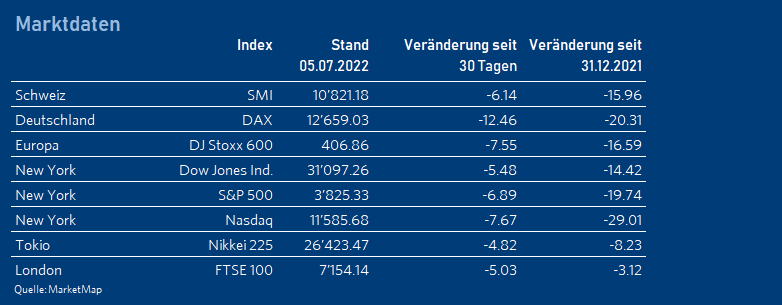

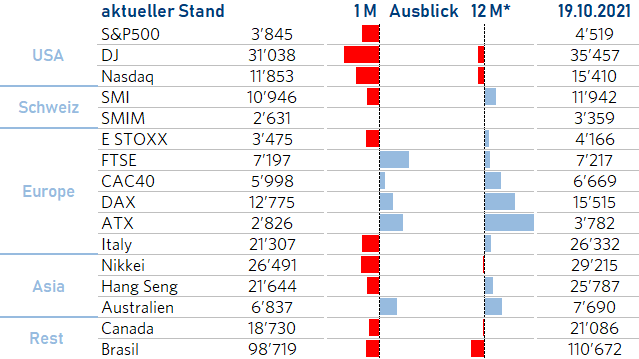

Click on the images to view our comments on each topic.

Switzerland

SNB acts independently

The SNB raised its key interest rate by 0.5% in mid-June and is expected to raise it further in the coming quarters. This increase was unexpected, both in terms of timing and magnitude. It shows that the assessment of the inflation forecast has changed significantly. The SNB's tighter monetary policy poses another downside risk to the Swiss economy, along with supply network disruptions and high commodity prices. The very low unemployment rate continues to boost private consumption and export activity remains strong. The SNB's inflation forecasts for 2023 are now at 1.9% and for 2024 at 1.6%. This should be reflected in further interest rate hikes, and in the key interest rate will remain in positive territory until the end of the year.

KOF economic forecast:

GDP 2022 + 2.8%

Inflation + 2.6%

SARON 3mt - 0.2% (SNB.ch)

Dino Marcesini, Partner

Our conclusion: The environment has become more challenging for companies. With the war in Ukraine and renewed lockdowns in China, previous supply network disruptions and raw material cost inflation have been further exacerbated. For 2022 as a whole, most turnover forecasts for Swiss companies remain strong. Price increases to date are boosting sales and protecting margins. Nevertheless, some profit warnings are to be expected for the second half of the year. Rising bond interest rates are weighing on the equity markets. The stock market will remain very volatile.

European Union

End of the negative interest rate policy

The Ukraine war and high inflation with ongoing global supply chain disruptions are severely affecting the relatively open European economy and have clouded the growth outlook. However, moderate growth is still being recorded. Private consumption has already suffered from high inflation in Q1, as this has led to significant real wage losses for consumers. Due to supply bottlenecks the industry was unable to fully utilise its production capacities.

Compared to the previous quarter, seasonally adjusted GDP increased by 0.3% in the Euro area and by 0.4% in the European Union (EU) in the first quarter of 2022. In the fourth quarter of 2021, GDP had increased by 0.3% in the Euro area and by 0.5% in the EU. In the first quarter of 2022, compared with the previous quarter, employment grew by 0.5% in the Euro area and by 0.4% in the EU. In the fourth quarter of 2021, employment grew by 0.4% in both the Euro area and the EU.

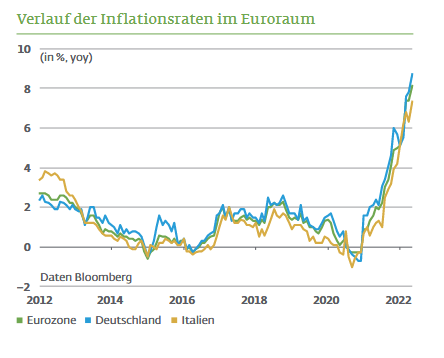

The headline inflation rate in the Euro area rose to 8.1% in May. The sharp rise in energy prices is one of the main causes, but price pressures have spread to many everyday goods (food, services, housing and travel).

In the Eurozone, economic growth slowed to a 16-month low in June due to stagnant demand. The S&P Global Flash Eurozone Composite PMI fell 2.9 points to 51.9 over the month, the lowest value since the recovery began 16 months ago and the second consecutive slowdown. Industrial production slowed for the first time in two years due to persistent supply bottlenecks and the service sector cooled noticeably.

Daniel Beck, Member of the Executive Board

Current inflation (ECB/HICP) + 8.1% (05.22)

Current 3-month Libor - 0.176%

GDP growth 2022 + 2.8% (E)

Our Conclusion: The European Central Bank (ECB) now expects real GDP growth of 2.8% for 2022 and 2.1% for 2023 and 2024. Compared to the March forecast, the outlook for 2022 and 2023 has been revised significantly lower by ./.0.9% and ./.0.7%, respectively. For 2024, an increase of + 0.5% was made.

Material and supply bottlenecks as well as high energy and commodity prices will continue to dampen trade and thus confidence and growth. However, there are reasons for economic growth: ongoing reopening of the economy, freedom to travel, good labour market situation, fiscal support and savings built up during the pandemic. After the current headwinds have abated, economic activity should pick up again.

At its June meeting, the ECB significantly raised its inflation forecasts. For the current year, the annual inflation rate will be expected with 6.8%, in 2023 with 3.5% and in 2024 with 2.1%. Average inflation excluding energy and food is projected to be 3.3% in 2022, 32.8% in 2023 and 2.3% in 2024.

For July, the ECB announced the first key interest rate hike in 11 years by 25 basis points (bp) to 0.25%. The ECB already stopped the end of the multi-billion bond purchases on July 1. However, in order to prevent a fragmentation of the Eurozone, the ECB has announced that it will use reinvestment under the Pandemic Emergency Programme (PEPP). The ECB will press the pace of monetary policy normalisation, as there is still no sign of an easing of inflation pressures. For September, we expect a further interest rate hike of 50 bp if inflation continues. The ECB's interest rate turnaround has already been priced into the financial markets and expectations point to rapidly rising interest rates. The markets are currently expecting key interest rate hikes in the Euro area of 200 bp within a year. The end of the negative interest rate policy is clearly in sight.

United Kingdom

USA

The Fed keeps inflation expectations in line

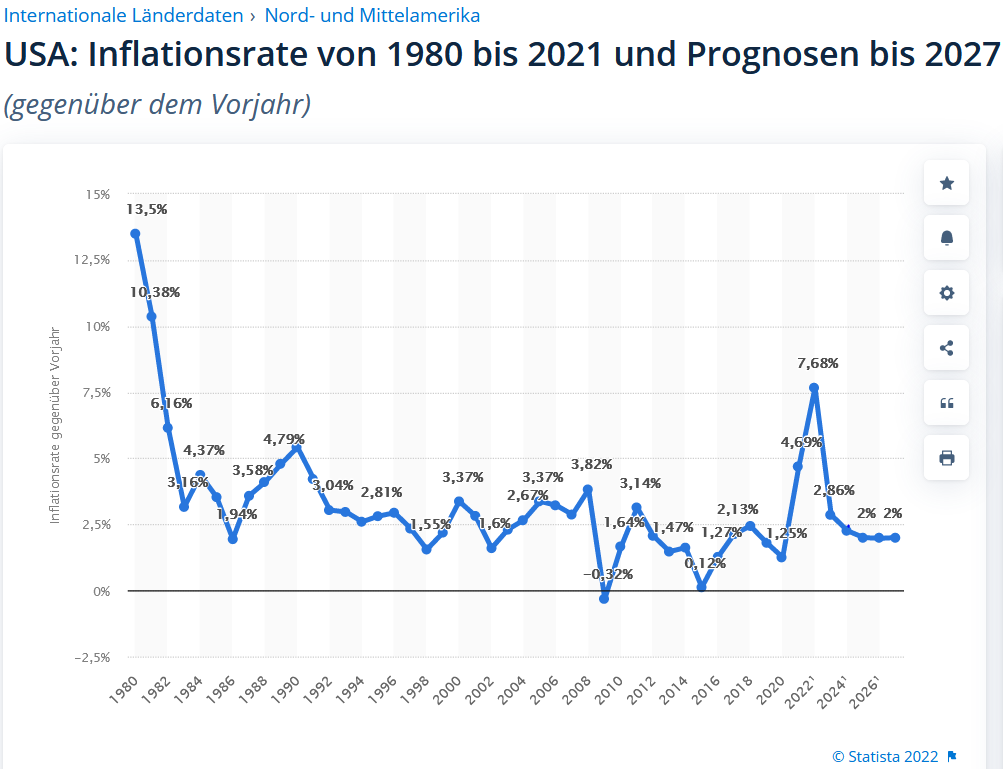

In June, the composite PMI for the US fell to 51.20 from 53.60 in May. The services component dropped from 53.40 to 51.6 and the industrial component from 57 to 52.70. This indicates a slowdown in economic activity but not yet a recession in 6 months (values above 50 signal economic growth). According to Factset, earnings growth of 4.1% is expected for the S&P 500 companies in Q2 2022, driven mainly by multiple energy companies. The price/earnings ratio of the S&P 500 based on expected earnings for the next 12 months is 15.8, which is 15% below the five-year average of 18.6 and 6.5% below the 10-year average. Unemployment in May was at a low of 3.6%, the same as in the previous two months. The labour market has been very robust, with two vacant positions for every job applicant. Inflation reached 8.6% in May, up 0.3% from April's rate, which was still down from March's rate of 0.2%. The Federal Reserve (Fed) then raised the Fed Fund Rate by 0.75% to 1.75% at its meeting on 15 June and held out the prospect of further decisive interest rate steps. It is now expected that the key interest rate will be raised to a total of 3.25 to 3.5% by the end of the year. The Fed's 'forward guidance' accelerates the adjustment process. Consequently, the Fed has reduced its growth forecast for the US economy to 1.75%. While the inflation rate in 2021 was 4.69%, an average value of 7.68% is expected for the current year. A significant decline to 2.85% is forecasted for 2023 and to 2.26% for 2024 (see also chart by Statista). Due to inflation and rising interest rates, most analysts expect a recession in the next 12 months with a probability of 40%. A mild recession now seems to be priced into stock prices. The S&P 500 Index is down 21% in the first half of the year, its the worst half-year performance since 1970. Countermovements due to excessive pessimism are therefore to be expected and possible at any time (the S&P 500 gained 27% in the second half of 1970).

Current inflation +8.6%

Fed Fund Rate +1.75%

GDP 2022 (E, IMF) +2.9%

Our conclusion: We expect economic growth to weaken, but demand will remain strong enough to absorb the interest rate hikes. Growth uncertainties will keep markets volatile in the coming weeks. A strong rebound can be expected as soon as the inflation figures start to recede.

China

Dawn in sight

The rigorous containment measures have been dismantled in many places, leading to an economic recovery. Production seems to be rapidly regaining its former strength. Consumption, on the other hand, is rather slow. This development has already been observed after previous outbreaks and, due to ongoing pandemic concerns, this pattern is likely to continue in the course of the year. Local governments are encouraged to make investments in infrastructure by the end of August. At the same time, monetary easing is in progress. Interbank rates have fallen significantly and the government is directing banks to expand lending. Thanks to the easing of the Corona restrictions, the stimulus should be unleashed in Q3, which will lead to a decent economic growth. The PMI Composite, which combines the industrial and services sectors, has already risen significantly in June from 42.2 to 55.3.

GDP 2022 + 4.5%

Inflation + 2.2

Central Bank Base Interest Rate 3Mt. + 3.7%

Our conclusion: China's economy is currently supported by an expansionary monetary policy, in contrast to the Western industrialised countries. This should also help stabilise the severely depressed property market and boost domestic consumption. However, export activity could weaken towards the end of the year from the slowing economic momentum of important trading partners. The stock market was able to recover from the lows.

Japan

All good in Japan?

Economic growth in Japan may recover slightly in the first half of 2022. However, the development is not straight upwards. Supply chain problems and geopolitical challenges continue to influence the situation after the pandemic, for example, industrial production in May 2022 fell by the most in two years compared to the previous month (production fell by 7.2, expected by analysts was 0.3). The picture is not much different in the areas of consumption, GDP and foreign trade. Investments are urgently needed in many areas to drive a sustainable recovery of Japan. Real GDP growth is still forecast to be around 2.39% year-on-year in 2022.

Japan's inflation was not yet a problem in the first months of this year, when figures were already rising in the Western world. In the last few months, however, it could be seen that it is also starting to rise and that the financial balance is also becoming more and more out of joint.

Mimi Haas, Lic. Rer.pol. HSG, M.A. in Banking and Finance HSG, Partner

Our conclusion: Japanese equities are not recommended as a buy in this environment.

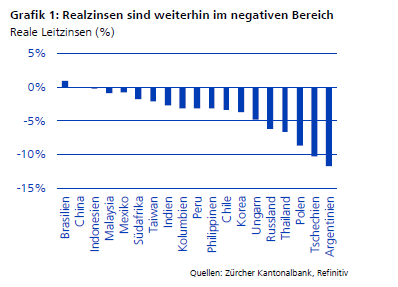

Emerging Markets

Light and shadow

Most central banks in Eastern Europe and Latin America have been raising interest rates massively since last year, whereas Asian monetary authorities have been hesitant so far. Domestic demand remains strong, leading to a rise in inflation. Therefore, central banks will have to increase interest rates further. But real interest rates are negative in virtually all emerging markets. At the same time, current account balances have turned from surplus to deficit as domestic demand recovers. The risk of currency devaluations has increased. Countries with high USD debts will find it difficult to serve the interest.

Our conclusion: Asian countries will have to raise key interest rates sharply to curb the threat of inflation. This is likely to hamper economic momentum and curb domestic consumption. Equity markets have underperformed in recent years and appear rather cheap at current levels.

Stocks

When will there be light at the end of the tunnel?

It is not difficult to review the market development in the first half of 2022 with concern: The coupled fear of galloping inflation and of the danger of recession in the economy has to be blamed for these market declines. The Fed's abrupt swing to a strongly hawkish stance additionally acted as an accelerant driving the market's steep decline in 2022. Given the likelihood that we will see two consecutive quarters of negative US GDP growth in 2022, it will not provide any real support for the stock markets either.

Will markets regain strength as inflation falls, or will central bank measures stifle economic growth too much around the world?

Even though corporate profits worldwide will moderate for the years 2022-2023 after last year's massive increase and the US economy, is slowing down slightly, a world recession is not yet likely. It is to be expected that the Western economy will regroup due to the global environment. Manufacturing data in many countries show that while new orders are slowing somewhat, the majority of companies continue to hire skilled personnel. Currently, production and employment continue to increase. This argues against a recession. Thus, at the moment, there is no sign of the economy slowing down too much and a reduction in inflation will be a positive signal for the markets.

What is currently priced into the markets?

The sharp drop of over 20% in the S&P, the worst start since 1970, has shocked the investment community. The bond market also failed to provide support and suffered a record loss as well: The US Aggregate Bond Index recorded a historic slump of over 10% in the same period (see Interest Rates section). The bond market has thus become competitive again and should be able to poach some of the risk capital. But as far as the equity markets are concerned: as long as interest rates do not decline, the markets have not yet fully priced in a significant drop in earnings. Thus, we believe it is likely that a recession is not yet priced in. Should this nevertheless occur, further equity market declines of up to another 15% are possible. However, if the economy turns out to be more robust and declines less than current forecasts, for example by quickly adjusting to the new environment, a sudden rebound may occur. Thus, the pricing of the markets suggests that a slow weakening of the economy is expected. European stocks have been punished more due to their geographic location with Russia and their economic links, and should deliver stronger results in the event of a rebound. In Europe, a slight recession in the stock markets should therefore already be taken into account.

Which equity strategy should be pursued at present?

Since the beginning of the year, the markets have punished growth stocks more than industrial and cyclical stocks. In contrast, the so-called "dividend aristocrats", i.e. the companies with the greatest track record of dividend growth, were able to hold up better in this poor environment, compensating for the weak performance in 2020 and 2021, which were dominated by technology and cyclical stocks, respectively. Currently, there is much to suggest that these defensive income-oriented stocks are still in focus until the end of the year. As far as the outlook for high-quality growth stocks in technology or other sectors is concerned, we have to wait for a discernible stabilisation of US interest rates. We expect that by 2023, investors will again take a liking to these stocks and accumulate shares in battered growth sectors that have fallen 20% or more without any significant decline in business activity. After all, less cyclical technology investments such as software and telecom services should see continued revenue growth and higher cash flows even in these times.

Our conclusion: Our model (CAIB) shows a slightly negative tendency of -0.04 with a range of -1 and +1 overall in the short term at this level. On a 12-month horizon, the CAIB shows a more positive opportunity profile of +0.10. On the one hand, the weaker economic forecasts for 2022 and 2023 cloud the picture negatively. On the other hand, these expectations have already been priced in, especially in the European equity markets. The average price-earnings estimates for 2023 of the leading European stock markets are significantly lower than those of the US and Asian stock markets. In the short term, we are focused on stocks with a higher dividend that can be maintained or increased in subsequent years, as well as stocks that correspond to the value strategy. With a 12-month view, we still advise buying the growth stocks of industry leaders that have been exposed to a sell-off this year. We advise investors who are already mainly invested in growth stocks to examine these holdings for their business model and competitive position in order to optimally position the portfolio for the price opportunities in 2023. Regionally, the European markets in particular offer a higher "surprise effect".

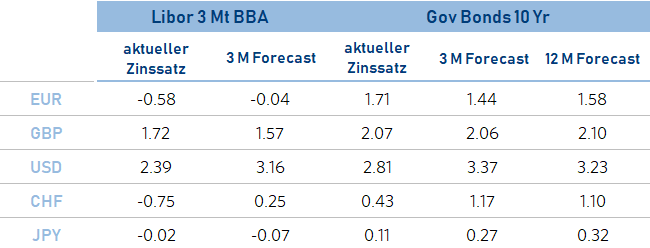

Interest

Bonds: Interest rates on a roller coaster?

Government bonds (neutral)

We are no longer as negative on government bonds as we were in our last investment committee and have upgraded them to Neutral. The US Federal Reserve has clearly accelerated its interest rate hikes and has also started the so-called "quantitative tightening" in June, a more restrictive monetary policy via a reduction of its central bank balance sheet, but also via bond sales. The European Central Bank (ECB) has also announced interest rate hikes. Inflation, the slowdown in economic growth, is already factored into valuations.

Our conclusion: The Fed still has room to raise rates. In Europe and Switzerland, growth is more affected by the conflict in Ukraine. Interest rates have already risen sharply since the beginning of the year. Global government bonds should generate similar returns to money market securities and we prefer a duration close to the benchmark level. We prefer government bonds from the core countries in Europe to those of the peripheral countries.

Investment grade bonds (neutral)

We expect a limited spread widening, which can be offset by positive interest income. Institutional investors are slowly starting to re-invest in this segment of their asset allocation.

Our conclusion: With a combination of higher interest rates and weaker economic and corporate earnings growth, we prefer IG bonds with short duration in USD and EUR. However, we remain neutral on this segment.

High-yield bonds (neutral)

We stick to our neutral assessment and prefer high-quality segments. The pressure on HY bonds may increase due to the overall situation. This is due to a decrease in demand for these securities, potentially a higher probability of default rates and more difficult financing conditions.

Our conclusion: Under the given conditions, we are neutral.

Emerging market bonds in hard currencies (cautiously attractive)

The current high yield of the JP Morgan Emerging Market Bond Index Global (7.7% yield to maturity), together with the still elevated spreads, offers an interesting yield advantage over US Treasuries to compensate for the risks. Many EM central banks have already raised their interest rates and the rise in US rates should slow down. Therefore, EM bond yields are expected to be able to withstand higher 10-year US yields. However, risks continue to be shaped by sentiment and capital flows.

Our conclusion: We prefer diversified exposure and have no regional preferences.

Mimi Haas, Lic. Rer.pol. HSG, M.A. in Banking and Finance HSG, Partner

Currencies

Currencies remain in the playing field of the geopolitical situation and central banks.

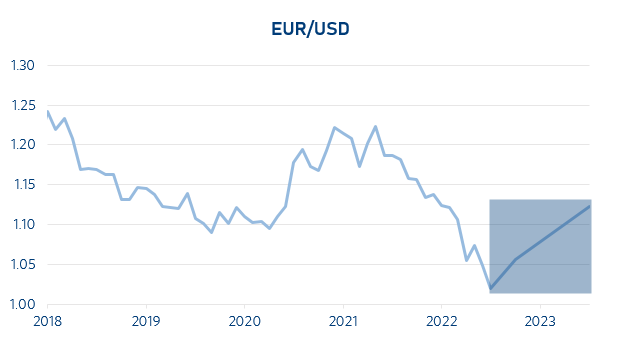

EUR / USD (current 1.04)

The Euro continues to fall against the greenback, which is considered a safe haven. The ECB remains one of the few major central banks to refrain from commenting on monetary policy steps. Poor sentiment in the financial markets, fears of recession and inflation continue to weigh on the EUR.

Our conclusion: The expected interest rate differential and the geopolitical situation continue to strengthen the US-dollar

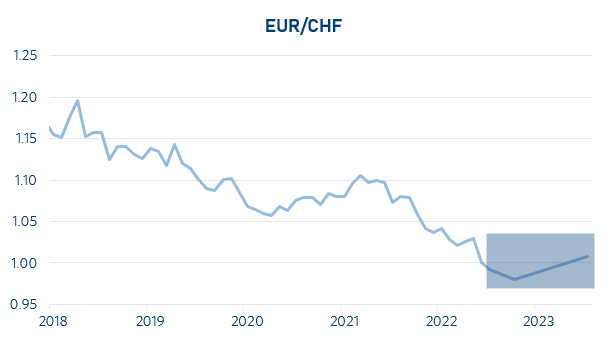

EUR/CHF(current 1.00)

The CHF remains high and has reached parity, although the SNB has started to intervene slightly over the last few weeks. EUR weakness and fears are pushing the CHF back up as a safe haven currency. In addition, the SNB's surprise decision to raise interest rates, with the prospect of continuing to do so, has influenced the CHF.

Our conclusion: The strength of the Swiss franc will continue in the current environment.

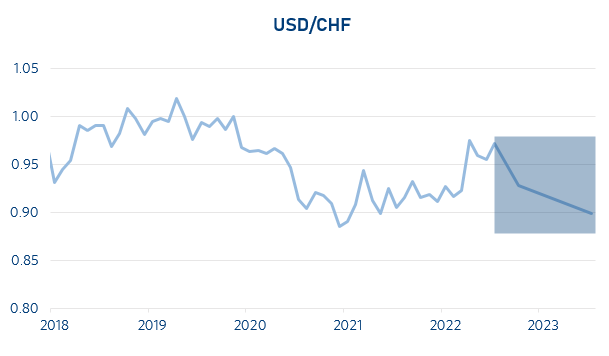

USD/CHF (current 0.96)

The USD has depreciated slightly against the CHF in recent weeks after the SNB surprisingly raised interest rates. The Swiss franc is considered a safe haven due to its financial system, the Dollar also has this function. In times of global economic and geopolitical uncertainty, however, investors tend to trust the CHF, hence this slight depreciation.

Our conclusion: We expect this to continue.

Mimi Haas, Lic. Rer.pol. HSG, M.A. in Banking and Finance HSG, Partner

Oil

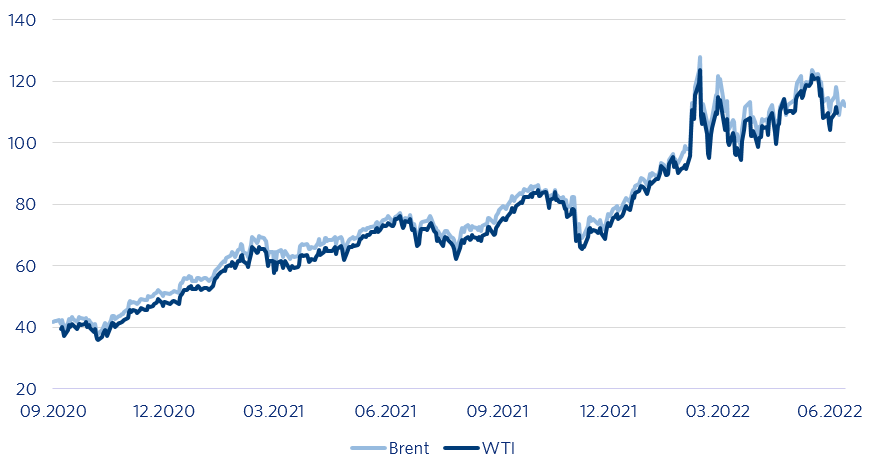

Russian oil finds new customers

At the virtual meeting of OPEC+ on 30.06.2022, it was decided to increase production in August by 648,000 barrels of oil per day as in July. This brings OPEC+ production closer to the pre-pandemic level. However, the problem at the moment is that the allocated production quotas cannot be exhausted by certain countries (OPEC was therefore still 850,000 barrels of oil per day below the announced quota at the end of April). Russian oil is currently finding more and more customers in Asian countries (e.g. China and India) at discounts of 25-30% to Brent.

Our conclusion: We expect the foreseeable decline in demand on the one hand and the announced increase in supply on the other to drive Brent and WTI oil prices down to around USD 80 per barrel in the course of the second half of 2022.

Precious Metals

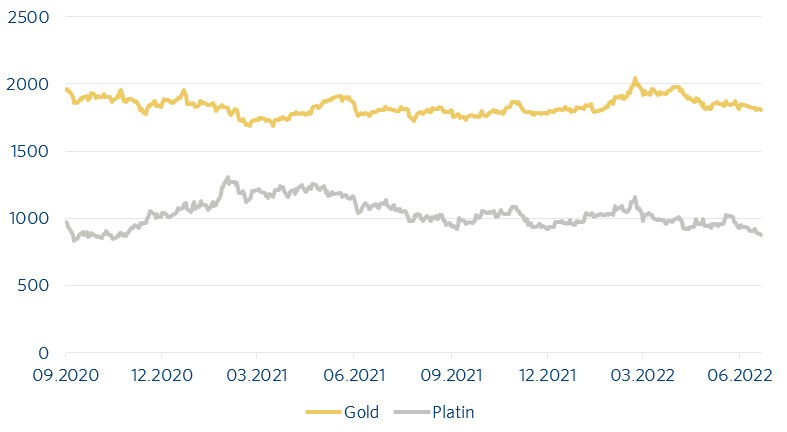

Gold in a headwind and platinum on the upswing?

Rising interest rates and a strong US dollar are competing with gold, whereas platinum is developing more positively thanks to lower overproduction and rising demand in the catalyst sector. Platinum is also increasingly being used as a substitute for expensive palladium in this market.

Andreas Betschart, Business Manager

Our conclusion: Gold faces competition from rising interest rates as a hedge against inflation and a firm dollar. Platinum, on the other hand, should strengthen over the coming months and depending on economic developments (supply chains).

Price range gold from USD 1,700 to 1,850 per ounce and platinum from USD 850 to 1,050 per ounce.

Abbreviations and explanations

bbl: 1 Barrell = 158,987294928 Litre

Bp: Basis points

GDP: Gross domestic products

BIZ: the Bank for International Settlements is an international financial organization. Membership is reserved for central banks or similar institutions.

EM-Bonds: Emerging market bonds. An emerging market is a country that is traditionally still counted as a developing country but no longer has its typical characteristics.

HY-Bonds: Fixed-income securities of poorer credit quality. They are rated BB+ or worse by the rating agencies.

IG-Bonds: Investment grade bonds are all bonds with a good to very good credit rating (Ra-ting). The investment grade range is defined as the rating classes AAA to BBB-.

IHS Markit: Listed data information services company

IWF: The International Monetary Fund (also known as the International Monetary Fund) is a legally, organiza-tionally, and financially independent specialized agency of the United Nations headquartered in the United States of America.

KOF: Business Cycle Research Centre at ETH Zurich

LIBOR: London Interbank Offered Rate is a reference interest rate determined in London on all banking days under certain conditions, which is used, among other things, as the basis for calculating the interest rate on loans.

OPEC: Organization of the Petroleum Exporting Countries

OPEC+: Cooperation with non-OPEC countries such as Russia, Kazakhstan, Mexico and Oman.

oz: the troy ounce is used for precious metals as a unit of measurement and is equal to 31.1034768 grams

Saron: The Swiss Average Rate Overnight is a reference interest rate for the Swiss franc

Seco: Swiss State Secretariat for Economic Affairs

Spread: Difference between two comparable economic variables

WTI: West Texas Intermediate. High-quality US crude oil grade with a low sulfur content.

Disclaimer:

The information and opinions have been produced by Chefinvest AG and are subject to change. The report is published for information purposes only and is neither an offer nor a solicitation to buy or sell any securities or a specific trading strategy in any jurisdiction. It has been prepared without regard to the objectives, financial situations or needs of any particular investor. Although the information is derived from sources that Chefinvest AG believes to be reliable, no representation is made that such information is accurate or complete. Chefinvest AG does not assume any liability for losses resulting from the use of this report. The prices and values of the investments described and the returns that may be received will fluctuate, rise or fall. Nothing in this report is legal, accounting or tax advice or a representation that any investment or strategy is appropriate to personal circumstances or a personal recommendation for specific investors. Foreign exchange rates and foreign currencies may adversely affect value, price or yield. Investments in emerging markets are speculative and involve considerably greater risk than investments in established markets. The risks are not necessarily limited to: Political and economic risks, as well as credit, currency and market risks. Chefinvest AG recommends investors to make an independent assessment of the specific financial risks as well as the legal, credit, tax and accounting consequences. Neither this document nor a copy of it may be sent in the United States and/or in Japan and they may not be handed over or shown to any American citizen. This document may not be reproduced in whole or in part without the permission of Chefinvest AG.