB also agreed within the October meeeting to leave the key interest rate at 4.5%, after rasing the rate in September.

The messages from the central banks are clear, however: key interest rates are about to peak. The key question now is when they will be lowered again. Opinions differ here and will depend on developments over the next few months.

Government bonds

Nominal yields on global government bonds remain attractive, which was mainly due to real interest rates and surprisingly solid economic data. These bonds offer a good mix of yield and stability. Although we now expect a soft landing for the US economy, there is likely to be a slowdown in growth over the next few quarters as tighter lending and financing conditions begin to impact economic activity. In addition, the expected persistent inflation situation suggests that the rate hike cycle is coming to an end.

Our conclusion: We are positive on global high quality government bonds.

Investment grade bonds (IG)

The rise in global IG bonds was supported by surprisingly good economic data. Spreads narrowed to expensive levels, while yields remained attractive. In our soft landing scenario, global IG bonds should offer attractive returns going forward as economic growth and inflation slow while yields have settled at high levels. However, we would now advise investors to extend the duration of bonds, even if yields are lower than at the lower end, to capture the consistency of returns for the longer duration.

Our conclusion: We remain positive on investment grade (IG) bonds and favor bonds with a good credit rating and longer duration.

High yield bonds (HY)

The default risk on HY bonds has increased with the market development and there is a risk of a further rating downgrade. The higher coupons do not compensate for this additional risk.

Our conclusion: We see this segment as less attractive for new investments, and we would recommend holding existing positions.

Emerging markets bonds (EM)

EM offer a yield premium for a higher default and currency risk. As a result of the robust US economic data, hard currency bonds from the emerging markets once again posted a positive performance. However, the rise in US Treasury yields, disappointing economic data from China and the widening of spreads in August offset these gains.

Our conclusion: This is why we tend to be neutral on this sub-class of bonds.

Mimi Haas, Lic. rer.pol. HSG, M.A. in Banking and Finance HSG, Partner

Sources: F&W, JP Morgan and Bloomberg

As of 14.11.2023

Currencies

Currencies continue to be influenced by the different interest rate levels

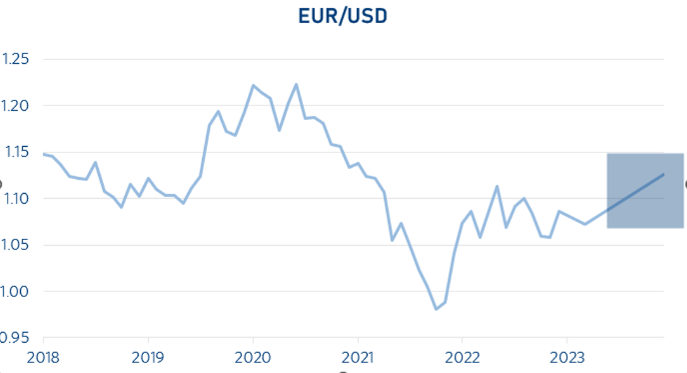

EUR/USD (14.11.2023: 1.07)

The movement of the currency pair was very volatile in 2023. This is due to the fact that the USA has much higher interest rates than the eurozone. But it is also further advanced in the cycle.

Our conclusion: We expect the dollar to weaken slightly.

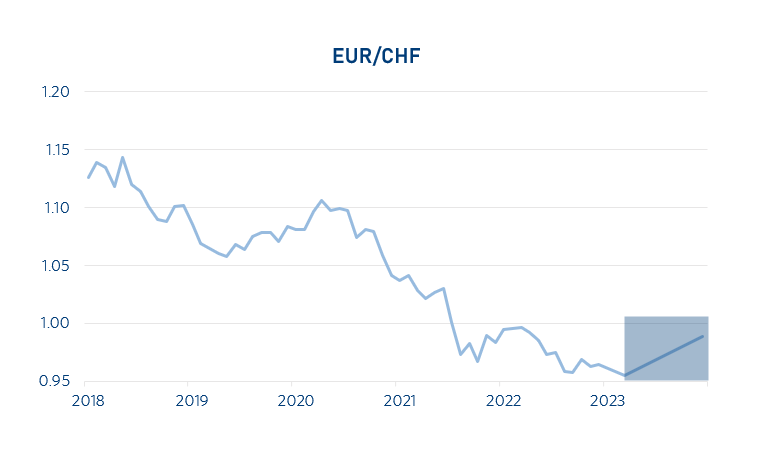

EUR/CHF (14.11.2023: 0.97)

The franc has outperformed all leading currencies in 2023. The main reason for this is the SNB's restrictive monetary policy. Switzerland's inflation profile is more favorable than that of the US and Europe. Interest rates remain low, but can be raised by the SNB if necessary. We do not see any potential for these to be lowered in the coming months.

Our conclusion: We expect the currency pair to move sideways.

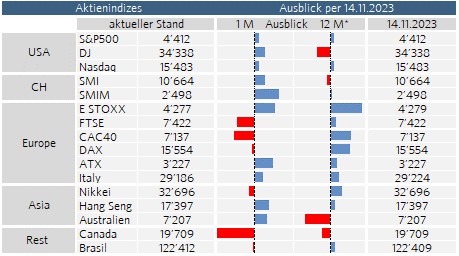

USD/CHF (14.11.2023: 0.90)

Inflationary pressure and the development of interest rates have an impact on currency developments. The interest rate differential between the two currencies is enormous, both central banks decided not to raise interest rates in September, so the decisive factor will be who lowers interest rates first.

Our conclusion: We expect the USD slightly lower against the CHF.

Mimi Haas, Lic. rer.pol. HSG, M.A. in Banking and Finance HSG, Partner

Sources: F&W, Market Map and Bloomberg

As of: 14.11.2023

Oil

Peak in oil consumption?

The term peak oil has so far been used to describe the supply-side peak in oil production. According to the International Energy Agency (IEA), however, the consumption of fossil fuels (oil, gas and coal) will now decline worldwide from 2030 onwards - on the demand side. After all, the IEA estimates that fossil fuels will still account for 73.00% of the global energy mix in 2030 (currently 80.00%) and will therefore remain an important factor in energy supply for a long time to come.

Despite the geopolitical tensions in the Middle East, the WTI oil price is currently trading at just under USD 80 again, which is well below the September high and is positive for inflation.

Our conclusion:

We expect WTI oil to move in the new range between USD 75.00 and USD 95.00 per barrel.

Dr. Patrick Huser, CEO

Sources: F&W, MarketMap,International Energy Agency (IEA)

As of: 14.11.2023

Precious Metals

Gold and platinum - hold

During geopolitically uncertain times, precious metals represent a safe haven and balance the portfolio accordingly. Central banks are continuing to buy gold, while demand for platinum is stagnating due to continued high US interest rates and falling car sales. Gold is currently trading at USD 1,972/oz. and platinum at USD 896/oz.

Our conclusion: Neutral

Unrest in global politics and still high interest rates are keeping gold at a high level, while platinum remains slightly in the shadow of gold. Both platinum and gold should remain in portfolios for diversification purposes.

Andreas Betschart, Business Manager

Sources: UBS

As of 11.11.2023

Abbreviations and explanations

bbl: 1 Barrell = 158,987294928 Litre

Bp: Basis points

GDP: Gross domestic products

BIZ: the Bank for International Settlements is an international financial organization. Membership is reserved for central banks or similar institutions.

EM-Bonds: Emerging market bonds. An emerging market is a country that is traditionally still counted as a developing country but no longer has its typical characteristics.

HY-Bonds: Fixed-income securities of poorer credit quality. They are rated BB+ or worse by the rating agencies.

IG-Bonds: Investment grade bonds are all bonds with a good to very good credit rating (Ra-ting). The investment grade range is defined as the rating classes AAA to BBB-.

IHS Markit: Listed data information services company

IWF: The International Monetary Fund (also known as the International Monetary Fund) is a legally, organiza-tionally, and financially independent specialized agency of the United Nations headquartered in the United States of America.

KOF: Business Cycle Research Centre at ETH Zurich

LIBOR: London Interbank Offered Rate is a reference interest rate determined in London on all banking days under certain conditions, which is used, among other things, as the basis for calculating the interest rate on loans.

OPEC: Organization of the Petroleum Exporting Countries

OPEC+: Cooperation with non-OPEC countries such as Russia, Kazakhstan, Mexico and Oman.

oz: the troy ounce is used for precious metals as a unit of measurement and is equal to 31.1034768 grams

Saron: The Swiss Average Rate Overnight is a reference interest rate for the Swiss franc

Seco: Swiss State Secretariat for Economic Affairs

Spread: Difference between two comparable economic variables

WTI: West Texas Intermediate. High-quality US crude oil grade with a low sulfur content.

Disclaimer:

The information and opinions have been produced by Chefinvest AG and are subject to change. The report is published for information purposes only and is neither an offer nor a solicitation to buy or sell any securities or a specific trading strategy in any jurisdiction. It has been prepared without regard to the objectives, financial situations or needs of any particular investor. Although the information is derived from sources that Chefinvest AG believes to be reliable, no representation is made that such information is accurate or complete. Chefinvest AG does not assume any liability for losses resulting from the use of this report. The prices and values of the investments described and the returns that may be received will fluctuate, rise or fall. Nothing in this report is legal, accounting or tax advice or a representation that any investment or strategy is appropriate to personal circumstances or a personal recommendation for specific investors. Foreign exchange rates and foreign currencies may adversely affect value, price or yield. Investments in emerging markets are speculative and involve considerably greater risk than investments in established markets. The risks are not necessarily limited to: Political and economic risks, as well as credit, currency and market risks. Chefinvest AG recommends investors to make an independent assessment of the specific financial risks as well as the legal, credit, tax and accounting consequences. Neither this document nor a copy of it may be sent in the United States and/or in Japan and they may not be handed over or shown to any American citizen. This document may not be reproduced in whole or in part without the permission of Chefinvest AG.