Click on the images to view our comments on each topic.

Switzerland

Opportunities for exporters and investors

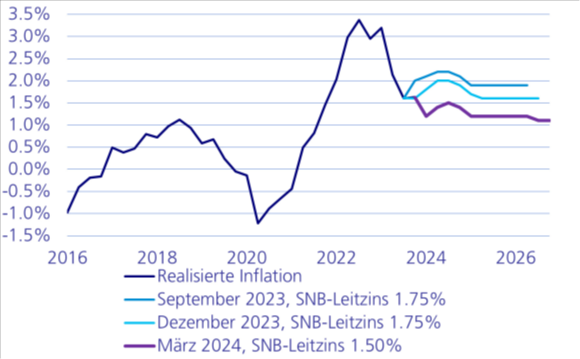

On March 21, the Swiss National Bank surprisingly lowered the key interest rate by 25 basis points to 1.50%. This led to a devaluation of the Swiss franc against the euro and the US dollar. The decision came as a surprise to most market observers, as they had expected a clearer signal from the European Central Bank and the US Federal Reserve. According to Thomas Jordan, Chairman of the SNB, this decision is due to the central bank's success in combating inflation. Although the growth of the Swiss economy is below the long-term trend level, no urgent risk of recession was identified that would have required a preventive step. However, low inflation gave the SNB leeway to cut interest rates. Nevertheless, this is not expected to signal a comprehensive easing cycle. The SNB forecasts an inflation rate of 1.40% for 2024 and 1.20% for 2025.

Although monetary conditions have eased thanks to the depreciation of the franc by almost 4.00% since the beginning of the year, the SNB Governing Board, which for the first time with the vote of new Governing Board member Antoine Martin, decided to cut interest rates. The comments on the real estate market were surprisingly brief. In the past, the SNB had expressed concerns about imbalances on the real estate market. Even though that real estate prices are continuing to rise, it only mentions the real estate market in passing in its press release. It has also revised its GDP forecast slightly upwards and now expects growth of around 1.00% for 2024.

GDP 2024 1.00% (SNB)

Inflation 2024 1.40% (SNB)

SNB key interest rate 1.50%

Our conclusion:

A weaker franc favors export-oriented sectors such as the watch industry, medical technology companies, the chemical, pharmaceutical industry and mechanical engineering. The earnings momentum of companies is high. We recommend buying Swiss equities and consider medium-sized companies to be interesting.

Sources: SNB, UBS, Chefinvest

As at: 25.03.2024

European Union

Tentative recovery and easing price pressure

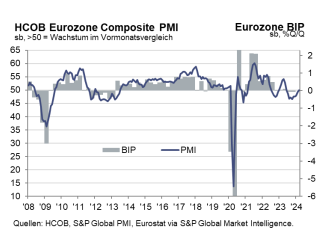

Compared to the previous quarter, seasonally adjusted gross domestic product (GDP) remained unchanged in both the euro area and the European Union (EU) in the fourth quarter of 2023. In the third quarter of 2023, GDP fell by 0.10% in the euro area and remained unchanged in the EU. For 2023 as a whole, GDP rose by 0.40% in both the euro area and the European Union (EU) after +3.40% in both areas in 2022. Europe spent last year largely in stagnation.

The European Central Bank (ECB) is now forecasting economic growth of 0.60% for the current year 2024, after previously forecasting 0.80%. The decline in inflation, the recovery in household income and the strengthening of foreign demand are positive factors here. A GDP growth rate of 1.50% is expected for 2025 and 1.60% for 2026.

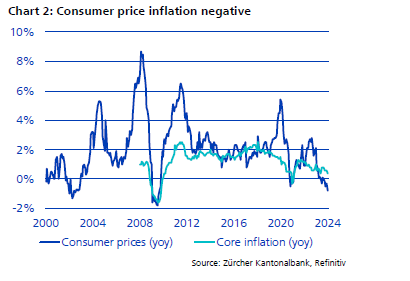

In the eurozone the annual inflation rate was 2.60% in February 2024, compared to 2.80% in January. The main reason for the decline is a low contribution from energy prices. A year earlier, it had been 8.50%. The annual inflation rate in the European Union was 2.80% in February 2024, down from 3.10% in January. A year earlier, it had been 9.90%. The experts at the European Central Bank (ECB) have revised their inflation projections downwards. Inflation of 2.30% is now expected for the current year 2024, 2.00% for 2025 and 1.90% for 2026. The forecasts for core inflation have also been adjusted downwards to 2.30% for 2024, 2.10% for 2025 and 2.00% for 2026.

The positive situation on the labor market continues and the unemployment rate remains at a very low level in many places. The seasonally adjusted unemployment rate in January 2024 in the euro area was 6.40%, down from 6.50% in December 2023 and down from 6.60% in January 2023. The unemployment rate in the EU was 6.00% in January 2024, unchanged from December 2023 and down from 6.10% in January 2023.

The final seasonally adjusted HCOB Composite PMI climbed to 49.9 points in March from 49.2 in February. With a 9-month high, it signaled that business activity has almost stabilized again. While the upturn in the service sector gained momentum, industrial production contracted less sharply. The situation remained mixed at country level. The continuing decline in growth in Europe's two largest economies, Germany and France, offset the accelerating upturn in the other eurozone countries.

GDP growth 2024 +0.60% (E)

EU inflation 2024 +2.30% (E)

Current 3-month Euribor +3.90%

Our conclusion:

European economic growth almost stabilized in March and price pressure eased further.

The economic outlook for Europe has gradually brightened recently and a slightly higher growth rate at subdued levels can be expected in the coming months. The good labor markets are a key reason for this. According to surveys of purchasing managers, the poor situation in industry has brightened slightly due to the better than originally expected global economy and the economically more important service sector is likely to expand again soon.

The ECB Governing Council left key interest rates unchanged at its meeting at the beginning of March. Looking ahead, the ECB expects inflation to reach its target of 2.00% in 2025. The reduction in inflation and growth forecasts points to an easing of interest rates in during the year. The market currently expects an initial interest rate cut of 25 basis points in June and three further cuts of the same magnitude by the end of the year. In total, this would amount to 100 bp by the end of the year.

We expect the macroeconomic and business environment to develop favorably. Based on this improved outlook for the European economy and the interest rate cuts promised by the ECB, we maintain our optimistic view for the European equity market.

Daniel Beck, Member of the Executive Board

Sources: European Commission, Statista, HCOB, S&P Global

As at: 25.03.2024

United Kingdom

When the clouds slowly clear

The current economic environment in the UK is characterised by a modest recovery, although certain challenges remain. A slight improvement in economic conditions is forecasted for the second quarter of 2024, but growth remains below the level of other developed economies. Some experts expect a gradual improvement in economic growth in the UK, with a projected GDP increase of around 0.2% in the second quarter of 2024. This is part of a wider trend of a slow but steady recovery over the year, with expected annual growth of 0.63% for the year 2024 according to IMF estimates. The Office for National Statistics (ONS) reported that 16% of businesses saw an increase in sales in February 2024. And only 20% of businesses do predict an increase in turnover in April 2024, indicating a continued cautious outlook among UK businesses.

Some experts expect inflation to reach the Bank of England's target level of 2.00% as early as 2024, which could allow interest rates to be cut in the summer. The IMF, on the other hand, sees inflation to fall to 3.60% in the course of 2024 and to 2.10% in 2025. According to the National Institute of Economic and Social Research (NIESR), lower average household incomes are a major challenge. This is because economic growth and productivity remain low at the moment, which is contributing to increased financial vulnerability and rising income inequality. According to IMF estimates, the unemployment rate is expected to rise to 4.70% in 2024 before falling slightly to 4.30% in 2025.

Our conclusion: Neutral

To summarise, the UK economy is on a path of slow recovery with modest GDP growth, cautious business optimism and a positive outlook for inflation and interest rates. However, the challenges of low productivity, income inequality and regional differences in wage growth remain significant concerns. We expect the central bank to stimulate interest rates sooner than anticipated. The attractiveness of UK investments is likely to increase in the third quater 2024.

Sources: S&P, Citigroup, MarketMap, IMF, and Chefinvest

As of: 25.03.2024

USA

Strong job growth

After the US economy grew by 3.20% in the last quarter of 2023, the GDPNow model of the Federal Reserve of Atlanta is forecasting growth of 2.10% for the first quarter of 2024. Economic growth therefore appears to be weakening less than expected at the start of the year. At its last meeting on March 20, the Fed also raised its GDP growth forecast for 2024 from 1.40% to 2.10% and left the Fed Fund Rate unchanged at 5.25% - 5.50%.

In February, headline inflation rose 0.10% on the previous month to 3.20%. By contrast, the core rate (excluding energy and food) fell 0.10% to 3.80%. Due to the slightly slower decline in inflation, the Fed has raised its estimate of inflation for personal consumption expenditures (PCE), which it closely monitors, from 2.40% to 2.60% for 2024. The markets have adjusted to the Fed's expectation of 'only' 3 interest rate cuts of 0.25% each since January. The first rate cut is now not expected until the June meeting.

The US Composite PMI weakened slightly in March compared to the previous month by 0.30% to a still robust 52.20 points. Encouragingly, the economic expansion was also supported by the manufacturing sector (sub-index +0.30 to 52.5 points). The services sub-index stood at 51.7 points (-0.60%).

The picture of sustained economic strength is also confirmed by the labor market. In February, 275,000 new jobs were created outside of agriculture (+200,000 were expected). Unemployment rose by 0.20% month-on-month to a (still low) 3.90% in February, approaching the latest Fed forecast of 4.00% for the current year.

S&P 500 companies' earnings are expected to rise by a total of 11.10% in 2024, after growing by 3.10% in the previous year. Based on earnings estimates for the next 12 months, the S&P 500 Index has a proud price/earnings ratio of 20.9. The 5-year average is 19.0 and the 10-year average is 17.7.

GDP2024 (IMF): +2.10% (E)

Inflation 2024 (IMF): +2.76% (E)

Fed Fund Rate: +5.50%

Our conclusion:

The US economy appears to be cooling compared to the previous year but remains on a solid growth trajectory. Declining inflation and the resulting foreseeable interest rate cuts will drive corporate sales and earnings figures. This supports the current valuation and the bull market.

Dr. Patrick Huser, CEO

Sources: Trading Economics, US Bureau of Labor Statistics, Statista, FuW, IMF World Economic Outlook October 2023, FactSet, FMOC

As at: 25.03.2024

China

New year, old challenges

The year began in China under the auspicious zodiac sign of the dragon. Despite this symbolism, economic successes in dragon years have not been exceptionally positive in the past. It seems that this will continue in 2024 as the Chinese economy continues to struggle to gain momentum. The official purchasing managers' index for the manufacturing sector has fallen in nine of the last ten months. Although the Chinese central bank lowered the benchmark interest rate for mortgages in February, the famous light at the end of the tunnel in the real estate market remains dimly visible for the time being. Nevertheless, household incomes are rising slightly and supporting private consumption. Some consumption indicators point to cautiously optimistic trends. In addition, the fiscal measures already introduced could give the economy a further boost, and it would be no surprise to see further announcements of targeted economic aid after the People's Congress in March. There is a possibility that economic growth in 2024 could be higher than previously expected. While many industrialized countries are still struggling with excessively high inflation rates, China continues to record negative inflation rates at the start of the new year. This is mainly driven by falling food prices, especially pork. Price pressure in other categories was also subdued. However, there are no clear signs of deflation yet.

IMF Economic Forecast

GDP 2024: 5.00%

Inflation 2024: 0.50%

3- month shibor: 2.16%

Our conclusion:

The annual meeting of the National People's Congress took place at the beginning of March. The GDP growth target was set at 5.00%. A target of 3.00% of GDP was set for planned new borrowing, which does not signal much scope for greater fiscal policy support. The Chinese stock market is very cheaply valued, reflecting the political risks.

Sources: ZKB, IMF, Chefinvest

As at: 24.03.2024

Japan

Markets in Japan are becoming less attractive

Japan's economic situation in 2024 shows a phase of mixed expectations and challenges. The GDP forecast for 2024 points to possible moderate growth, influenced by internal and external factors such as global market conditions and domestic consumption. The Bank of Japan's interest rate policy remains cautious, with interest rates expected to remain close to zero to stimulate investment and keep inflation within the central bank's target range. Minutes of the latest central bank meeting show that many Bank of Japan policymakers see the need to proceed slowly in exiting ultra-loose monetary policy. One board member said the health of the economy did not warrant rapid interest rate hikes, according to a summary of opinions at the bank's March meeting. The central bank's move away from negative policy in the first half of the year did not come as a surprise, as the market was well prepared for it. Another point to keep an eye on is that the central bank wants to reduce its large equity holdings.

The unemployment rate is stable at 2.40%, which could have a positive impact on consumption and economic growth. Japanese companies' profit and sales expectations for 2024 depend heavily on the global economic recovery, exchange rates and domestic and external economic conditions. The government is actively promoting a sustainable economic recovery, particularly through the promotion of green technologies and digitalization, as well as measures to support start-ups and promote energy independence. This overview shows that Japan is facing various economic and political challenges. The country is striving to promote stable growth through targeted measures and reforms.

IMF Economic Forecasts:

GDP 2024: 1.00%

Inflation 2024: 2.90%

3- months (JPY Libor) -0.03%

Our conclusion:

The equity index has risen sharply in 2023 and 2024, which is why we advise clients not to make any new investments in the market. Existing investments should be adjusted, according to the weighting entered at the beginning, for risk considerations. This is because a market that has risen so sharply is susceptible to corrections.

Mimi Haas, Lic. rer.pol. HSG, M.A. in Banking and Finance HSG, Partner

Sources: IMF, FT, SSGA Economist and AI

As of: 25.03.2024

Emerging Markets

Central bank reactions and growth prospects

Emerging market currencies are under pressure due to the strong economy in the US and the strength of the dollar. This is leading to widespread currency weakness in emerging markets, which is triggering various reactions from central banks. Despite currency devaluation risks, most central banks are focusing on domestic inflation in the services sector and are less impressed by the US. The aggressive response of central banks to the inflation shock and the narrowing of current account deficits last year have better protected emerging markets from capital outflows. Despite some precautionary measures, the picture of significant interest rate cuts over the next twelve months is likely to remain, suggesting a broader cycle of rate cuts in the second half of the year to boost the economy. In Brazil, the Banco Central do Brasil confirmed its sixth key interest rate cut in a row in March. This should stimulate investment and consumption.

The Indian economy continued its robust growth in the last month of the first quarter, as shown by the preliminary purchasing managers' indices. The PMI Composite, PMI Manufacturing and PMI Services all point to continued expansion, with both domestic and export demand strong. New jobs have been created, albeit on a moderate scale. Despite increasing cost pressure, business confidence remains high. The purchasing managers' indices point to a strong first quarter overall.

Our conclusion:

The emerging markets are well positioned for sustained economic growth. Equity valuations for the major emerging markets such as Mexico and India appear attractive.

Sources: ZKB, IMF, Chefinvest

As at: 24.03.2024

Stocks

Powell, Jordan & Co. conjure up new highs

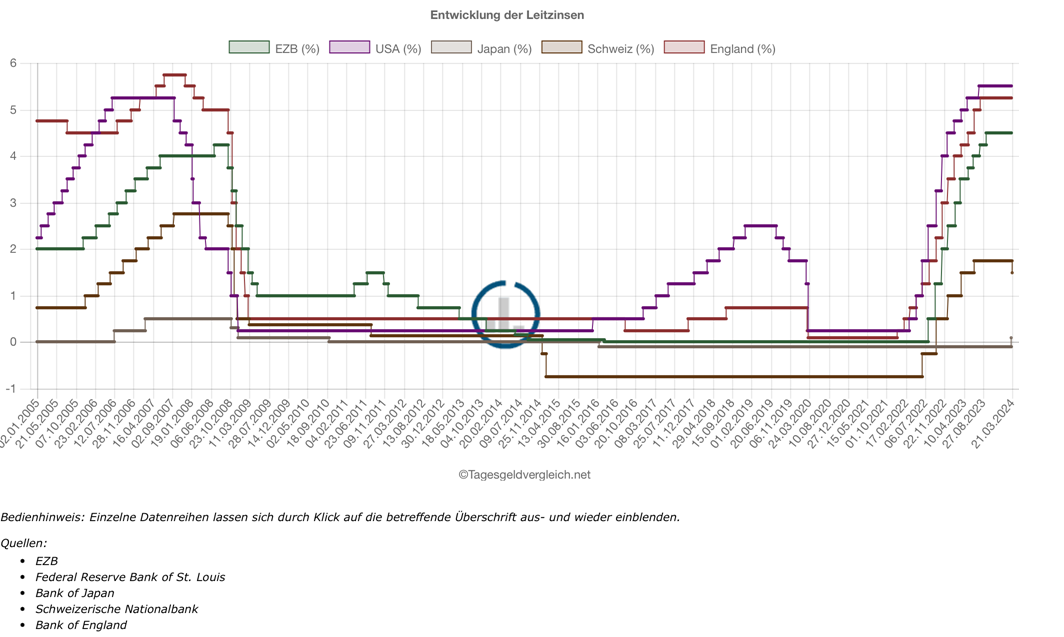

The global stock markets are showing their best side, driven by decisive measures taken by central banks around the world. In the USA in particular, monetary easing that exceeded expectations, underlined by Fed Chairman Jerome Powell's confident statements, led to new highs on the stock markets. Powell emphasized that despite growth, the US economy would not deter the central bank from further easing measures. As a pioneer in this regard, the Swiss National Bank lowered borrowing costs, a move that was expected but in coordination with the ECB. Thus, it is likely that other central banks will follow sooner than expected, with the opposite move by the Bank of Japan.

Contrary to the conventional wisdom that a maturing bull market tends to taper, we are witnessing a broadening of the bull market. An increasing number of US and global stocks are breaking through their trading ranges, supporting expectations that 2024 will see a more global and cross-sector gain. This is also reflected in the importance of diversification, as the share of US equities in global market capitalization has risen from 50.00% to 70.00% and is seen as unlikely to increase further in the next few years. "Nearshoring" should ensure that corporate profits are increasingly shifted back to consumer markets, which may be good news for European companies.

Our conclusion: The traffic light is green

The financial markets are in unexpectedly positive shape, driven by a slowdown in inflation and an uptick in corporate profits - a real "party time" for investors. The US Federal Reserve (Fed) foresees sustained growth in the economy over the next three years and plans to cut the key interest rate to around 3.00% by the end of 2026, a marked contrast to the gloomy forecasts two years ago, which predicted expensive money and the end of the post-pandemic economic recovery. The Swiss National Bank, traditionally in coordination with the ECB, could be a trendsetter, with Japan appearing as an exception with its continued low interest rate policy.

The CAIB Barometer confirms this optimistic outlook with a probability of success of 66.00% in the short term and 65.00% over a one-year horizon. The Swiss stock markets are particularly characterized by advantages due to a less strongly appreciating Swiss franc in international comparison.

Rico Albericci, CEFA

Sources: S&P, Citigroup, MarketMap, IMF, and Chefinvest

As of: 25.03.2024

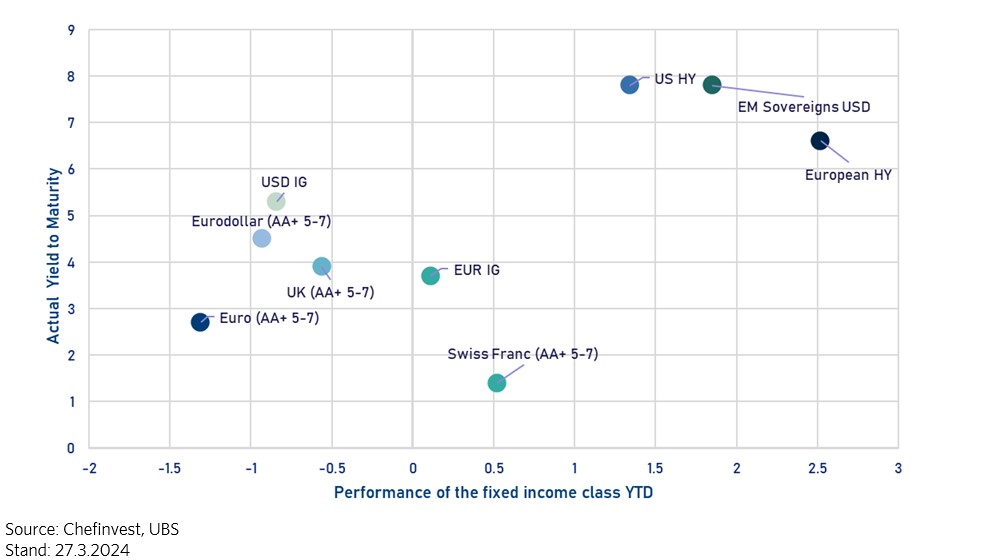

Interest

Expected key interest rate cuts influence bond yields

Surprisingly, the Swiss National Bank predicted to cut key interest rates in March 2023. In the CHF investment segment, interest yields have already been below dividend yields for several months, making them less attractive. The ECB and the Fed will follow soon in the coming months. It is only a question of time and depends on a variety of factors, such as the global economic situation, inflation expectations, wage structure, labor market data and geopolitical developments, when this will happen. As interest rates fall, same will happen in the two currency areas mentioned above, as in Switzerland. This is why you should extend the maturities of new investments to take advantage of today's higher interest rates.

Government bonds:

We expect yields on this bond class to fall. Weaker growth should contribute to lower interest rate expectations.

Investment grade bonds:

Due to attractive yield premiums on quality bonds and an improvement in creditworthiness, an overweighting of this asset class is recommended. The duration range should be adjusted to the expected interest rate cuts.

High yield bonds:

The current yields of 7.00% offer a good buffer against payment defaults. A possible widening of the spread in 2024 could result in attractive entry points. High-yield bonds with a better BB rating are better equipped for a possible economic downturn due to lower debt. However, we recommend this asset class more to investors who can bear the risk and should be allocated to an ETF.

Emerging markets bonds:

Emerging markets bonds in local currency offer a high yield of 9.00% and are relatively safe from currency losses and credit defaults, especially if US yields are forecast to fall. However, we recommend this asset class more to investors who can bear the risk and should allocate to an ETF.

Our conclusion:

Overall, bonds appear attractive in 2024 due to their yield and the economic environment, although the risk varies depending on the type of bond.

Mimi Haas, Lic. rer.pol. HSG, M.A. in Banking and Finance HSG, Partner

Sources: F&W, JP Morgan and Bloomberg

As of: 25.03.2024

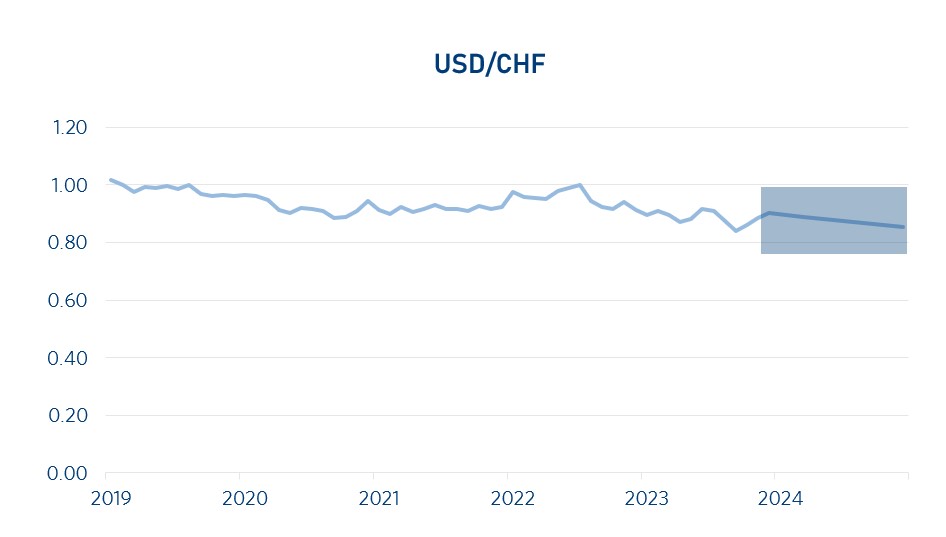

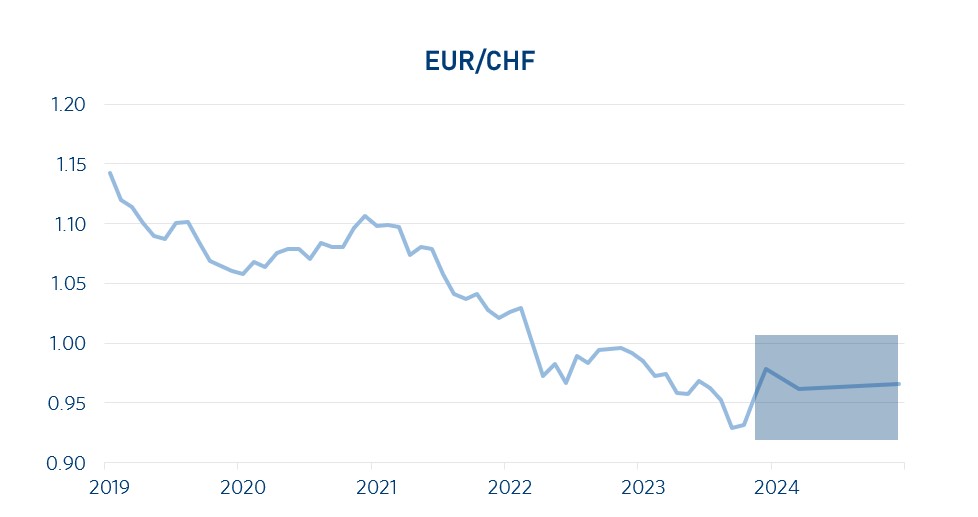

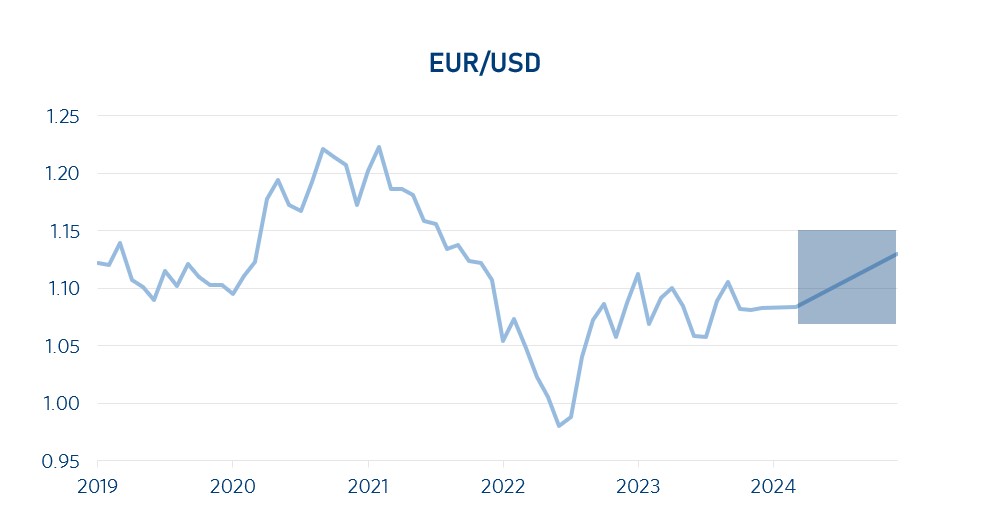

Currencies

SNB brings changes to the market by raising key interest rates

EUR/USD: (28.03.2024: 1.08)

Lower than expected inflation and labor market data in the US caused the exchange rate to rise at the end of 2023. In 2024, there are increasing signs that the optimism of the final months of the past year 2023, that a rapid turnaround in monetary policy is to be expected, is becoming unlikely. Supported by surprisingly strong labor market data, the US dollar appreciated again and recouped some of its losses. The EUR/USD is still on a downward trend from its high in December 2023. Our conclusion: The currency pair will therefore remain volatile, as in 2023, and will develop depending on the central banks and their actions.

EUR/CHF: (28.03.2024: 0.98)

The SNB lowered interest rates from 1.75 % to 1.50 %, making it the first major central bank to cut rates. It appears that the Swiss franc is under pressure and will remain under pressure even after the SNB's surprise rate cut ahead of the ECB. As expected, the monetary policy statement maintained the line that the SNB remains ready to actively intervene in the foreign exchange market if needed. It is pointed out that the easing of monetary policy was made possible because the fight against inflation has been effective over the past two and a half years. Of course, the SNB had to be cautious, as Switzerland is heavily dependent on the eurozone. In the EUR/CHF pair, the first resistance level is 0.978/0.98. After that, there is room for further gains up to 0.99 or parity.our conclusion: we forecast that the franc will weaken against the euro in the short term.

USD/CHF: (28.03.2024: 0.91)

The positive interest rate differential between the dollar and the franc, which widened after the SNB decision, suggests that the USD will be supported.

Our conclusion:

The currency pair should trend slightly higher in the coming months.

Mimi Haas, Lic. rer.pol. HSG, M.A. in Banking and Finance HSG, Partner

Sources: F&W, Market Map and Bloomberg

As of: 28.03.2024

Oil

Challenging balancing act

According to the International Energy Agency (IEA), the post-pandemic surge in demand has come to a standstill. Despite weak demand (e.g. from China), the oil market remains tight. This is due to the fact that less oil has been produced in the USA and Canada due to extremely low Arctic temperatures and OPEC+ is sticking to its production cuts. For the current year, the IEA expects global demand of 103 million barrels per day and supply of 103.8 million barrels per day. The WTI oil price is currently trading at just over USD 80 per barrel.

Our conclusion: We expect WTI oil to move in a range between USD 70 and USD 90 per barrel.

Dr. Patrick Huser, CEO

Sources: F&W, MarketMap,International Energy Agency (IEA)

as at: 25.03.2024

Precious Metals

Interesting development in the last 3 months

The gold price experienced a positive development with an increase of around 7.00% in the last 30 days. At the time of asking, the price was around USD 2,173 per ounce, a slight increase on the previous day and a year-on-year increase of +9.50%. Falling key interest rates are likely to push the gold price to further highs.

Platinum, on the other hand, showed less positive movement; however, it is recovering with a current price of around USD 907 per ounce, which represents an increase of USD 9.00 compared to the previous day. Stricter emission standards as well as falling US interest rates could further help platinum to increase its price.

Our conclusion: Gold will move between USD 2,050 and USD 2,150 per ounce in the coming months and platinum will continue to rise.150 USD per ounce and platinum between 870 and 920 USD per ounce.

Andreas Betschart, Business Manager

Sources: UBS

As at: 25.03.2024

Abbreviations and explanations

bbl: 1 Barrell = 158,987294928 Litre

Bp: Basis points

GDP: Gross domestic products

BIZ: the Bank for International Settlements is an international financial organization. Membership is reserved for central banks or similar institutions.

EM-Bonds: Emerging market bonds. An emerging market is a country that is traditionally still counted as a developing country but no longer has its typical characteristics.

HY-Bonds: Fixed-income securities of poorer credit quality. They are rated BB+ or worse by the rating agencies.

IG-Bonds: Investment grade bonds are all bonds with a good to very good credit rating (Ra-ting). The investment grade range is defined as the rating classes AAA to BBB-.

IHS Markit: Listed data information services company

IWF: The International Monetary Fund (also known as the International Monetary Fund) is a legally, organiza-tionally, and financially independent specialized agency of the United Nations headquartered in the United States of America.

KOF: Business Cycle Research Centre at ETH Zurich

LIBOR: London Interbank Offered Rate is a reference interest rate determined in London on all banking days under certain conditions, which is used, among other things, as the basis for calculating the interest rate on loans.

OPEC: Organization of the Petroleum Exporting Countries

OPEC+: Cooperation with non-OPEC countries such as Russia, Kazakhstan, Mexico and Oman.

oz: the troy ounce is used for precious metals as a unit of measurement and is equal to 31.1034768 grams

Saron: The Swiss Average Rate Overnight is a reference interest rate for the Swiss franc

Seco: Swiss State Secretariat for Economic Affairs

Spread: Difference between two comparable economic variables

WTI: West Texas Intermediate. High-quality US crude oil grade with a low sulfur content.

Disclaimer:

The information and opinions have been produced by Chefinvest AG and are subject to change. The report is published for information purposes only and is neither an offer nor a solicitation to buy or sell any securities or a specific trading strategy in any jurisdiction. It has been prepared without regard to the objectives, financial situations or needs of any particular investor. Although the information is derived from sources that Chefinvest AG believes to be reliable, no representation is made that such information is accurate or complete. Chefinvest AG does not assume any liability for losses resulting from the use of this report. The prices and values of the investments described and the returns that may be received will fluctuate, rise or fall. Nothing in this report is legal, accounting or tax advice or a representation that any investment or strategy is appropriate to personal circumstances or a personal recommendation for specific investors. Foreign exchange rates and foreign currencies may adversely affect value, price or yield. Investments in emerging markets are speculative and involve considerably greater risk than investments in established markets. The risks are not necessarily limited to: Political and economic risks, as well as credit, currency and market risks. Chefinvest AG recommends investors to make an independent assessment of the specific financial risks as well as the legal, credit, tax and accounting consequences. Neither this document nor a copy of it may be sent in the United States and/or in Japan and they may not be handed over or shown to any American citizen. This document may not be reproduced in whole or in part without the permission of Chefinvest AG.