Click on the images to view our comments on each topic.

Switzerland

Solid economy

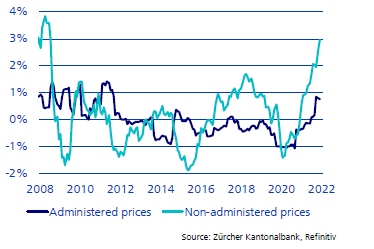

After dipping below the long-term average, the KOF Economic Barometer rises above it again in April. The important leading indicator for the Swiss economy increased from 99.2 to 101.7 points, thus exceeding analysts' expectations. The hospitality and other services sectors are responsible for this increase, while the indicators for foreign demand are slowing down the most. The unemployment is currently very low at 2.5%, which supports domestic consumption. The inflation rate has risen significantly in recent months, but remains modest by international standards.

An important reason for this is the energy mix, as a large part of Swiss energy consumption is based on hydroelectric and nuclear energy. In addition, administered prices have a high weight in the consumer price index. The costs of electricity, gas, public transport, medicines, doctors' and hospital services are regulated by the state. These prices are gradually adjusted upwards, but not abruptly. The return to negative inflation rates is unlikely for some time. This gives the Swiss National Bank the opportunity to herald an end to negative interest rates.

Inflation (KOF) +1.9%

3 Month Saron -0.71%

GDP (KOF) growth 2022 +3%

Our conclusion: According to the KOF economic forecast, the Swiss economy will grow by just under 3% this year - but only in the favourable scenario. If the Ukraine crisis spreads and there is a complete halt to all Russian energy and raw material exports, including to the EU, a withdrawal of trade in Russian crude oil from Switzerland and a significant appreciation of the Swiss Franc, GDP growth of only one percent would remain in 2022. The large, listed Swiss companies are solidly positioned and international leaders. The Swiss equity market remains attractive.

Status: 02.05.2022

European Union

Europe - Cautious recovery

According to initial estimates, seasonally adjusted gross domestic product (GDP) fell significantly below in the Eurozone by 0.2% and in the European Union (EU) by 0.4% in the Q1 of 2022. In Q4, GDP grew by 0.3% in the Euro area and by 0.5% in the EU.

Compared with the same quarter of the previous year, seasonally adjusted GDP grew by 5.0% in the euro area and by 5.2% in the EU in the first quarter of 2022, after +4.7% in the Euro area and +4.9% in the EU in the previous year and +4.9% in the EU in the previous quarter.

The Ukraine war, expensive energy prices, persistent supply bottlenecks and the slowdown of Chinese growth are shaking up the relatively open European economy considerably and have clouded the growth outlook. The thesis of the imminent spike in inflation, which has been repeatedly put forward since November last year, has not materialised. The overall inflation rate in the Eurozone rose to 7.5% in April. Such high inflation has not been seen in many places in since the 1980s.

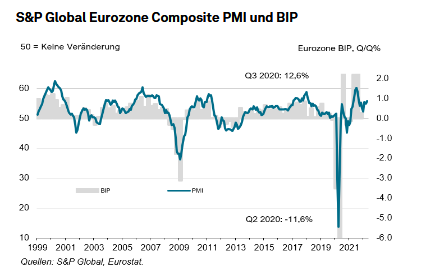

Eurozone economic growth accelerated again in April. The upswing in the service sector more than compensated for the near stagnation in industry. The S&P

Global Flash Eurozone Composite PMI rose 0.9 points to 55.8 - the highest level since last September. In particular, the higher increase in new orders points to an demand in the Eurozone.

Current inflation (ECB/HICP) + 7.5% (04.22)

Current 3-month Euribor - 0.429%

GDP growth 2022 + 2.8% (E)

Daniel Beck, Member of the Executive Board

Our conclusion: In its latest forecast, the IMF expects the Eurozone to grow by only 2.8% in 2022 - a downgrade of 1.1% from the January forecast. In Germany, the largest economy in Europe, GDP is now expected to grow by 2.1%, (1.7% less than assumed in January).

Encouragingly, the economic and sentiment indicators published since February clearly indicate a continuing economic recovery. Robust and broad-based growth is signalled by the purchasing managers' indices. Businesses remain confident and accumulated savings, growing employment, fiscal stimulus from governments and the lifting of Corona restrictions will support the service sector.

In the first quarter, it became apparent that the record inflation rates (7.5%) were a heavy burden on consumption. However, the inflation rate stabilised in April for the first time in a long time because energy prices stopped rising. If this trend continues in the coming months or inflation begins to fall slightly, this should have a positive effect on consumption.

The pressure on the European Central Bank (ECB) to accelerate monetary policy normalisation has once again increased significantly. ECB chief Lagarde has held out the prospect of raising interest rates in the Euro area in the summer. The multi-year experiment with negative interest rates should soon come to an end. Some economists now expect four ECB rate hikes in a row, starting in July. However, it is assumed that an interest rate of 1.0% will be the end of the line.

Status: 02.05.2022

United Kingdom

USA

Will Powell manage a soft landing?

The US Federal Reserve (Fed), as recently indicated by its Chairman, Jerome Powell, raised the benchmark Fund Rate by 0.5% to a target range of 0.75-1% at its 3-4 May meeting. The market expects further rate hikes in the next few meetings and a rate of 2.5% by the end of the year, which would correspond to a neutral level of the policy rate.

With inflation at 8.5% in March (April figures will not be published until around May 10th), which is a four decades high, the monetary authorities do not have any other choice. Although March is expected to mark a peak and inflation rates are expected to decline gradually in the coming months due to base effects, there is no reason to expect a significant slowdown in inflation. However, with 5.3 million unfilled jobs, the labour market is currently running too hot for a noticeable decline in inflation. The ongoing lockdowns due to China's zero-covid strategy and the related supply chain problems that are likely to persist in the near future are also not helping to ease price pressures. In addition, the Fed has announced that it will reduce the Fed's balance sheet, which expanded to USD 9 trillion during the pandemic, as of June by USD 47.5 billion and as of September by USD 95 billion per month. However, this will not to be implemented through sales, but by not reinvesting maturing securities.

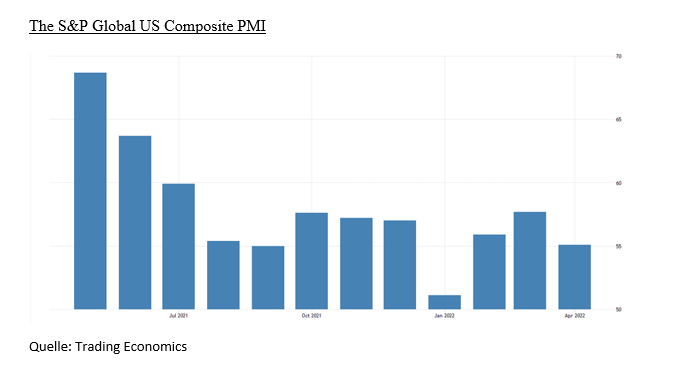

The S&P Global US Composite PMI for April 2022 was 55.1 index points, down 2.6 index points from the previous month. The slowdown was mainly due to the services sector. This means that the index value is still comfortably above the reference value of 50, which indicates an expanding economy in 6 months.

Of the 55% of S&P 500 companies that already published their Q1 2022 results, 80% reported higher-than-expected earnings per share and 72% reported higher-than-expected revenues. Average earnings growth was 7.1%, higher than the 4.7% expected at the end of March 2022. Based on expected earnings over the next 12 months, the price/earnings ratio of the S&P 500 is 18.1, 0.5 lower than the 5-year average and 1.2 higher than the 10-year average.

US GDP surprisingly fell 1.4% in Q1. This was mainly due to destocking and the widening trade deficit. Without these effects, GDP grew by 2.6%. In its April forecast, the IMF estimates US growth at 3.7% in 2022 and 2.3% in 2023. The pent-up consumption demand caused by the pandemic, as well as the historically high surpluses of private households, will give the economy positive impulses in the coming months.

Inflation 2022 (E) IMF: 7.6%

GDP 2022 IMF: 3.7%

Current Fed Fund Rate: 1%

Our conclusion: Uncertainties about inflation and a more restrictive monetary policy are pushing up risk premiums for equity investments. Economic growth remains robust and rising corporate profits support the current market valuation.

Status: 02.05.2022

China

Uncertainty prevails

In the first quarter, the economy grew slightly better than expected at 4.8%. However, rigorous Corona containment measures have led to major losses in recent weeks, so that the start of the second quarter has been unsuccessful. The PMI Composite Index, which tracks the overall economy, has fallen to 42.7 points and is at all-time lows. But unlike the Western economies, China is easing its monetary policy and thus has a different starting point. While interest rates are rising and the money supply is being reduced in the West, China can pursue an expansionary monetary policy. There is also no acute inflation problem as in the West, with core inflation hovering at a good 1% in March. As the world's largest importer of oil and agricultural goods, China cannot completely escape price developments, but the projected 3% inflation rates remain low by international standards. In the past two years, government spending has been limited and some reforms initiated. This year, the government has enough leeway to support the economy with various measures. Tax and fee cuts for businesses are being considered. Local governments are expected to increase spending on infrastructure projects. Loosening of restrictions in the real estate sector is also conceivable. The effects of the Omicron wave and the adherence to the zero-covid policy, together with the lockdowns, are hampering economic growth.

Our Conclusion: In the Ukraine conflict, China is taking a dangerous stance with its declarations of solidarity with Russia and causing great uncertainty among international investors. The economic impact is currently limited, as the country is only indirectly affected. Market observers still expect the economy to grow by just under 5% this year. Stock prices have already corrected sharply and valuations are low, reflecting the current high political risks.

Status: 02.05.2022

Japan

Positive trend in 2021, is it sustainable?

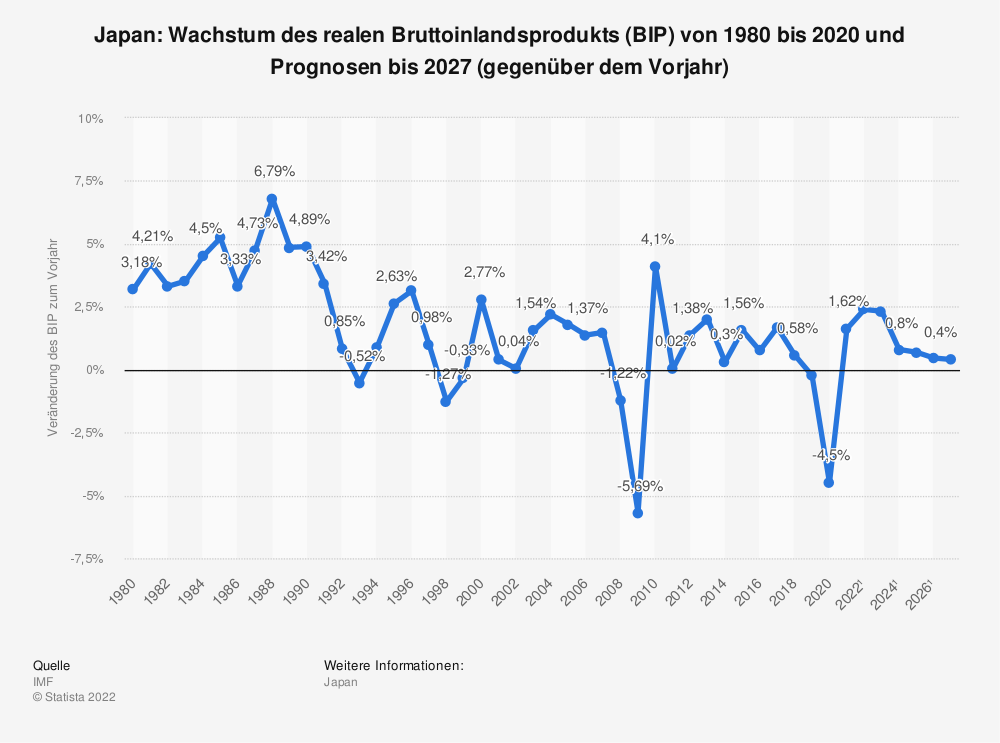

The IMF's forecast for real BIP growth in 2022 is 2.39% compared to 1.62% in 2021 and will fall again significantly after 2022. The strong growth in the two years is due to policy support in the form of a massive economic stimulus program worth about EUR 400 bn and the pandemic effect (high vaccination rates and catch-up effect for example in private consumption). Many parameters such as the weak yen (good for the economy), rising inflation expectations (Japan has been suffering from deflation for two decades) and a stock market that has fallen less than American and European stocks.

On the other hand, as in the rest of the world, this growth is threatened by the geopolitical situation and supply shortages. In addition, the new government will have to carry out far-reaching reforms to deal with the problems of recent years. To secure energy supplies, the Japanese government is sticking to projects with Russia and so far is not taking an alternative path. It will be exciting in the coming months to see which effect prevails and whether the IMF's forecast that the real BiP will fall again after 2023 is correct.

Mimi Haas, Lic. Rer.pol. HSG, M.A. in Banking and Finance HSG, Partner

Our conclusion: Based on the uncertainty described above, the Japanese stock market is not attractive for foreign investors at the moment.

Status: 02.05.2022

Emerging Markets

Unequal development

Consumer and business sentiment in the Eastern European region has deteriorated sharply, according to the latest surveys. The impact of the war in Ukraine will strongly affect economic data this quarter. The high level of uncertainty, higher interest rates and prices are reducing consumers' purchasing power to buy. Supply network disruptions and weakening new orders are weighing on the industry. Purchasing managers' indices in the emerging markets have also deteriorated, but are still in growth territory. Eastern Europe is suffering from the war in Ukraine. In Asia, China is hampering growth with its zero-covid strategy. The situation in Latin America, on the other hand, has improved. However, the high inflation rates are forcing most central banks to raise interest rates and thus tend to inhibit the economy.

Our conclusion: The strong USD is weighing on many emerging markets that have taken on debt in USD. Inflation rates are out of control in some countries, for example Turkey. Supply network disruptions, higher commodity prices and higher interest rates argue against exposure to emerging markets.

Status: 02.05.2022

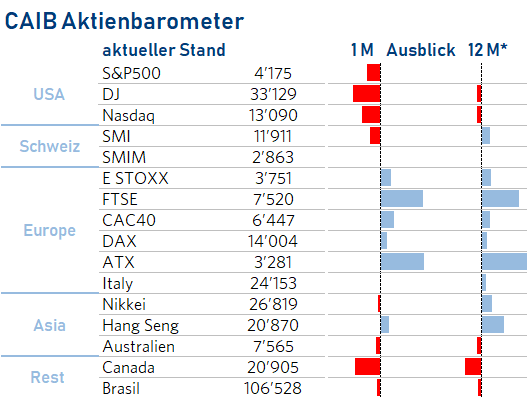

Stocks

Is there light at the end of the tunnel?

Equity markets in the US, Europe, China and Japan have posted double-digit losses so far this year, and in 2022 global equity markets have lost 13% in USD terms. In fact, under pressure from higher interest rates and slowing revenue growth, most of the technology stocks that drove portfolios higher in 2020 and 21 have fallen excessively. Recently, the US reported a 1.40% annualised decline in real GDP for the first quarter of 2022, the first decline since 2020. This decline is consistent with the results of e-commerce platforms (e.g. Amazon) and is therefore unlikely to be a coincidence.

For its part, the war in Ukraine is exacerbating inflationary pressures triggered by Covid. It is likely to lead to further shortages in the supply of commodities, from energy to agricultural products to rare metals. The news that Russia is stopping natural gas exports to its Eastern European trading partners will exacerbate the shortages and economic damage in the medium term. The urgency to replace gas imports with liquefied natural gas (LNG) is a case in point. These are challenging developments for the economy and for equity markets. There may nevertheless be some positives in all this: lower demand for goods and services and deeper trade flows than recently expected may lead to lower inflation and thus a more moderate Fed tightening cycle. This may coincide with the maintenance of economic growth. This would be a clear support for equity markets.Even with stable earnings expectations, PE multiples on the S&P 500 have fallen 15% over the past year. And if we look at valuations outside the US, current multiples are even in line with historical norms.

If investors can spot a stabilisation of interest rates and there is no recession, there is a possibility that equities will start to rally, especially among growth companies. Sectors such as fintech, clean energy, electric vehicles and biotech should then receive renewed attention due to their growth and long-term value creation. With the right buy timing, the significant sell-offs among industry leaders in these themes offer rare opportunities to take exposures at more reasonable valuations. Chinese equity valuations have already reached the historic lows of 2008 and offer limited downside risk at these levels. However, restoring confidence in the earnings prospects of Chinese companies requires several important conditions: These include an end to lockdowns, a further depreciation of the CNY against the USD and clarification that the political transition to the 20th Party Congress is on track. This could take until Q4 2022. Until then, valuations are likely to remain at alarmingly low levels.

Our Conclusion: Once interest rates peak, markets will stabilise and return to core issues (trends, environment, innovation). The inflation-calming measures should now be weakened. Our model (CAIB) shows a slightly positive overall and short-term trend of +0.03 at this level with a range of -1 and +1. On a 12-month basis, the CAIB shows a more positive opportunity profile of +0.10. In the short term, we favour stocks with a higher dividend that can be maintained or increased in subsequent years, as well as stocks that correspond to the value strategy. With a 12-month view, we advise buying the growth stocks of industry leaders that have been exposed to a sell-off this year. In both the short and long term, we see an increase in opportunities in European stocks due to the low valuation.

Status: 02.05.2022

Source: Chefinvest AG, Zurich, Market Map

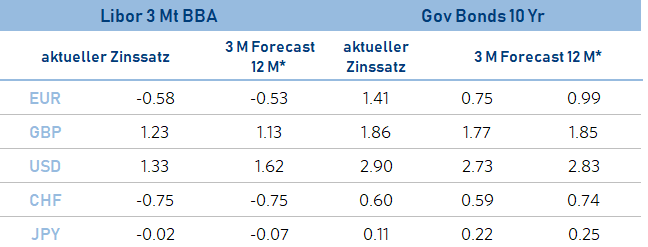

Interest

Bonds: Inflation and conflict in Ukraine weigh

Government bonds (unattractive)

Geopolitical uncertainty persists. But high global inflation and the post-COVID-19 recovery should lead to higher nominal benchmark yields in many regions over time. The US Federal Reserve has made it clear that it is prepared to raise interest rates aggressively to contain inflation. Many other central banks are moving in the same direction. Higher real yields pose a significant risk to bonds and other markets.

Our conclusion: The Fed still has room to raise rates. It may be forced to accelerate the pace of tightening due to the solid growth outlook and high inflation. Hence short duration. In Europe and Switzerland, growth is more affected by the conflict in Ukraine. Interest rates have already risen sharply since the beginning of the year.

Investment grade bonds(neutral)

However, this robustness in spreads does not mean an immediate return to spread tightening. The concern is still the extreme risk of accelerated liquidity withdrawal combined with weak growth expectations and geopolitical uncertainty. This could trigger a widening of credit spreads, e.g. a rise in the yield of US BBB securities to over 250 bp. Selected domestically-oriented European IG hybrid bonds with short-term maturities and defensive US credit securities are likely to be more resilient.

Our conclusion: Geopolitical risks increase volatility, so we rate this segment neutral.

High-yield bond(neutral)

We maintain our neutral rating and expect spreads in the 420-440 bp range, with the possibility of tactical tightening. A sell-off in credit markets usually starts with higher volatility leading to a repricing of credit spreads, with IG bonds suffering more first. The second stage of the sell-off is more characterised by defaults. This mainly affects HY stocks, as creditworthiness deteriorates and financing becomes more difficult. In the extreme risk scenario, we would assume that US HY bond yields could quickly rise above 500 bps.

Our conclusion: Although HY bond spreads could rise another 60-80 bps, the current level of interest rate yields means that interest rate risk is limited, neutral.

Emerging market bonds in hard currencies (neutral)

The current high yield of the JP Morgan Emerging Market Bond Index Global (6.6% yield to maturity), together with the still elevated spreads, offers an interesting yield advantage over US Treasuries to compensate for the risks. Many EM central banks have already raised their interest rates. Therefore, EM bond yields are expected to be able to withstand higher 10-year US yields. However, the risks related to the geopolitical situation and a larger-than-expected rise in US interest rates remains.

Our conclusion: While yields have risen far enough, so have the risks. Therefore, we rate this asset class as neutral at the moment.

Maria Albericci

Status: 02.05.2022

Source: Chefinvest AG, Zurich, Market Map

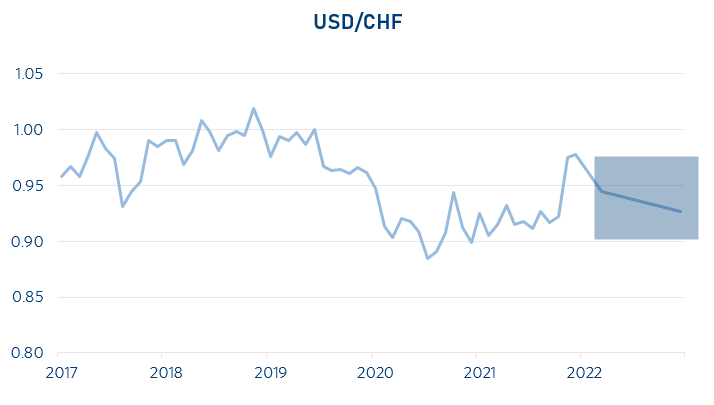

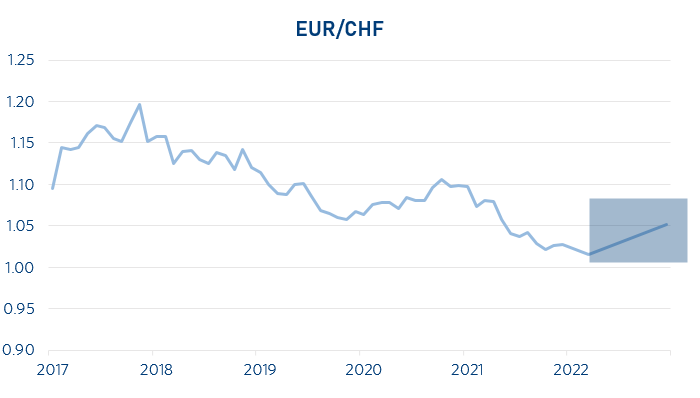

Currencies

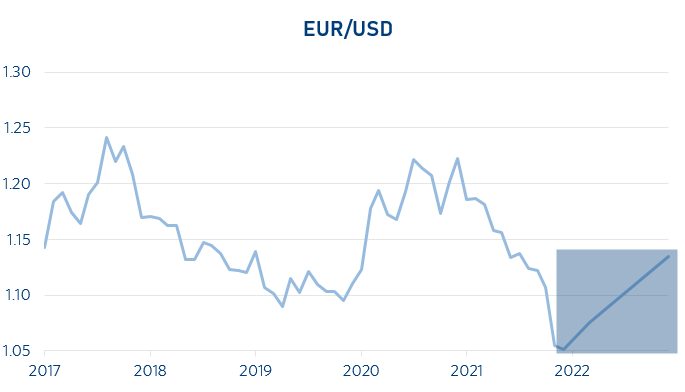

Dollar/Euro/Franc soon parity?

Currencies continue to be in the playing field of the geopolitical situation and central banks. There is no fundamental change since the AKS at the beginning of the year.

EUR/USD (Currently 1.05)

The euro continues to fall against the greenback, which is considered a safe haven. The FED will raise interest rates significantly this year, which will bring investors new investment opportunities in USD.

Our conclusion: The expected interest rate differential and the geopolitical situation continue to strengthen the USD.

EUR/CHF (Currently 1.02)

The SNB has started to intervene slightly. However, it must be said that it is an advantage for the Swiss economy to have its own and independent currency. The safe haven effect and the appreciation tendencies counter inflation and this is worth its weight in gold. Inflation in Switzerland is currently around 2.4%. That is why the SNB has allowed the appreciation to a certain extent. It is important that the Swiss Franc can move close to the market, i.e. determined by supply and demand. Interest rate policy in Europe will play a major role.

Our conclusion: The strength of the Swiss Franc will continue in the current environment.

USD/CHF (Currently 0.97)

The USD remains strong against the CHF. The persistent and high inflation in the USA is visibly forcing the US Federal Reserve to tighten monetary policy earlier and more strongly, and is again providing investors with new investment opportunities in USD.

Our conclusion: We expect this to continue.

Mimi Haas, Lic. Rer.pol. HSG, M.A. in Banking and Finance HSG, Partner

Status: 02.05.2022

Source: Chefinvest AG, Zurich, Market Map

Oil

The cards are redistributed

In April, the International Energy Agency (IEA) lowered its oil demand estimates for this year by 260,000 to 99.4 million barrels per day. The main reasons for this are an expected economic slowdown in China as a result of the ongoing lock-downs. Oil production is expected to decline by a net 500,000 barrels per day due to the sanctions against Russia. On the supply side, the release of a total of 180 million barrels from strategic reserves decided by the USA at the end of March is currently helping. This means that 1 million barrels per day will be made available for half a year. Furthermore, it can be assumed that the supply chains will be reformatted and emerging countries will buy more (cheaper) oil from Russia. Brent and WTI oil prices have settled just above USD 100 in recent weeks.

Our Conclusion: The slight declines in supply and demand are currently more or less in balance. We still expect the supply situation to calm down in the coming months and oil prices to be well below USD 100 per barrel in the second half of the year.

Status: 02.05.2022

Precious Metals

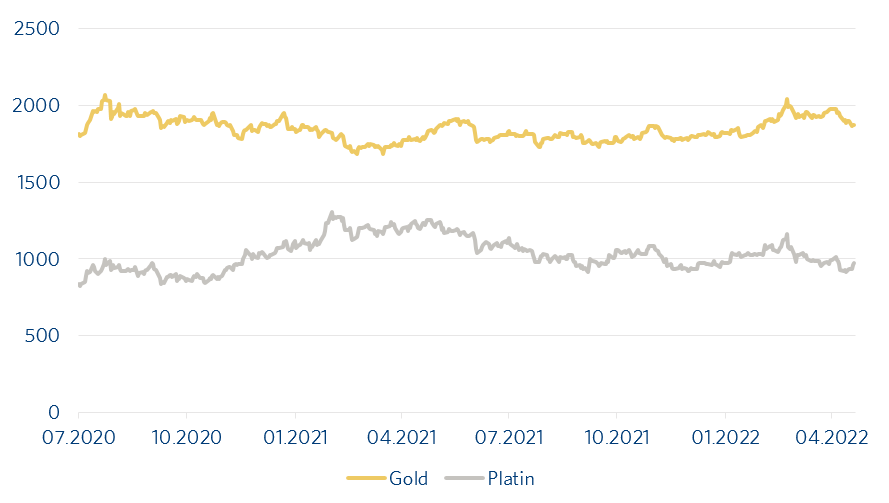

Gold price under pressure

The prospects of future measures regarding interest rate hikes by the US Federal Reserve have caused the gold price to fall to just under USD 1,860 per ounce. The stronger USD is not helping gold at the moment either, negative real yields are supporting it. Platinum is also slightly weaker at around USD 932 per ounce and must continue to hope for better functioning supply chains at automotive suppliers.

Andreas Betschart, Business Manager

Our conclusion: We expect slightly volatile gold prices in the coming months with a trading range of USD 1,830 to 2,030 per ounce. We continue to see platinum in a price band of USD 900 to 1,100 per ounce in the coming months.

Status: 02.05.2022

Source: Chefinvest AG, Zurich, Market Map

Abbreviations and explanations

bbl: 1 Barrell = 158,987294928 Litre

Bp: Basis points

GDP: Gross domestic products

BIZ: the Bank for International Settlements is an international financial organization. Membership is reserved for central banks or similar institutions.

EM-Bonds: Emerging market bonds. An emerging market is a country that is traditionally still counted as a developing country but no longer has its typical characteristics.

HY-Bonds: Fixed-income securities of poorer credit quality. They are rated BB+ or worse by the rating agencies.

IG-Bonds: Investment grade bonds are all bonds with a good to very good credit rating (Ra-ting). The investment grade range is defined as the rating classes AAA to BBB-.

IHS Markit: Listed data information services company

IWF: The International Monetary Fund (also known as the International Monetary Fund) is a legally, organiza-tionally, and financially independent specialized agency of the United Nations headquartered in the United States of America.

KOF: Business Cycle Research Centre at ETH Zurich

LIBOR: London Interbank Offered Rate is a reference interest rate determined in London on all banking days under certain conditions, which is used, among other things, as the basis for calculating the interest rate on loans.

OPEC: Organization of the Petroleum Exporting Countries

OPEC+: Cooperation with non-OPEC countries such as Russia, Kazakhstan, Mexico and Oman.

oz: the troy ounce is used for precious metals as a unit of measurement and is equal to 31.1034768 grams

Saron: The Swiss Average Rate Overnight is a reference interest rate for the Swiss franc

Seco: Swiss State Secretariat for Economic Affairs

Spread: Difference between two comparable economic variables

WTI: West Texas Intermediate. High-quality US crude oil grade with a low sulfur content.

Disclaimer:

The information and opinions have been produced by Chefinvest AG and are subject to change. The report is published for information purposes only and is neither an offer nor a solicitation to buy or sell any securities or a specific trading strategy in any jurisdiction. It has been prepared without regard to the objectives, financial situations or needs of any particular investor. Although the information is derived from sources that Chefinvest AG believes to be reliable, no representation is made that such information is accurate or complete. Chefinvest AG does not assume any liability for losses resulting from the use of this report. The prices and values of the investments described and the returns that may be received will fluctuate, rise or fall. Nothing in this report is legal, accounting or tax advice or a representation that any investment or strategy is appropriate to personal circumstances or a personal recommendation for specific investors. Foreign exchange rates and foreign currencies may adversely affect value, price or yield. Investments in emerging markets are speculative and involve considerably greater risk than investments in established markets. The risks are not necessarily limited to: Political and economic risks, as well as credit, currency and market risks. Chefinvest AG recommends investors to make an independent assessment of the specific financial risks as well as the legal, credit, tax and accounting consequences. Neither this document nor a copy of it may be sent in the United States and/or in Japan and they may not be handed over or shown to any American citizen. This document may not be reproduced in whole or in part without the permission of Chefinvest AG.