Click on the images to view our comments on each topic.

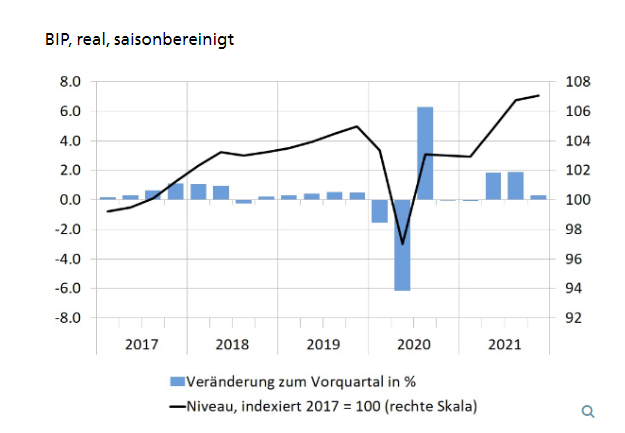

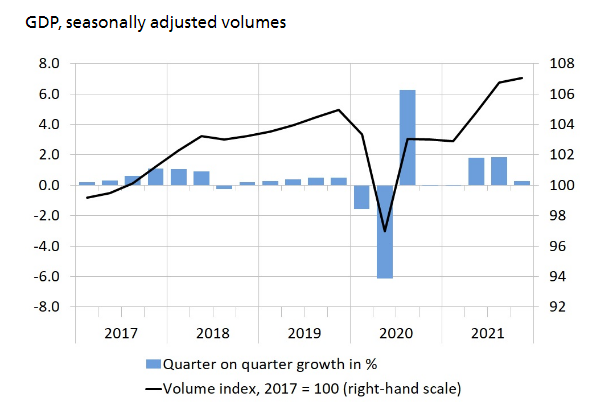

Switzerland

Stable and confident

In Switzerland, GDP grew by 0.3% in Q4 2021 to a total of 3.7% for 2021. The economy thus recovered quickly from the slump in 2020. All sectors of the economy were affected by the recovery, albeit to varying degrees. The first weeks of the new year were still marked by the recent Corona wave and the associated measures. In mid-February, the Federal Council lifted almost all Corona measures and consumer behaviour is expected to return to pre-crisis patterns. The unemployment rate is encouragingly low and has returned to pre-crisis levels. The war in Ukraine poses major risks for the global economy. According to SECO experts, the direct impact of the conflict on Switzerland is likely to be limited. The economic interdependence with Russia and Ukraine is relatively low. Indirect effects are expected on the cost side. Energy, some basic foodstuffs and industrial metal prices have risen significantly. Inflation expectations have therefore also been raised for Switzerland to 1.9% for 2022. The strong Swiss franc is only partially dampening import inflation.

Our conclusion: The uncertainty surrounding the Ukraine conflict is very high. The Swiss economy would be hit hard if there were a significant economic downturn in important trading partner countries. SECO has lowered its growth forecasts for the current year to 3%, which is still a very positive figure. The Swiss economy is well diversified and internationally broad-based. Most large companies have solid balance sheets. The state is hardly indebted and also has ample scope for intervention if necessary. The framework conditions for investments in the Swiss equity market remain good.

As of: 15.03.2022

Source: SECO

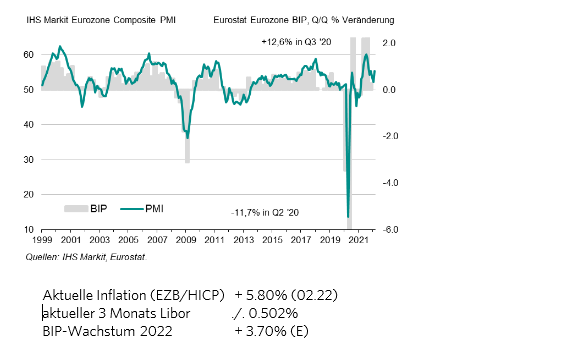

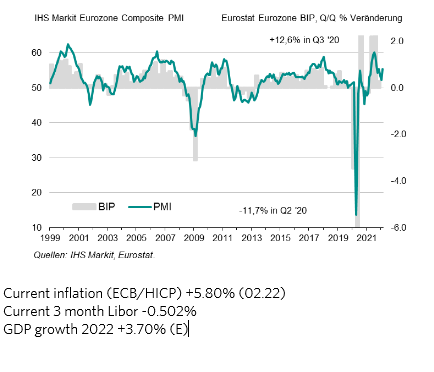

European Union

Europe - Slower growth

The euro area economy grew by 5.3% in 2021 as a whole, and gross domestic product (GDP) at the end of the year had reached the level it had before the outbreak of the pandemic. However, the Russian war against Ukraine brings new risks to the European economy, which is just recovering from the Corona pandemic. For this reason, the experts of the European Central Bank (ECB) have revised their estimates for GDP growth downwards and reduced the growth forecast for this year to 3.7%. For 2023 they now assume 2.8% and for 2024 1.6%. Rising energy prices in particular (+31.7% in February), which have recently increased significantly due to the escalation in the Ukraine-Russia conflict, are keeping inflation at a high level. In the euro area, the inflation rate in February was 5.8%, the highest value since the introduction of the euro. Both purchase and supply prices rose at new record rates. Eurozone economic growth returned to robust strength in February ahead of the Ukraine invasion. The final IHS Markit Eurozone Composite Index (PMI) rose 3.2 points to 55.5 in February from January's 11-month low. The year-to-date business outlook brightened compared to January, and was again more optimistic than in the previous three months.

Daniel Beck, Member of the Executive Board

Our conclusion: The economic recovery in the Eurozone will depend on the course of the war between Russia and Ukraine, the effects of the economic and financial sanctions and other measures. In their baseline scenario for 2022, the ECB experts continue to expect strong growth in the euro area economy (3.7%), albeit at a slower pace than expected before the outbreak of the war. On the positive side, firstly, the easing of adverse effects from the Omikron variant of the coronavirus gives a strong boost to the economic recovery. Second, there are signs of an easing in supply constraints. Third, the prospect of strong domestic demand, and the labour market situation is improving. The unemployment rate fell to 6.8% in January.

Expected (IMF) 2022:3.7% (E), Current inflation (ECB/HICP) 5.8% (02.22), Current 3-month Libor -0.502%.

As of: 15.03.2022

Source: CIHS Markit

United Kingdom

USA

The hawks are back

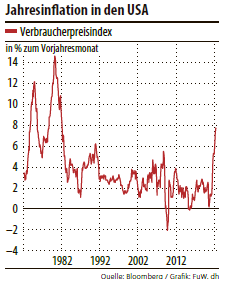

After strong economic growth of 5.6% in 2021, the IMF, according to its latest forecast from the end of January 2022, expects a still strong expansion of 4.0% in the USA for the current year, followed by moderate growth of 2.6% in 2023. However, due to the latest developments, it can be assumed that these expectations will be corrected downwards. The rule of thumb is that for every USD 10 increase in the oil price, gross domestic product is reduced by 0.5%. In the fourth quarter of 2021, the corporate profits of the S&P 500 companies increased by a good 30%, as in the three preceding quarters. For the first quarter of 2022, analysts still expect earnings growth of 4.8% for these companies (compared to an expected +5.8% at the end of 2021) and sales growth of 10.7%. The price/earnings ratio of expected corporate earnings over the next 12 months is currently 18.5 (slightly below the 5-year average of 18.6 but above the 10-year average of 16.8). The US composite purchasing managers' index was surprisingly robust in February 2022 with a value of 55.9. It was driven equally by the services and industrial sectors. Inflation figures in February 2022 rose further to 7.9% (January 7.5%). Food and rental costs were among the biggest price drivers. This is the highest inflation in 40 years. No wonder the US Fed has now shifted its focus from full employment to fighting inflation. After the first rate hike of 0.25% decided on 16.3., 5 further rate hikes of 0.25% each are expected in 2022 to a target range of 1.5 to 1.75%. Inflation expectations over 10 years currently risen to 2.9% and now require decisive action by the Fed.

Our conclusion: We expect price pressure to ease in the summer months due to the pandemic and energy-related supply bottlenecks. In the second half of the year, we expect the stock market to rise again due to falling inflation figures and moderate growth.

Source: FuW

China

China slows down

According to official figures, China's economy grew by 8.1% in the past year, as reported by the Beijing statistics office. The growth of the gross domestic product was slightly better than analysts had expected on average. However, growth weakened significantly in the fourth quarter. The start of the new year was weak. Virus containment measures have slowed down the service sector in particular. Companies' earnings outlook is clouded by increasing Covid 19 outbreaks as well as lockdowns in metropolises like Shenzhen. Growth will also be hampered by falling investment in the real estate sector this year. The housing starts index does not signal a recovery until 2023, and the central bank will consider cutting short-term interest rates further to support the economy.

Our conclusion: Economic forecasts are lowered despite the expected fiscal stimulus and monetary easing. For 2022, GDP growth forecasts are below 5%. China's role in connection with the war in Ukraine is still unclear. A concession by China towards Russia could lead to countermeasures by the West towards Chinese companies or even sanctions against China. The US Securities and Exchange Commission (SEC) is increasing pressure against companies that refuse to open their books to US authorities. This is fuelling concerns about delisting of Chinese companies from US stock exchanges and has led to severe stock market turbulence. The risks for investments in China have increased significantly.

Source: Zurich Cantonal Bank

Japan

How to continue with a positive trend in times of uncertainty

The Japanese economy rebounded in the final quarter of 2021, albeit at a slower pace than expected. In the world's third-largest economy, GDP rose by 5.4% in 2021. This is the first time in three years that Japan's economy has grown. Last year, Japan's economy oscillated between growth and contraction from quarter to quarter, mirroring the ripples of the Corona pandemic. Rising commodity prices, Corona and supply shortages were the main drivers. In the last quarter of 2021, private consumption recovered and the impact of the pandemic weakened. The IMF (International Monetary Fund) said in its latest update that the recovery was due to strong and timely policy support. For this year, the IMF expects Japan to grow by 3.3% as policies remain supportive and vaccination rates are high. At this stage, it is not possible to say how the Russian crisis will affect the country. The domestic stock index has lost around 10% so far.

Mimi Haas, lic. rer. pol. HSG, M.A. in Banking and Finance

Our conclusion: If the trends remain positive, Japan may become interesting for an equity investment.

Source: FuW, Financial Times, Market Map

Emerging Markets

Inflation fears

The GDP growth rates for the fourth quarter surprised positively both in the Asian region and in Latin America. The start into the new year has been successful and countries such as Brazil, Colombia and India are convincing with continued high economic momentum. On the other hand, the central banks are concerned about the higher prices for energy and basic foodstuffs. In Brazil, for example, the annual inflation rate has exceeded 10%. Rising inflation rates are constantly being combated with new rounds of interest rate hikes. Currently, key interest rates are being raised by an average of 50 basis points per rate hike.

Our conclusion: The war in Ukraine may have a negative impact on global growth and inflation, mainly due to rising energy prices. Emerging markets are more exposed and vulnerable. We do not recommend new investments in emerging markets.

As of: 15.03.2022

Source: Statista

Stocks

Russia as game changer

The conflict between Russia and Ukraine occurred at a time when most of the world had overcome the Covid pandemic. Monetary policy normalisation, reflected in sharply rising real yields, was initially the main impetus for stock markets since the beginning of the year - until Russia launched the military attack on Ukraine, which was unimaginable to many. This conflict, as well as the far-reaching sanctions and corporate measures to isolate the Russian economy, sent commodity prices soaring and intensified inflationary pressures and supply shortages with far-reaching effects. Moreover, this pointless conflict comes at an inopportune time for the Fed: looking ahead to this week's Fed meeting, the Bank will tighten monetary policy at a time of weaker consumer sentiment, and yet its core objective - containing inflation - is unlikely to be achieved any time soon.The IMF already reacted to the price rises in January, cutting growth forecasts for 2022 in favour of 2023 sharply and moderately for the US and for Europe and Asia. Nevertheless, our baseline scenario does not foresee a recession in 2022 and 2023. However, the risk of stagflation has increased, which is related to the indeterminate long-term impact of the conflict and may be poison for equity returns. What is remarkable is the global determination of shareholders, consumers and company managements, with the exception of China, to partially or totally disengage from the Russian market. This "voluntary" sales disengagement will impact sales and profits in the short term. Current EPS growth forecasts are therefore likely to be revised downwards by companies and analysts in the coming months. The S&P 500 closed on Monday with a PE of 18.6x, which is a significant depreciation since the beginning of the year. We believe that most of these future adjustments have already been priced into the markets. European stock markets, for example, have already lost between 13% and 16% on average. The Chinese markets and the US technology exchanges have already corrected by up to 20%.

Our conclusion: As long as the extent of the conflict is not completely clear, the markets can overshoot to the downside. Once the bottom is reached, markets will reassess the new realities. One positive fact is that the US and European economies are growing and maintaining employment momentum. Economic easing measures should now be imposed with extreme caution. Commodity price spikes are also a signal for markets to increase production. This is true for oil producers, farmers and even commodity producers such as car manufacturers. This is all part of a market mechanism that reallocates resources to meet demand. Finally, periods of high uncertainty and negative news are usually followed by a period of higher investment returns. "Market timing" - the complete switch between cash and investments - becomes pure speculation with daily fluctuations of 3% in global equity prices and quadruple volatility in major commodities until prices rebalance. In our view, it is better to complement equity and bond portfolios with inflation hedges. Our model (CAIB) is forecasting a neutral trend overall and in the short term, and is slightly positive on a 12-month horizon. Due to the current low valuations and the opportunity profile, we are overweighting quality European equities, which will continue to have good growth potential due to nearshoring.

As of: 15.03.2022

Source: Chefinvest AG, Zurich, Market Map

Interest

Rising oil price and inflation bring significant volatility

Government bonds

The Russian invasion of Ukraine triggered strong risk aversion. In many regions, nominal benchmark yields are likely to be further supported by high global inflation and the post-COVID recovery over time.

Higher real yields pose a significant risk to bonds and other markets.

Economic growth in the Eurozone is likely to be affected by rising commodity prices and the side effects of sanctions. Fiscal policy tools are likely to be used to cushion high energy prices, allowing the ECB to maintain moderate monetary policy in the short term. In the US, high inflation and solid economic growth should support the Fed's restrictive stance. This leaves room for higher yields on US Treasuries.

Our conclusion: We see the attractiveness of government bonds depending on the respective interest rate hikes.

Investment grade bonds (IG)

The positive fundamental factors of global IG bonds should cushion the drag from the change in monetary policy direction. However, this robustness in spreads does not mean an immediate return to spread tightening. For bond funds, a wave of redemptions has probably begun and should continue for a few more weeks until investors adjust to the Fed's balance sheet reduction. Our concern remains the extreme risk of accelerated liquidity withdrawal combined with weak growth expectations and geopolitical uncertainty. This could trigger a widening of credit spreads, especially in longer-dated areas.

Our conclusion: We are cautious on investment-grade (IG) bonds at the moment.

High-yield bonds

(HY) Solid credit data, especially in US HY energy stocks, should offset recent macroeconomic uncertainties. However, the extreme risk of an abrupt widening of spreads, especially in longer-dated areas, is increasing. Geopolitical tensions complicate the already precarious balance of the domestic economic outlook, significant corporate pricing power and the withdrawal of expansionary monetary policy by central banks to curb inflation.

Our conclusion: We believe high-quality HY corporate bonds can provide good diversification in a bond portfolio.

Emerging-markets bonds

(EM) The recent sharp widening of Russian and Ukrainian credit spreads has put additional pressure on EM HW government bond spreads. Growth concerns and higher inflation rates added to this worry. The wider spreads have improved valuations. However, they are not yet attractive enough to justify a more positive view on the asset class given current geopolitical risks. The withdrawal of capital from specialised emerging market bond funds has accelerated as a result of recent events. They are likely to remain under pressure in the short term. The asset class usually outperforms when the Fed has started raising interest rates.

Maria Albericci, Chairman/Managing Director

Our conclusion: We consider it premature to bet on emerging market (EM) bonds.

Currencies

Safe Haven, Central Banks and War, Drivers of Currencies

Currencies are in the playground of the geopolitical situation and central banks at the moment. Safe havens in currencies are making a comeback.

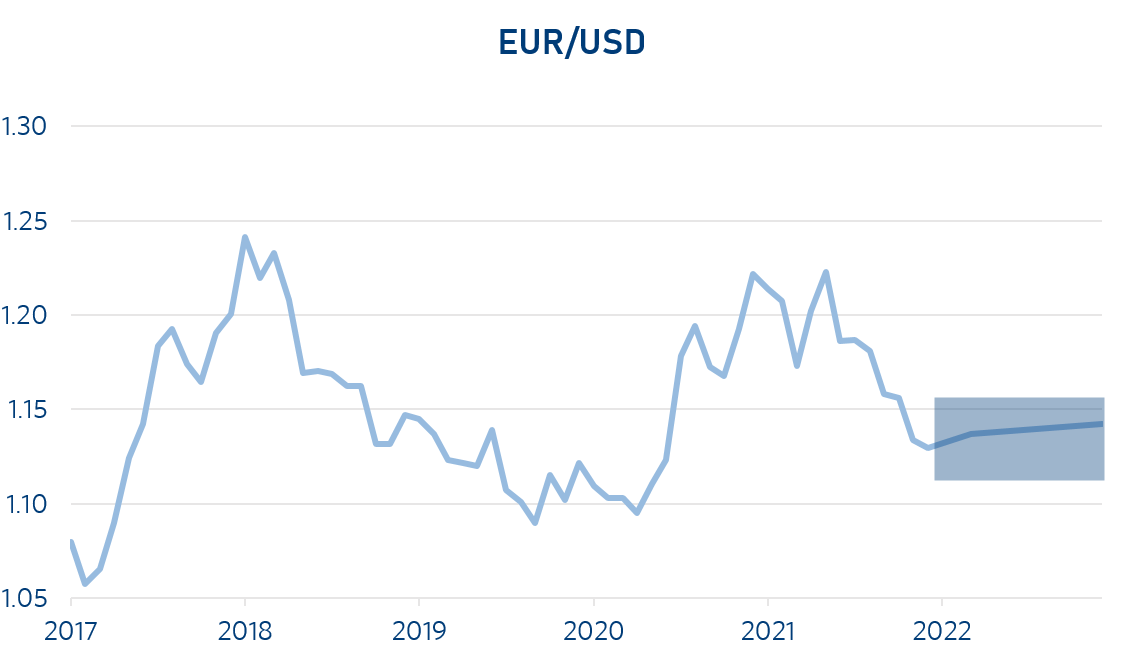

EUR/USD (currently 1.09)

The euro continues to fall against the greenback, which is considered a safe haven. The FED will raise interest rates this year, which will again provide investors with new investment opportunities in USD.

Our conclusion: The expected interest rate differential and the geopolitical situation continue to strengthen the dollar.

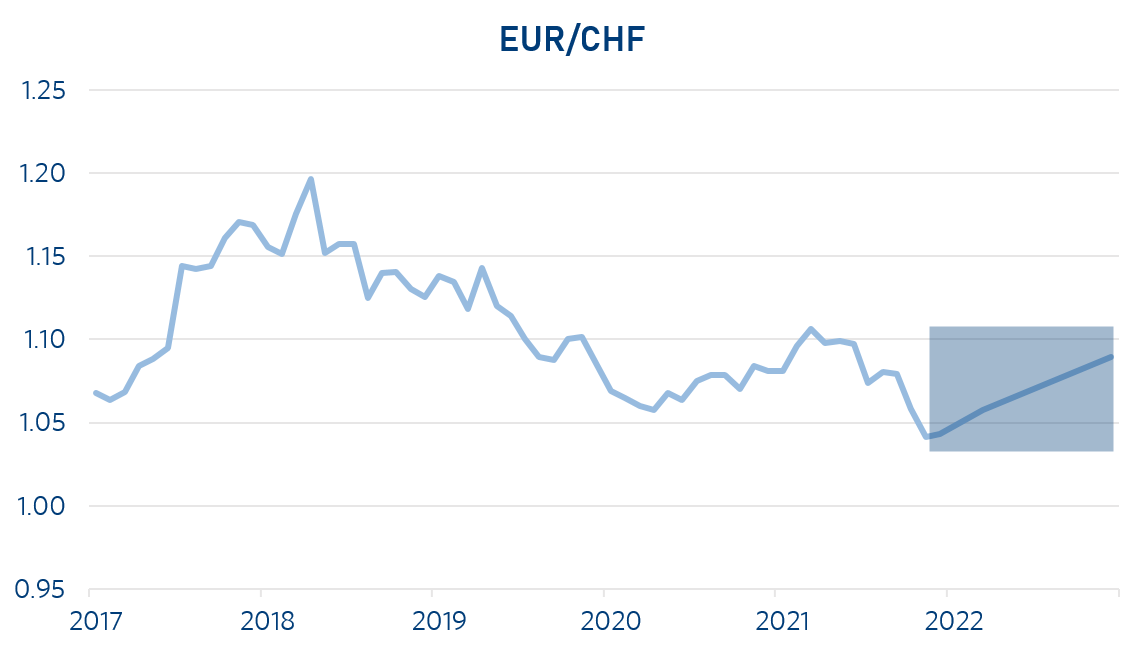

EUR/CHF (currently 1.024)

After the military attack it took a few days for the franc to move against the EUR. At times we could even see parity. It is a clear euro weakness and not a classic franc strength. The current price movement cannot be explained by current valuations, but is the result of the flight to safe havens, like the franc. Since the strength of the franc remains without serious consequences at the moment, it is not to be expected that the central bank will intervene, as it did in the past.

Our conclusion: as long as the military intervention continues and no solution is in sight, the franc will remain strong.

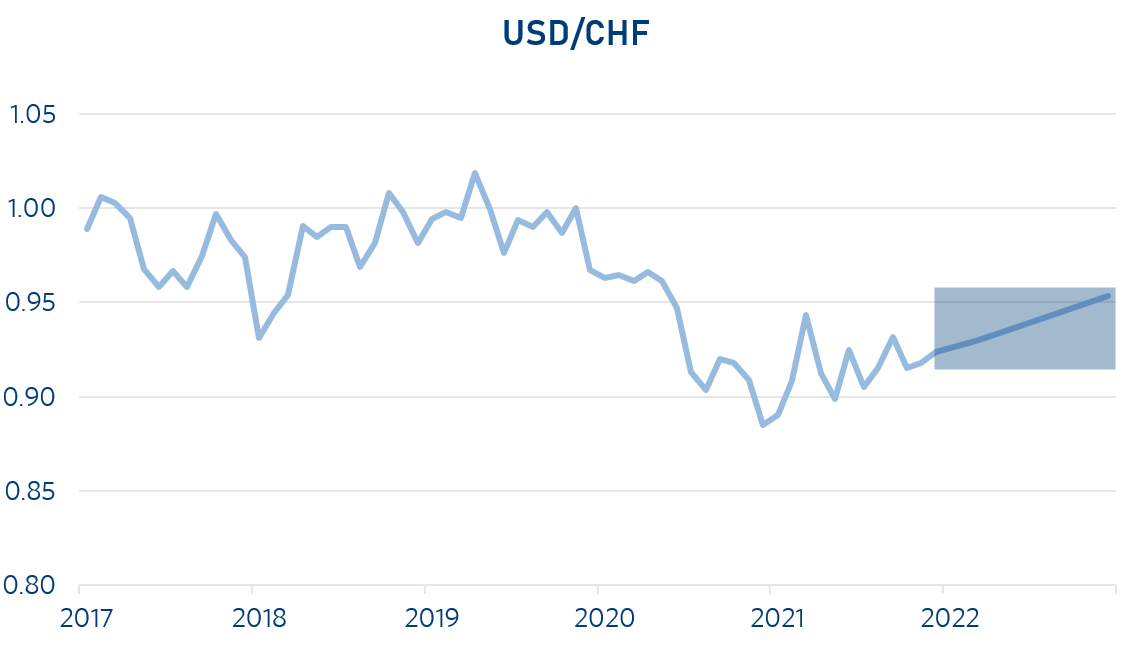

USD/CHF (currently 0.94)

The USD continues to be strong against the CHF. The persistent and high inflation in the USA is visibly forcing the US Federal Reserve to tighten monetary policy earlier and more strongly. The USD is benefiting from this, especially against low interest rate currencies such as the CHF.

Mimi Haas, lic. rer. pol. HSG, M.A. in Banking and Finance

Our conclusion: We expect this to continue.

As of: 15.03.2022

Source: Chefinvest AG, Zurich, Market Map

Oil

The come back of fracking?

The oil price for Brent and WTI have risen above 100 USD. In real terms, this has only been surpassed in 1979/1980, 2006 -2008 and 2011 - 2014. With 11.3 million barrels of oil per day, Russia is a very important oil producer (Sokol grade). The boycott of Russian oil decided by the USA and England affects them immensely less than Europe, which is why it is less likely that Europe will join the embargo. The fracking companies in the USA are cautious despite the high prices because of past experience. They are only expected to produce 760,000 barrels of oil per day more in 2022. Of the OPEC countries, only Saudi Arabia, the UAE and Iran have production reserves of more than 1 million barrels per day. The strategic emergency reserves of the member countries of the International Energy Agency (IEA) amount to 1.5 billion barrels of oil. The release of 60 million barrels of oil at the beginning of March was probably more of a symbolic act.

Our conclusion: We expect oil prices to fall well below USD 100 per barrel again in the second half of the year as a result of a calming of the geopolitical situation and a normalisation of supply and demand.

Precious Metals

Gold shines

Gold has proven its quality as a safe haven in recent weeks. The price per ounce reached USD 2,050 at the beginning of March. In the last few days it has weakened again to USD 1,920 per ounce. Platinum reached an ounce price of USD 1,150 at the beginning of March, but has weakened again to USD 1,000 per ounce in recent days due to its more cyclical character. A sustained economic cycle, especially in the automotive sector, is necessary for a renewed upward trend.

Andreas Betschart, Business Manager

Our conclusion: We expect firm gold prices in the coming months with a trading range of USD 1,850 to 2050 per ounce. For platinum, we see a price range of USD 900 to 1,100 per ounce in the coming months.

As of: 15.03.2022

Source: Chefinvest AG, Zurich, Market Map

Abbreviations and explanations

bbl: 1 Barrell = 158,987294928 Litre

Bp: Basis points

GDP: Gross domestic products

BIZ: the Bank for International Settlements is an international financial organization. Membership is reserved for central banks or similar institutions.

EM-Bonds: Emerging market bonds. An emerging market is a country that is traditionally still counted as a developing country but no longer has its typical characteristics.

HY-Bonds: Fixed-income securities of poorer credit quality. They are rated BB+ or worse by the rating agencies.

IG-Bonds: Investment grade bonds are all bonds with a good to very good credit rating (Ra-ting). The investment grade range is defined as the rating classes AAA to BBB-.

IHS Markit: Listed data information services company

IWF: The International Monetary Fund (also known as the International Monetary Fund) is a legally, organiza-tionally, and financially independent specialized agency of the United Nations headquartered in the United States of America.

KOF: Business Cycle Research Centre at ETH Zurich

LIBOR: London Interbank Offered Rate is a reference interest rate determined in London on all banking days under certain conditions, which is used, among other things, as the basis for calculating the interest rate on loans.

OPEC: Organization of the Petroleum Exporting Countries

OPEC+: Cooperation with non-OPEC countries such as Russia, Kazakhstan, Mexico and Oman.

oz: the troy ounce is used for precious metals as a unit of measurement and is equal to 31.1034768 grams

Saron: The Swiss Average Rate Overnight is a reference interest rate for the Swiss franc

Seco: Swiss State Secretariat for Economic Affairs

Spread: Difference between two comparable economic variables

WTI: West Texas Intermediate. High-quality US crude oil grade with a low sulfur content.

Disclaimer:

The information and opinions have been produced by Chefinvest AG and are subject to change. The report is published for information purposes only and is neither an offer nor a solicitation to buy or sell any securities or a specific trading strategy in any jurisdiction. It has been prepared without regard to the objectives, financial situations or needs of any particular investor. Although the information is derived from sources that Chefinvest AG believes to be reliable, no representation is made that such information is accurate or complete. Chefinvest AG does not assume any liability for losses resulting from the use of this report. The prices and values of the investments described and the returns that may be received will fluctuate, rise or fall. Nothing in this report is legal, accounting or tax advice or a representation that any investment or strategy is appropriate to personal circumstances or a personal recommendation for specific investors. Foreign exchange rates and foreign currencies may adversely affect value, price or yield. Investments in emerging markets are speculative and involve considerably greater risk than investments in established markets. The risks are not necessarily limited to: Political and economic risks, as well as credit, currency and market risks. Chefinvest AG recommends investors to make an independent assessment of the specific financial risks as well as the legal, credit, tax and accounting consequences. Neither this document nor a copy of it may be sent in the United States and/or in Japan and they may not be handed over or shown to any American citizen. This document may not be reproduced in whole or in part without the permission of Chefinvest AG.