Click on the images to view our comments on each topic.

Switzerland

Solid economic growth

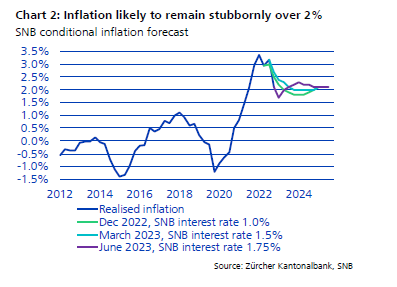

The Swiss economy is robust. Employment growth was surprisingly positive and unemployment is at a low of 1.90%. Consumer spending is at a high level and exports increased strongly. The export industry is supported by the flourishing pharmaceutical and chemical industries as well as by watch exports. Negative factors are the shortage of skilled employees and the inflation-related loss of purchasing power in some large markets. The leading indicators signal a slowdown in the manufacturing sector. High net immigration and the stable service sector ensure that the Swiss economy will continue to grow this year. The Swiss National Bank raised interest rates by another 25 basis points in June, bringing the key interest rate to 1.75%. Inflation is expected to average over 2.00% this year, slightly above the tolerance band of 0.00% to 2.00%.

SECO economic forecast

GDP 2023: +1.10% (E)

Inflation 2023: +2.40% (E)

SNB key interest rate: +1.75%

Our conclusion:

The SNB will counter the relatively high inflation rates with another interest rate hike in September. Declining energy prices and the strong Swiss franc are also contributing to an easing on the inflation front. The first companies delivered solid results for the first half of the year in July. The Swiss equity market is valued low by historical standards and offers good long-term investment opportunities.

Sources: OECD and SECO

As of 17.07.2023

European Union

Slight brightening of the economy expected

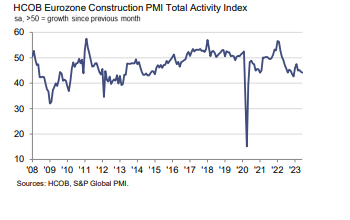

In the Eurozone economic output fell by 0.10% in the first quarter compared to the previous quarter. The currency area has thus slipped into a so-called technical recession. Economists speak of a technical recession when the gross domestic product (GDP) shrinks in two consecutive quarters. However, the recession is still very mild. Economists had expected stagnation. Year-on-year, the economy grew by a revised 1.00% in the period from January to the end of March. From a regional perspective, Germany's recession in the winter half-year in particular weighed on the Eurozone economy. Due to the high importance of industry, Germany suffers particularly from the global reduction of inventory capacities. On the other hand, Spain and Italy supported growth in the first half of the year. Both countries continue to benefit from the inflow of substantial funds from the EU reconstruction plan. The labour market remains robust. The average unemployment rate at the end of May was at an all-time low of 5.90% in the European Union (EU) and 6.50% in the Euro area. Inflation in the Eurozone continued to ease in June. It increased by 5.50% compared to the previous year. In May, inflation had stood at 6.10%. In contrast to headline inflation, core inflation, which excludes volatile prices for goods such as energy, rose again. It rose from 5.30% to 5.40% after falling in the previous two months. In detail, however, the upward price trend weakened broadly. Only for services was it higher than in the previous month, at 5.40%. Food and beverages, on the other hand, rose less strongly, as did industrially manufactured goods. Energy prices even fell significantly by 5.60%. A fading upswing in the service sector and declining industrial production caused stagnation in the Eurozone in June. At 49.90 points, down from 52.80 points in May, the seasonally adjusted HCOB Composite PMI for the Eurozone signalled that economic growth stalled in June.

GDP growth 2023: +0.90% (E)

EU Inflation 2023: +5.40% (E)

Current 3-month Libor: +3.66%

Our conclusion:

The Euro area economy weakened slightly at the turn of the year. However, it has proved relatively resilient to the pronounced negative supply shocks that have hit the economy. In the near term, economic growth is expected to remain weak, but to pick up in an environment of falling inflation and easing supply disruptions in H2. The situation varies across sectors. In manufacturing, activity continues to cool, reflecting lower global demand and tighter financing conditions in the Euro area. The services sector continues to be robust. The labour market will continue to provide a strong stimulus to the economy. Almost one million new jobs were created in the first quarter of 2023. In June Eurosystem staff macroeconomic projections, the outlook for GDP growth has been revised slightly downwards for 2023 and 2024 and left unchanged for 2025. However, a significant economic slump is not implied. They assume that the average annual growth rate of real GDP will fall to 0.90% in 2023 (after 3.50% in 2022) and then pick up to 1.50% in 2024 and 1.60% in 2025. The ECB has raised interest rates in the Euro area eight times in a row since July 2022 - most recently at its meeting in mid-June by 0.25 percentage points each time. The key policy rate, the rate at which commercial banks can borrow money from the ECB, rose to 4.40%, while the key rate for banks that deposit their money at the ECB rose to 3.50%. ECB President Lagarde said after the June meeting that another rate hike was "very likely". She warned against a "too rapid" change in monetary policy given the persistently high inflation in the Euro area. The next ECB interest rate meeting is scheduled for 27 July. As for inflation expectations, the ECB expects headline inflation to average 5.40% in 2023, 3.00% in 2024 and 2.20% in 2025. The downward effect from lower energy price assumptions is more than offset by upward revisions in food and core inflation. Price pressures remain strong. Core inflation is projected to be 5.10% in 2023, before falling to 3.00% in 2024 and 2.30% in 2025.

Daniel Beck, Member of the Executive Board

Source: European Commission, Statista and S&P Global

As of 17.07.2023

United Kingdom

USA

The bulls are back

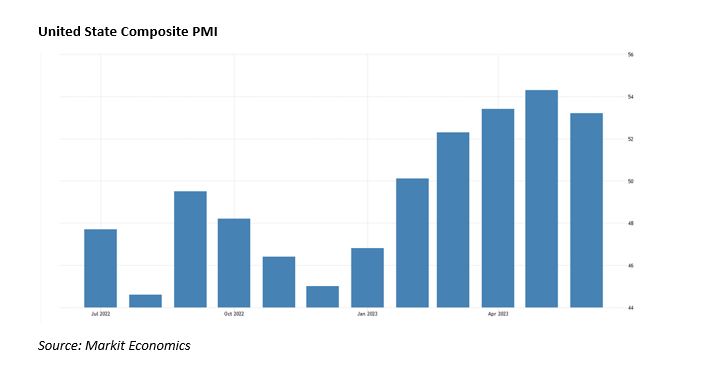

According to Markit Economics, the S&P Global US Composite PMI reached 53.20 points in June (0.20 points better than expected but 1.30 points lower than in May). The good performance was again due to the services sector, which weakened slightly from 54.90 to a still solid 54.40 points in June compared to the previous month. The manufacturing sector, on the other hand, weakened further in this period from 48.40 to 46.30 points and is thus clearly below the expansion threshold of 50. Fortunately, the leading economic index still indicates expanding economic activity, despite the Fed's restrictive monetary policy. The inflation rate fell by a further 1.00% to 3.00% in June compared to the previous month (3.10% was expected). The core rate (excluding food and energy), on the other hand, declined only slightly by 0.50% to 4.80% in this period. A decline of the growth rate in the rent-increases, which were still responsible for more than 50% of core inflation in June, will also lower the core rate further in the second half of the year due to the basis effect.

The US labour market is in excellent shape despite the sharp rise in interest rates. The unemployment rate in June was 3.60% (May 3.70%) and 209,000 new jobs were still created in June (excluding agriculture). While this shows an expected slowdown in the labour market due to the Fed's monetary policy braking manoeuvre, it also shows a still astonishing resilience. There are still almost twice as many job offerings as job seekers, but this also indicates that wages may continue to rise. At the Fed's last meeting on 14.6.2023, as expected, the Fed took a pause in the more than year-long cycle of rate hikes. However, Chairman Jerome Powell made it clear that this was probably only a pause and that one to two more rate hikes of 0.25% each could be expected this year. In the market, however, only a rate hike from 5.25% to 5.50% is currently expected for the upper band of the Fed Fund Rate at the next meeting of the central bank on 26 July. For the second quarter of 2023, analysts expect an average earnings decline of 7.10% for the companies represented in the S&P 500 Index, according to Factset. However, the first published earnings figures indicate a much smaller decline of just under 2.00% due to better than expected figures. Positive earnings growth is then expected again from the 3rd quarter onwards. GDP grew by 2.00% in the first quarter of 2023. According to the GDP Now Model of the Federal Reserve Bank of Atlanta, it should even be 2.30% in the second quarter.

GDP 2023(IMF): +1.60% (E)

Inflation 2023(IMF): +4.50% (E)

Fed Fund Rate: +5.25%

Our conclusion:

The US economy and labour market are defying the monetary headwinds surprisingly well. This probably also has to do with the billion-dollar post-pandemic fiscal packages. Whether the long-predicted economic slowdown (soft landing) or even an actual recession will occur, depend on further declining inflation rates and the resulting leeway for the Fed to lower interest rates. We expect inflation rates to continue to fall in the coming months. Meanwhile, rising corporate earnings will support equity valuations in the second half of the year.

Dr. Patrick Huser, CEO

Sources: Markit Economics, IMF World Economic Outlook July 2023, FactSet

As of 17.07.2023

China

Catch-up effects

The national economy grew by only 0.80% in the second quarter compared to the first quarter. The government's target of 5.00% growth this year seems very ambitious. Hopes, after a good start in Q1, have faded. Domestic demand is weak and things are not going well in the real estate sector either. Construction investments are lower than in the previous year and the vacancy rate has not yet decreased. The unemployment rate has risen sharply among young people and is over 20.00%. Foreign direct investment has slumped since the beginning of the year and exports are also shrinking. Overall, the data situation is poor and has led the central bank to cut the key interest rate in June. According to statements by the deputy governor, counter - cyclical adjustments will be stepped up. Lending to SMEs is to be stimulated.

IMF Economic Forecast

GDP 2023: +5.20% (E)

Inflation 2023: +2.00% (E)

3 Month Shibor: +2.10%

Our conclusion:

The Chinese economy came under pressure in Q2. As inflation is zero, unlike in other economies, the central bank has the leeway to cut interest rates to stimulate the economy. The YUAN has depreciated against the USD and the EURO. This could support the export industry. The low valuation of the Chinese equity market reflects the tense economic situation and political risks. We currently do not recommend investing in the Chinese market.

Sources: IMF and LLB

As of 17.07.2023

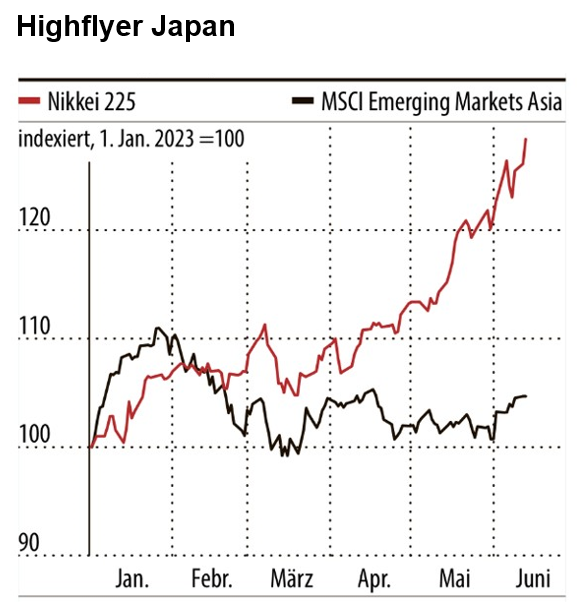

Japan

The Japanese National Bank is taking its special path, are they right?

Japan is the only country that continues to use negative interest rates and intervenes with bond purchases. Decades of experience with deflation have shaped the Japanese strategy and they are patiently pursuing their monetary policy, even though core inflation remains stubbornly above 3.00%. The YEN has already lost about 8.00% of its value against the US-dollar this year. This creates an advantage for Japanese exporters in particular. They can maintain or expand their margins despite the increased prices, which means that the economic engine is currently running hot. In the first quarter, Japan's GDP grew by an annualised 1.60% in real terms compared to the previous quarter; hardly any other industrialised country can keep up. Japanese companies are increasingly distributing their cash reserves to shareholders. The P/E ratio of around 15 remains rather low for equities. This all leads to a high in the stock market.

GDP 2023: +1.60% (E)

Inflation 2023: +1.60% (E)

3 Month Tona Rate: -0.03%

Our conclusion: Still positive

Japan is still undervalued and underrepresented in portfolios compared to other markets. The market offers a good opportunity for medium-term investors. Even if the potential is lower than at the beginning of 2023.

Mimi Haas, Lic.rer.pol. HSG, M.A. in Banking and Finance HSG, Partner

Sources: F&W, JP Morgan and Bloomberg

Emerging Markets

Economic trough overcome

In the last few months, inflation has receded thanks to falling food, energy and goods prices. After some central banks were forced to aggressively raise interest rates as early as 2021, there are now signs of easing. In Latin America, the first rate cuts could be announced in the coming months, while in Asian countries they are not expected until next year. Overall, the economic data in the first quarter were surprising and the economy is likely to have picked up in the second quarter, so that economic growth of almost 5.00% for the whole year seems realistic, especially for the Asian countries. Many countries there will benefit from investment from the west as supply chains are rebuilt to reduce a one-sided dependence on China. This will take many years.

Our conclusion:

The economic outlook has brightened, especially in Asian countries. Equity markets are favourably valued.

Sources: IMF and LLB

As of 17.07.2023

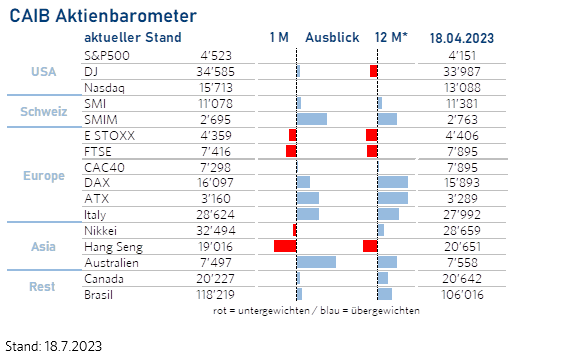

Stocks

Game Change?

The global economy has exceeded the pessimistic expectations of most investors. The biggest fears did not materialise: The US Treasury was able to replenish its coffers by more than $500 billion thanks to a debt ceiling agreement. Nota bene without siphoning off bank deposits, as short-term lenders reduced their use of a key Fed credit facility overnight. And globally, there is a sharp fall in inflation due to lower energy prices, even if the core rate has not yet fallen to the desired level. The good news here is that a fall in core inflation is imminent. Thus, interest rate hikes are now expected to be enforced less aggressively and some central banks will start to move away from restrictive monetary policy in 2024. Even labour markets are slowly easing, although employment rates remain high. Some stock markets are even benefiting at the moment from the fact that inflation is slowing faster than the labour market. In the coming weeks, the quarterly reports of large US technology companies, industrials and retailers will be published. In the process, Wall Street analysts' estimates for the upcoming earnings reports have already been reduced somewhat in Q2. Still, with inflation falling and the economy weakening, it will be somewhat more difficult for companies to maintain profit margins. Of course, corporate profits in Q3 may surprise, but it will take a special effort for many companies to reach their projected full-year profit numbers. In fact, the use of artificial intelligence can become a key element in this. Through improved production processes, faster analysis and efficiency gains, some companies are already able to increase revenue potential and reduce costs. They are gaining a competitive advantage. At the same time, the use of artificial intelligence can also increase competitive pressure within industries. In any case, it is a game changer.

Our conclusion: buy selectively

Although some US securities houses are increasing their equity exposure worldwide due to the looming interest rate easing, we are somewhat more cautious in the short term. At 0.07, our CAIB Index shows a slightly weaker opportunity plus than in the last survey, but it is still in positive territory. In the longer term (12 months), we see a better opportunity plus of +0.10 and recommend equity investments in European countries. We assume that companies in general will be able to optimise their processes due to the increased use of artificial intelligence and thus increase efficiency and earnings power. Here we consider the most promising opportunities to be in the Capital Goods, General Retail, Telecoms, Tech/Hardware, Semiconductors, Medical Devices and Luxury Goods sectors.

Sources: S&P, Citigroup, MarketMap, IMF, and Chefinvest

As of 17.07.2023

Interest

A new stabiliser in the portfolio!

Market opinion and the opinion of the US Federal Reserve are drifting apart. While the market expects key interest rates to be 150 basis points lower by the end of 2024, the FED tends to believe that key interest rates will remain high. Who will be right?

Government bonds

Global government bond yields rose because of high inflation and relatively good global economic data. The rise in yields that has just taken place, has created an interesting entry point into this segment.

Our conclusion: We are rather positive on good global government bonds.

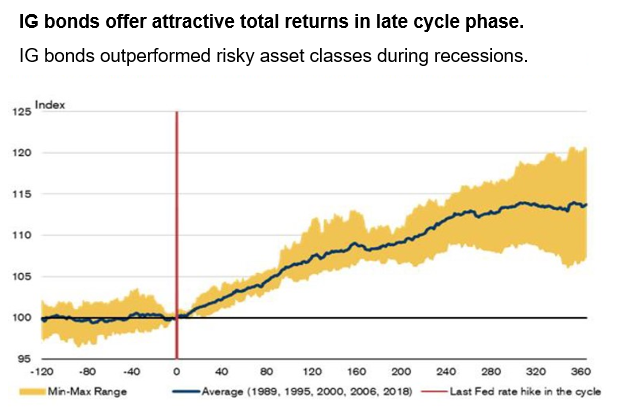

Investment-grade bonds (IG)

The gains of IGs have softened somewhat recently, but they can still offer attractive returns. We prefer high-quality bonds, as downgrade risk is growing in the existing economic environment and the investor is hardly compensated for additional risk.

Our conclusion: We remain positive on investment grade (IG) bonds, favouring those with shorter maturities and good credit quality.

High yield bonds (HY)

We continue to expect returns similar to money market investments. The default risk on HY bonds has increased with market developments and there is a risk of a further rating downgrade. The higher coupons do not compensate for this additional risk.

Our conclusion: We recommend avoiding this segment in the coming months.

Emerging market (EM)

EM bonds offer a yield premium for higher default and currency risk. Robust fundamentals and the expectation that there will not be a severe recession support this asset class. The higher coupons of this asset class compensate the investor for the higher risk. EM bonds benefit from the expectation that there will not be a deep recession and easing of pandemic policies in Asia. Therefore, they can offer attractive returns relative to risk in the future.

Our conclusion: We consider it attractive for riskier investors to invest in EM in hard currencies. To reduce the risk of default, ETFs should be considered and credit quality closely scrutinised.

Mimi Haas, Lic.rer.pol. HSG, M.A. in Banking and Finance HSG, Partner

Sources: MarketMap, Bloomberg and F&W

As of 17.07.2023

Currencies

Will the national banks soon put an end to interest rate hikes?

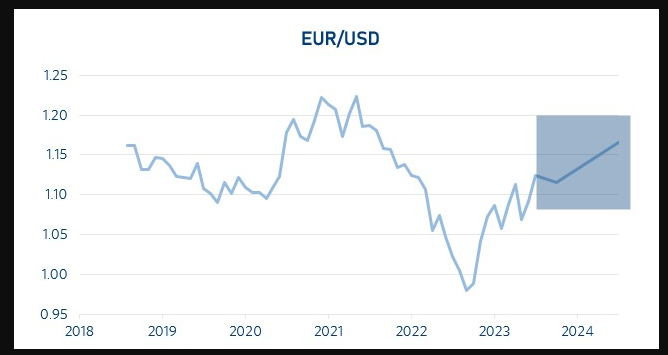

EUR/USD (20.07.2023: 1.12)

The EURO has recovered some of its losses from 2022 since the beginning of the year. For the further development of the currency pair, it is crucial whether the Fed starts to lower interest rates soon or whether it stays on the path of high interest rates. This means that the difference in interest rates will be decisive.

Our conclusion: We expect the currency pair to level off.

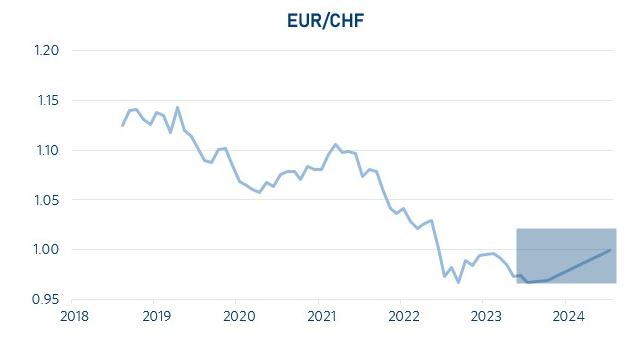

EUR/CHF (20.07.2023: 0.96)

The ECB is behind the Fed in its monetary tightening cycle. The SNB is more likely to continue to pursue a restrictive monetary policy. A positive factor for the CHF continues to be its valuable safe haven status in uncertain times.

Our conclusion: We expect the currency pair to level off.

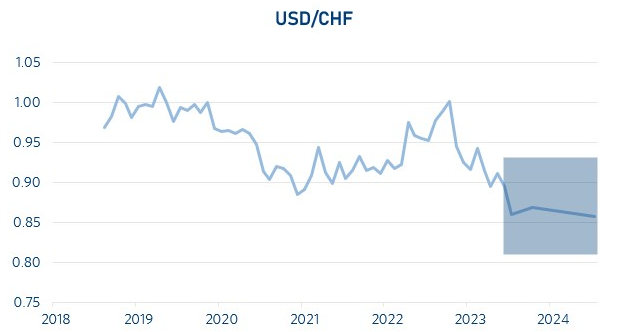

USD/CHF (20.07.2023: 0.86)

Inflation in Switzerland also rose in the first half of 2023, but nevertheless much more moderately than in the US. The reasons for this are that the SNB did not push economic stimulation too excessively during the pandemic, unlike the USA and the Eurozone. As a result, there was no completely excessive inflation of the money supply or monetary liquidity in Switzerland, as in many other countries. This means that Switzerland has caused far fewer inflationary drivers in 2020 and 2021 than the Eurozone and the USA. The interest rate spread between the US and Swiss key interest rates is high and will remain so in 2023.

Our conclusion: We expect the USD to move sideways against the CHF unless the Swiss National Bank changes its policy.

Mimi Haas, Lic.rer.pol. HSG, M.A. in Banking and Finance HSG, Partner

Sources: MarketMap, Bloomberg and F&W

As of 17.07.2023

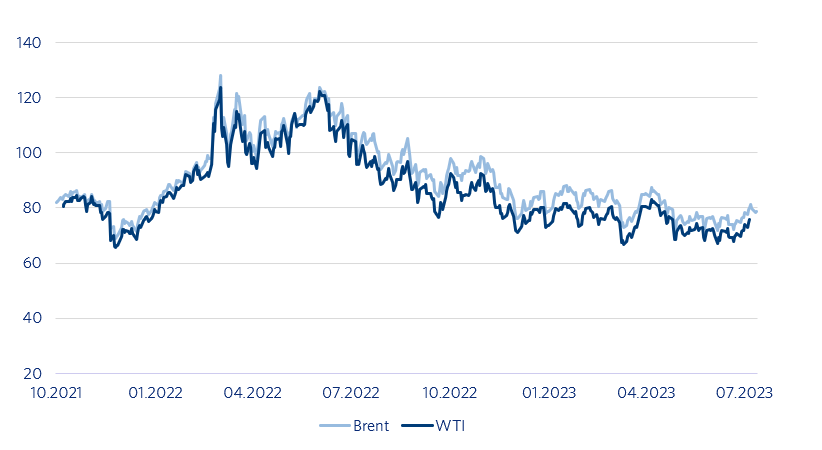

Oil

Demand weakens

Despite the announcement by Saudi Arabia respectively Russia to extend the production cuts of 1 million barrels per day decided in April until August respectively to cut exports by 500,000 barrels per day, the oil price has been moving sideways in recent months. This is due to the uncertain economic outlook and especially the weak growth in China. Subdued demand continues to balance the curbed supply.

Our conclusion:

We continue to expect a sideways movement at prices between USD 70.00 and 80.00 per barrel of WTI oil.

Sources: F&W, MarketMap

As of 17.07.2023

Precious Metals

Precious metal benefits from weak US dollar

Gold (on 18.7.2023 at USD 1'962/oz.) as well as platinum prices (on 18.7.2023 at USD 989/oz.) have trended upwards and gained in recent days. They were able to benefit from lower US employment figures as well as from the continued weakness of the US dollar. In the coming months, we will see whether the US Federal Reserve enters an easing cycle, which in the past has led to a revival of ETF demand and thus higher prices.

Our conclusion: Neutral

Gold and platinum can continue to be used as a hedge in the portfolio context and will continue to develop positively in the course of the coming months depending on the development of the economy and the US interest rate trend.

Andreas Betschart, Business Manager

Sources: UBS, Bloomberg

As of 17.07.2023

Abbreviations and explanations

bbl: 1 Barrell = 158,987294928 Litre

Bp: Basis points

GDP: Gross domestic products

BIZ: the Bank for International Settlements is an international financial organization. Membership is reserved for central banks or similar institutions.

EM-Bonds: Emerging market bonds. An emerging market is a country that is traditionally still counted as a developing country but no longer has its typical characteristics.

HY-Bonds: Fixed-income securities of poorer credit quality. They are rated BB+ or worse by the rating agencies.

IG-Bonds: Investment grade bonds are all bonds with a good to very good credit rating (Ra-ting). The investment grade range is defined as the rating classes AAA to BBB-.

IHS Markit: Listed data information services company

IWF: The International Monetary Fund (also known as the International Monetary Fund) is a legally, organiza-tionally, and financially independent specialized agency of the United Nations headquartered in the United States of America.

KOF: Business Cycle Research Centre at ETH Zurich

LIBOR: London Interbank Offered Rate is a reference interest rate determined in London on all banking days under certain conditions, which is used, among other things, as the basis for calculating the interest rate on loans.

OPEC: Organization of the Petroleum Exporting Countries

OPEC+: Cooperation with non-OPEC countries such as Russia, Kazakhstan, Mexico and Oman.

oz: the troy ounce is used for precious metals as a unit of measurement and is equal to 31.1034768 grams

Saron: The Swiss Average Rate Overnight is a reference interest rate for the Swiss franc

Seco: Swiss State Secretariat for Economic Affairs

Spread: Difference between two comparable economic variables

WTI: West Texas Intermediate. High-quality US crude oil grade with a low sulfur content.

Disclaimer:

The information and opinions have been produced by Chefinvest AG and are subject to change. The report is published for information purposes only and is neither an offer nor a solicitation to buy or sell any securities or a specific trading strategy in any jurisdiction. It has been prepared without regard to the objectives, financial situations or needs of any particular investor. Although the information is derived from sources that Chefinvest AG believes to be reliable, no representation is made that such information is accurate or complete. Chefinvest AG does not assume any liability for losses resulting from the use of this report. The prices and values of the investments described and the returns that may be received will fluctuate, rise or fall. Nothing in this report is legal, accounting or tax advice or a representation that any investment or strategy is appropriate to personal circumstances or a personal recommendation for specific investors. Foreign exchange rates and foreign currencies may adversely affect value, price or yield. Investments in emerging markets are speculative and involve considerably greater risk than investments in established markets. The risks are not necessarily limited to: Political and economic risks, as well as credit, currency and market risks. Chefinvest AG recommends investors to make an independent assessment of the specific financial risks as well as the legal, credit, tax and accounting consequences. Neither this document nor a copy of it may be sent in the United States and/or in Japan and they may not be handed over or shown to any American citizen. This document may not be reproduced in whole or in part without the permission of Chefinvest AG.