Click on the images to view our comments on each topic.

Switzerland

With Optimism ahead

The Swiss economy proved resilient in the third quarter. Industrial production increased strongly and private consumption remained at a high level.

The inflation rate has come off its highs and was around 3.0% in October, which is low by international standards. However, it is above the price stability target of 2% set by the Swiss National Bank. Therefore, another key interest rate hike is expected in December. The SNB was able to slightly reduce the accumulated foreign currency reserves in the past quarters and thus avoid a weakening of the Swiss franc, which reduces import inflation. As a small, open economy, Switzerland cannot escape the difficult international environment. SECO's expert group for economic forecasts lowered its growth forecasts for Switzerland significantly to 2.0% in 2022 and to 1.1% in 2023.

The inflation rate for 2023 is forecasted at 2.4%. Private consumption as well as the service and pharmaceutical sectors will contribute to the economic momentum. Construction activity, on the other hand could slow down as a result of higher interest rates. The unemployment rate will remain at a record low level.

SECO economic forecast

GDP 2022: +2%

Inflation: +3%

SARON 3 Mt.: +0.45%

Our Conclusion: Positive

The energy crisis in Europe is also leaving its mark on Switzerland, but no recession is expected. The companies are producing at the limits of their capacity and were able to deliver pleasing results for the third quarter. All in all, the expectations of analysts were beaten. Swiss shares are currently trading slightly below their historical average price and offer long-term potential.

Source: OECD and SECO

European Union

Lower growth and higher inflation

Real GDP growth in the European Union (EU) surprised on the upside in the first half of 2022. The expansion continues in a significantly weakened form in the third quarter. Seasonally adjusted gross domestic product (GDP) rose by 0.2% in the third quarter of 2022 in both the EU and the Euro area. Compared to the same quarter of the previous year, this means an increase of 2.1% in the Euro area and 2.4% in the EU.

The labour market continued to perform well despite the difficult environment. Due to strong economic growth in the first half of 2022, two million net additional jobs were created in the EU and the number of people in work rose to an all-time high of 213.4 million. In September, it was at a record low of 6.2%.

In October the overall inflation rate in the Eurozone reached a new high of 10.7% and grew above the 10.0% mark for the first time since the introduction of the Euro. As in the previous months, energy prices in particular increased by 41.9%. Prices for industrial goods excluding energy climbed by 6.0% and for services by 4.4%. In November, inflation could lose some of its momentum for the first time in a long time and inflation in the Euro zone should exceed its peak in the near future.

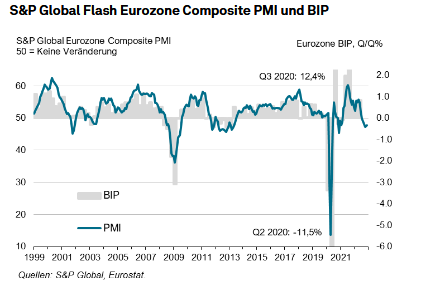

Economic output in the Eurozone fell for the fifth month in a row in November. However, the decline slowed due to reduced order losses, easing supply bottlenecks and an improved business outlook. The S&P Global Flash Eurozone Composite PMI currently stands at 47.8 points, down from 47.3 in October and below the neutral growth threshold of 50 points for the fifth month in a row. However, it signals a slightly weaker decline in economic output in the Eurozone.

Current inflation (ECB/HICP) + 10.7% (10.22)

Current 3 month Libor + 1.922% (E)

IP growth 2022 + 3.2% (E)

Our Conclusion: Positive

The strongest labour market in decades in the EU will remain resilient. However, labour markets are expected to react with a lag to the slowdown in economic activity. EU employment growth is projected at 1.80% in 2022, before stalling in 2023 and moderating to 0.4% in 2024. The unemployment rate is projected at 6.20% in 2022, 6.5% in 2023 and 6.4% in 2024.

In the first ten months of 2022, inflation has been higher than expected and the EU Commission has raised the annual inflation forecast to 9.3% in the EU and 8.5% for the Euro area. The strong price increases will be partly offset by high special government spending and the latest wage settlements. For the coming year 2023, inflation is expected to fall to 7.0% in the EU and 6.1% in the Euro area. In 2024, it is expected to slow to 3.0% and 2.6%.

The Governing Council decided in October to raise the three key interest rates by 75 basis points each. The interest rate for the main refinancing operations as well as the interest rates for the marginal lending facility and the deposit facility were raised accordingly to 2.00%, 2.25% and 1.50%, respectively, with effect from 1 November.

Monetary tightening is now expected to ease and the probability of an ECB rate hike of only 50 basis points in December has recently increased. A recession is approaching, but some of the bad economic news from previous months now seems clearly exaggerated (easing of the supply chain situation and reduced risk of energy rationing).

Due to the strong growth in the first half of the year, real GDP growth should rise to 3.3% in the EU (3.2% in the Euro area) in 2022. This is well above the 2.7% forecast in the summer forecast. The strong headwinds and major uncertainties that continue to hold back demand will further dampen economic activity in the coming months, so that GDP growth in 2023 is expected to reach only 0.3% overall in both the EU and the Euro area. Economic growth is expected to gradually pick up by 2024, averaging 1.6% in the EU and 1.5% in the Euro area.

Daniel Beck, Member of the Executive Board

Source: European Commission, Statista and S&P Global

United Kingdom

USA

Inflation has peaked

The S&P Global overall Purchasing Managers' Index (Composite PMI) for the USA fell to 46.30 points in November (October 48.20). Above all, the sharp decline in new orders shows that the economic slowdown expected due to higher interest rates is beginning to take hold. Index values below 50 signal a shrinking economy in 6 months. On the positive side, input price components have declined and managers' expectations for future business performance have increased.

As expected, the US economy grew again in Q3 2022 at an annualised rate of +2.6%. In Q2, it had still declined by 0.6%. For the 4th quarter, the SPF (Survey of Professional Forecasters) November 2022 still expects annualised growth of +1.0%. For the next year, the economy is expected to grow only minimally in the first two quarters (+0.2%), but in the second half of the year growth rates of +0.9% in the third quarter and +2.1% in the fourth quarter are expected.

After the inflation in June this year when USA reached a high of 9.1%, it has gradually eased in the recent months and in October it was still +7.7% (core inflation excluding food and energy was +6.2%). The strong interest rate hikes by the US Federal Reserve (last time to 4.0% in November) are beginning to take effect. The peak of short-term interest rates (Fed Fund Rate) in this hike cycle, which is expected in the first quarter of 2023, is now at 4.75-5.0%. Based on this development, the majority of market participants currently expect the Fed Fund Rate to be raised by 'only' 0.5% to 4.5% at the next Fed meeting on 14 December. However, the inflation figures for November, which will be published on the 10th of December, may still change expectations in this regard. For 2022, the SPF expects average inflation of +7.7% and +3.4% for 2023 (core inflation +6.3% in 2022 and +3.5% in 2023).

In the third quarter of the current year, 69% of S&P 500 companies did beat earnings expectations and 71% the sales expectations, according to FactSet. Profits thus grew by only +2.2% compared to the same quarter last year (compared to +3.5% expected in September). Earnings are expected to decline -1.1% in Q4 and to grow modestly by +2.3% and +1.5% in Q1 and Q2 2023, and will return to high single-digit growth in the second half of the year. As a result, the price/earnings ratio of the S&P 500 based on expected earnings for the next 12 months has risen to 17.2, which is still below the five-year average of 18.5 and just above the ten-year average of 17.

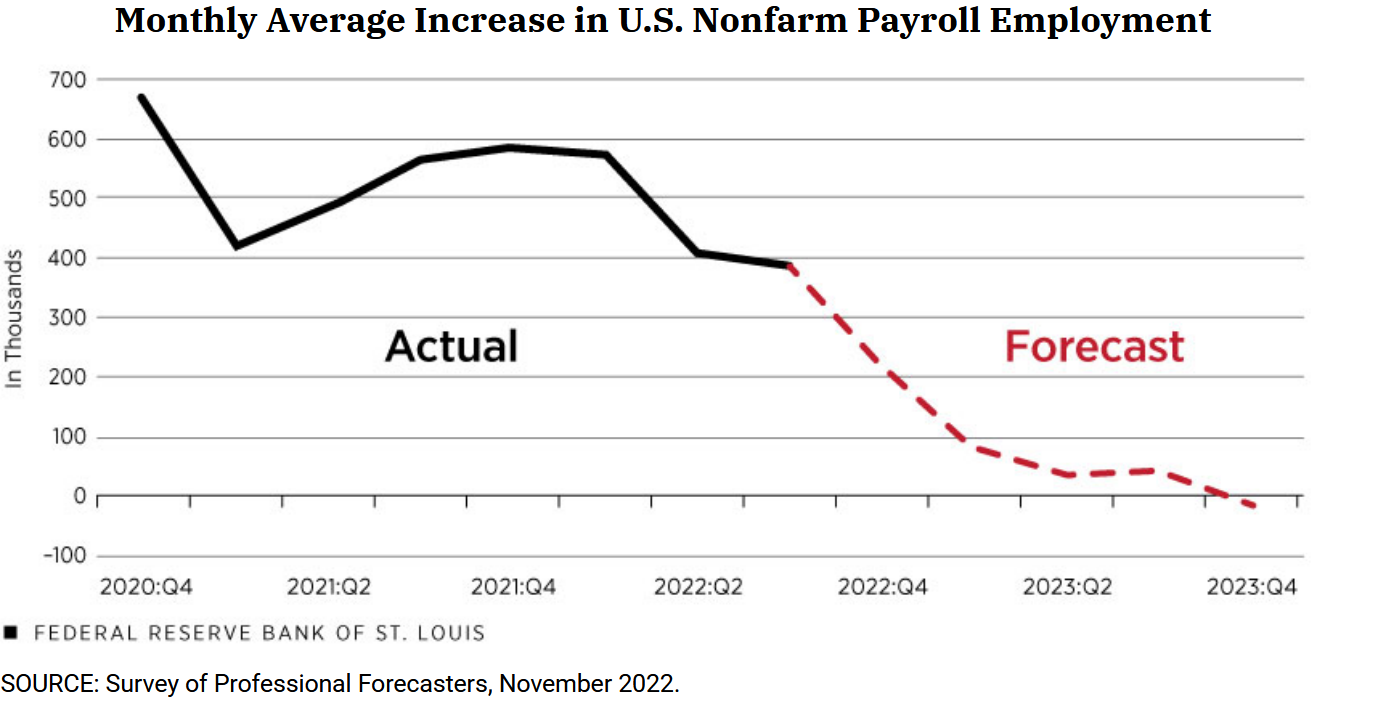

The November labour report will provide further insight into whether the interest rate hikes of recent months have already managed to cool the overheated labour market. At the end of October, unemployment was still at a historically low 3.7% and the number of job openings was 10.7 million. The SPF expects no new jobs to be created in Q4 2023.

Fed Fund Rate: +4.0%

BIP 2022(IWF): +1.6%

Inflation 2022 (SPF): +7.7%

Our Conclusion: Neutral

We expect that due to the restrictive monetary policy, inflation figures will continue to fall substantially next year and that the Fed will start to ease fiscal policy again from mid-2023. The current price level already anticipates a slight recession in the first half of the year. However, due to the persisting inflation and growth uncertainties, markets are likely to remain volatile in the coming weeks. As soon as the inflation figures clearly recede, a further market recovery is to be expected.

Source: Statista, Survey of Professional Forecasters and FactSet

China

New government orientation

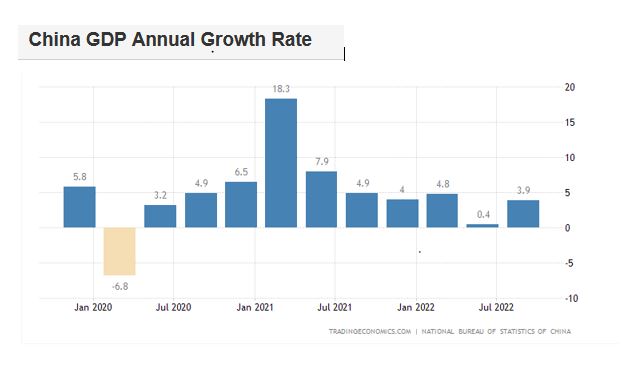

An unfavourable environment has characterised China throughout the year. The strict Corona policy has made economic development considerably more difficult. In addition, the upheaval in the real estate sector has intensified. Higher global energy prices have also translated into weaker external demand. These factors have slowed China's GDP growth and it is expected to be well below 5.0% this year, far short of expectations. The IMF is forecasting growth of only 3.2%.

The party congress in October marked a change in economic policy. In several industrialised countries, a transition from just-in-time to just-in-case can be observed, which is due to the instability of supply chains in the context of the lockdowns. On the other hand, the US and its allies consider of China as a rival and are increasingly pursuing protectionist trade policies. China is therefore trying to gear its economy more towards domestic demand. For its five-year plan, the strategy of dual circulation was developed, in which the domestic and foreign economies are promoted equally. The People's Bank of China, unlike Western central banks, will continue to ease monetary policy to support the economy. The Renminbi exchange rate will continue to depreciate slightly against the USD, supporting export activity.

IMF economic forecast

GDP 2022 +3.20%

Inflation +2.20%

Shibor +2.18%

Our Conclusion: Negative

The effects of the rigorous Corona policy and the turbulence in the real estate sector are slowing down economic development. The new appointment to the political office in October signals that the state will again play a bigger role in the Chinese economy in the future. GDP growth of 5.0% for 2023 therefore seems very ambitious. The low valuation of the equity markets reflects the major political risks. We do not recommend making any new investments at the moment.

Dino Marcesini, Partner

Source: IMF and LLB

Japan

Under positive omens!

Covid, the political crisis, and the reform backlog should slowly be over. For decades, the third-largest economy has been characterised by deflationary tendencies and a perceived economic stagnation. In contrast to the rest of the world, the Japanese central bank (BoJ) is therefore sticking to its expansionary monetary policy. Inflation, which at 3.0% is comparatively low, is welcomed in Japan. It is consciously accepted that the Yen will depreciate strongly. The currency has lost almost 25% against the USD since the beginning of the year.

Japan is a country with few natural resources and therefore has to import both food and other raw materials from abroad. In the past, this circumstance prompted the country to open up to global trade early on and to become one of the first major export nations in the world. The country is considered a driver and pioneer of technological progress, and focuses on mega trends such as robotics, hydrogen and artificial intelligence.

The Japanese government has also requested and approved a special budget of more than USD 198 bn in recent weeks, which according to F&W is about 5.3% of Japan's GDP. These measures are intended to secure domestic demand for years to come.

The environment (low interest rates, more expansionary monetary policy, a fiscal package and a weak Yen) is positive for the stock market and the economy. Japanese equities have corrected only slightly compared to other indices in 2022. Japanese corporate balance sheets are in good shape and the corporate reporting season was satisfactory, with net profits alone slightly below analyst expectations.

GDP 2021 USD 4.9 bn.

Inflation October 2022 3.7%

Japanese key interest rate -0.1%

Our Conclusion: Positive

The country should be slowly emerging from its crises and offers investors a good opportunity to diversify a portfolio.

Mimi Haas, Lic. Rer.pol. HSG, M.A. in Banking and Finance HSG, Partner

Sources: F&W, Reuters and Bloomberg

Emerging Markets

Differing speed

India is the second largest economy after China in the emerging market equity indices. The Indian economy benefited this year from a rapid lifting of the Covid measures. As a strategic trading partner of Russia, India can purchase oil and gas at large discounts, which has a dampening effect on the inflation trend. In addition, the country is emerging as a winner in the planned diversification of production, which is being pursued by international companies. The expansion of the industrial sector will accelerate economic momentum. Among the large emerging markets, India will have the strongest economic growth. The experts expect an expansion rate of 6.0% for next year after 6.8% for 2022.

Latin America navigated inconspicuously through the turbulent global economic environment this year. Key interest rates have already been raised substantially. This year's annual average inflation rates of around 8.0% in Mexico and 9.5% in Brazil can be compared with the data from the USA and Europe, with a clear downward trend particularly in Brazil. This should give the central bank leeway to lower key interest rates as early as 2023.

Our Conclusion: Neutral

India is taking advantage of the geopolitical tensions for cheap energy imports from Russia. The country should benefit as a location for internationally active companies, which are driving the diversification of production facilities. Economic growth will remain dynamic. In Latin America, Brazil benefited from high commodity prices this year, which will not be repeated in 2023. Lula, elected in autumn, will take office on 1.1.2023 and become president for the third time. However, there are no great hopes for economic reforms. The IMF expects GDP growth of only 2.0% for the next few years. Brazil should therefore be underweighted.

Dino Marcesini, Partner

Sources: IMF and LLB

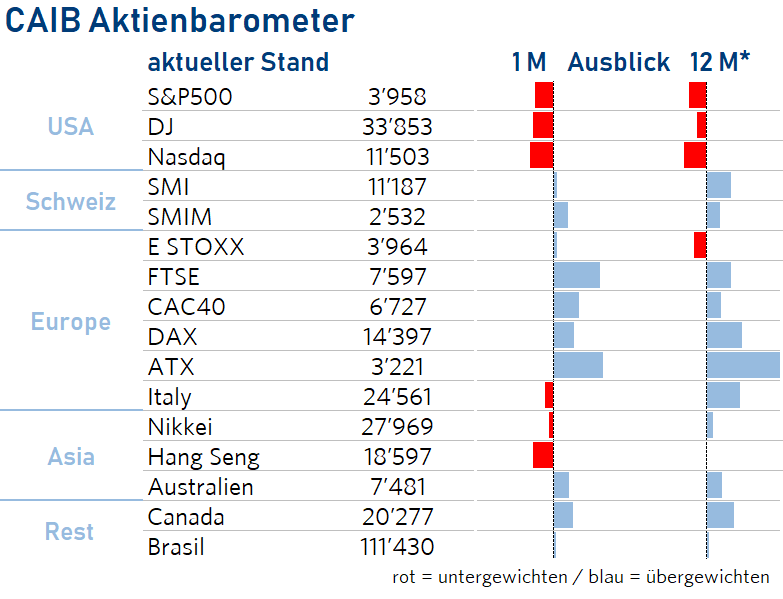

Stocks

Do the bulls prevail again?

There is currently a showdown war between bulls and bears. For many, it is a confusing market, full of hopes and fears. The question is not how perceptions change from month to month, but rather: is anything the Fed or the ECB is doing likely to prevent a slowdown in the economy? The bears are suspicious of this and fear rising interest rates due to the central banks' tightening monetary policy, the reduction of liquidity in the market due to the withdrawal of the Fed's and ECB's Quantitative Easing programmes and, above all, a prolonged recession. The bulls see the current high net pessimism rate of -22.0% (Haver Analytics). The recession is already expected and possibly already factored into prices, new hope for lower inflation since the last reports and share buyback plans due to low valuations of some companies as opportunities. Thus, the bears assess the recent stock rally as an interim bear rally and the bulls see themselves vindicated anyway.

The stock markets recovered strongly from the lows in October and November, with the EuroStoxx600 and the S&P rising by 15%. The driver was the surprisingly better US inflation figures and the fact that the economy is cooling down a bit after all and central banks will be less aggressive in implementing interest rate hikes. The recent layoffs in various industries are also seen as an additional cooling in the overheated sectors and are being taken positively for the time being. Large US tech companies are cutting staff after a year of rapid hiring and lavish spending due to pandemic-related growth. More than 25,000 tech employees were laid off in November, including at Meta, Amazon and Twitter, about twice as many as in October. US and European investment banks are also cutting jobs and slashing bonuses as advisory and underwriting revenues slump due to the slowdown in capital markets and M&A activity.

Our Conclusion: Slightly positive

In general, we are slightly positive on the equity markets in the short term and on a 12-month horizon. We favour the continental European stock markets, as they have a significantly lower valuation than the US stock markets and also have better competitive conditions on the world market due to the weaker currency.

However, economic and geopolitical headwinds such as the COVID 19 pandemic and the Russia-Ukraine war will continue to reshape global structures and relationships in 2023. Seven overarching themes, we believe, will shape the economic and risk environment next year: Establishing global security, resolving energy conflicts, re-aligning supply chains, reshaping labour markets, building affordable healthcare, improving environmental management and economic dissonance. In these areas, Western-oriented markets in particular will significantly increase their investments. Especially "green" investments are likely to come to the fore again.

Sources: S&P, Citigroup, MarketMap, IMF and Chefinvest

Interest

Revival: Traditional Role as Diversifier?

Government bonds

It is highly likely that central banks will raise key interest rates until the end of 2022. This behaviour will only change when inflation declines. Influenced by real interest rates, yields will continue their upward trend, albeit at a slower pace. Europe has slightly more room to tighten than the US.

Our Conclusion: Neutral

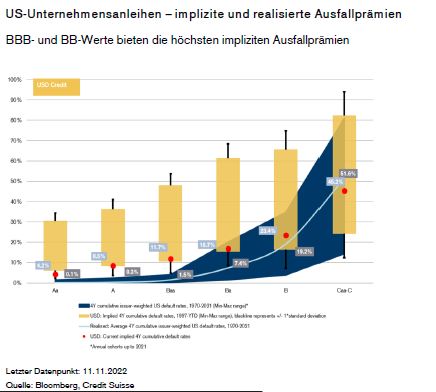

Investment grade bonds (IG)

Corporate bonds are now attractively valued again. For investors who want to take advantage of the attractiveness of European corporate bonds, these can be an interesting solution in USD. For riskier investors, credit securities rated BBB to BB are a good investment opportunity, as they have the best ratio of implied to realised default premiums. Furthermore, higher potential returns can be found in shorter maturities.

Our conclusion: Neutral. We are neutral on investment grade (IG) bonds at the moment. When investing in these securities, we recommend a shorter maturity.

High Yield Bonds (HY)

HY bond spreads are at levels seen in previous recessions. The asset class remains problematic as global growth risks, high inflation and continued higher policy rates as yield drivers slow demand for corporate bonds.

Our conclusion: Positive. HY bonds can be a good diversification in a bond portfolio. One should focus on a higher quality in the segment and a shorter duration.

Emerging Markets (EM) Bonds

EM offer a yield premium for higher default and currency risk. Robust fundamentals and the expectation that there will not be a severe recession support this asset class. The higher coupons of this asset class compensate the investor for the higher risk.

Our conclusion: Positive for riskier investors. We consider it interesting to invest in EM in hard currencies. To reduce the risk of default, ETFs should be considered and credit quality should be closely scrutinized.

Mimi Haas, Lic. Rer.pol. HSG, M.A. in Banking and Finance HSG, Partner

Sources: Reuters, IMF and Financial Times

Currencies

Safe haven, central banks and interest rates continue to influence

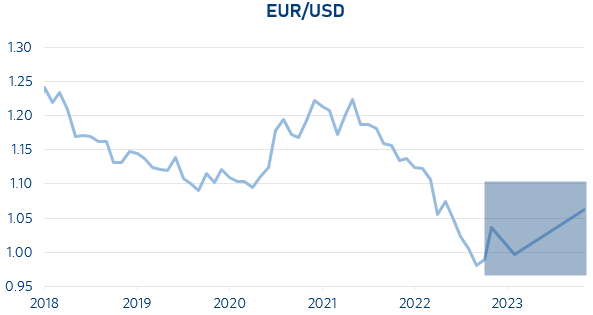

EUR/USD (01.12.2022: 1.05)

The USD has weakened slightly in recent weeks. Inflation figures in the US were unexpectedly good in November. This means that the FED will slow down the rate hikes. However, the key interest rate may still be higher in the USA and thus the interest rate advantage will continue.

Our conclusion: Neutral. The existing interest rate differential and the geopolitical situation continue to strengthen the dollar, but for next year it can be said that the further upside potential is limited.

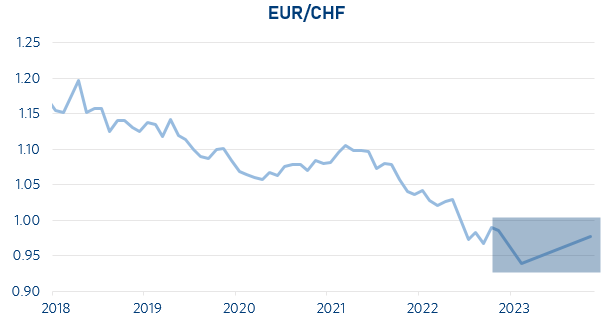

EUR/CHF (01.12.2022: 0.99)

The economic slowdown in the Eurozone will continue. No factor such as war in Ukraine, supply chain problems, has been solved. The Swiss National Bank has a greater potential to raise interest rates as the growth prospects in Switzerland are better than in the Eurozone. Switzerland has a solid current account surplus. The deteriorating environment further strengthens the franc as a safe haven asset.

Our conclusion: Negative. As long as the above scenario persists, the Swiss franc will remain strong; it may even appreciate slightly in the coming months.

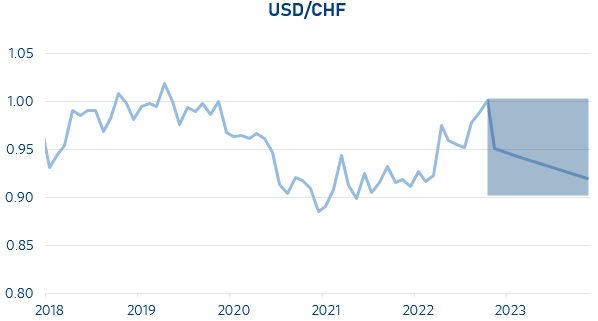

USD/CHF (01.12.2022: 0.94)

The USD has also weakened slightly against the CHF. Monetary tightening in the USA will certainly slow down. The interest rate in Switzerland has been positive again since this summer, but at a much lower level. This will not change in the coming weeks. The interest rate differential continues to lead to a slightly stronger dollar.

Our conclusion: Negative. This will continue to be the case.

Mimi Haas, Lic. Rer.pol. HSG, M.A. in Banking and Finance HSG, Partner

Sources: Market Map and Financial Times

Oil

Market forces prevailed over OPEC+

Despite OPEC+ cutting Oil production by 2 million barrels per day from November, the Oil price has fallen further to USD 80 per barrel of Brent Oil. This is mainly due to the weakening of the global economy and thus demand (especially from China), but probably also to the mild autumn temperatures so far. For the West, this development is welcome, as it contributes to further decreasing inflationary pressure. However, with the oil embargo against Russian Oil coming into force on 5 December, 1 to 3 million barrels of Russian Oil need to be replaced.

Our Conclusion: Neutral

We expect Oil prices to trend sideways over the winter months, but with further declines in Oil prices from spring 2023 due to falling demand.

Source: F&W

Precious Metals

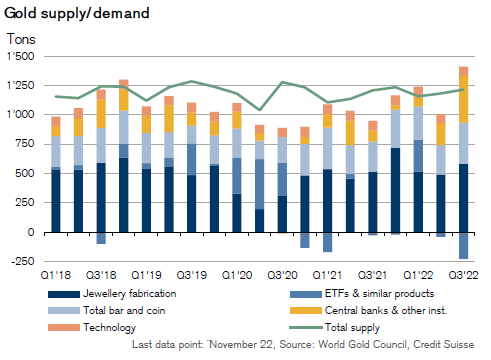

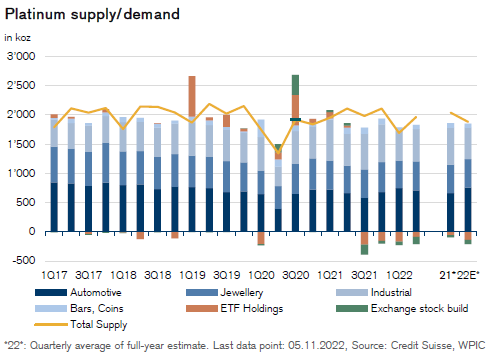

Rebound of gold and platinum

Gold has developed positively since the low of the year just above USD 1,600 oz. at the beginning of November. This is thanks to a certain recovery in the Chinese and Indian markets as well as in the Middle East. In addition, various central banks are again stocking up more strongly on the yellow precious metal.

Platinum has risen strongly in the 4th quarter and should be in the profit zone for this year. The shortage of South African production as well as an increase in car production are currently helping the precious metal.

Our Conclusion: Positive

The two precious metals remain interesting for diversification purposes and will continue to be a good asset in the portfolio in the future.

Andreas Betschart, Business Manager

Source: Credit Suisse

Abbreviations and explanations

bbl: 1 Barrell = 158,987294928 Litre

Bp: Basis points

GDP: Gross domestic products

BIZ: the Bank for International Settlements is an international financial organization. Membership is reserved for central banks or similar institutions.

EM-Bonds: Emerging market bonds. An emerging market is a country that is traditionally still counted as a developing country but no longer has its typical characteristics.

HY-Bonds: Fixed-income securities of poorer credit quality. They are rated BB+ or worse by the rating agencies.

IG-Bonds: Investment grade bonds are all bonds with a good to very good credit rating (Ra-ting). The investment grade range is defined as the rating classes AAA to BBB-.

IHS Markit: Listed data information services company

IWF: The International Monetary Fund (also known as the International Monetary Fund) is a legally, organiza-tionally, and financially independent specialized agency of the United Nations headquartered in the United States of America.

KOF: Business Cycle Research Centre at ETH Zurich

LIBOR: London Interbank Offered Rate is a reference interest rate determined in London on all banking days under certain conditions, which is used, among other things, as the basis for calculating the interest rate on loans.

OPEC: Organization of the Petroleum Exporting Countries

OPEC+: Cooperation with non-OPEC countries such as Russia, Kazakhstan, Mexico and Oman.

oz: the troy ounce is used for precious metals as a unit of measurement and is equal to 31.1034768 grams

Saron: The Swiss Average Rate Overnight is a reference interest rate for the Swiss franc

Seco: Swiss State Secretariat for Economic Affairs

Spread: Difference between two comparable economic variables

WTI: West Texas Intermediate. High-quality US crude oil grade with a low sulfur content.

Disclaimer:

The information and opinions have been produced by Chefinvest AG and are subject to change. The report is published for information purposes only and is neither an offer nor a solicitation to buy or sell any securities or a specific trading strategy in any jurisdiction. It has been prepared without regard to the objectives, financial situations or needs of any particular investor. Although the information is derived from sources that Chefinvest AG believes to be reliable, no representation is made that such information is accurate or complete. Chefinvest AG does not assume any liability for losses resulting from the use of this report. The prices and values of the investments described and the returns that may be received will fluctuate, rise or fall. Nothing in this report is legal, accounting or tax advice or a representation that any investment or strategy is appropriate to personal circumstances or a personal recommendation for specific investors. Foreign exchange rates and foreign currencies may adversely affect value, price or yield. Investments in emerging markets are speculative and involve considerably greater risk than investments in established markets. The risks are not necessarily limited to: Political and economic risks, as well as credit, currency and market risks. Chefinvest AG recommends investors to make an independent assessment of the specific financial risks as well as the legal, credit, tax and accounting consequences. Neither this document nor a copy of it may be sent in the United States and/or in Japan and they may not be handed over or shown to any American citizen. This document may not be reproduced in whole or in part without the permission of Chefinvest AG.