Click on the images to view our comments on each topic.

Switzerland

Challenges and opportunities in a global context

SECO is forecasting modest growth in Swiss GDP of 1.10% for 2024, which is slightly below the predicted rate of 1.20%. The economy grew moderately in the third quarter of 2023, driven in particular by the services sector. Global differences characterize the economy. While the US is experiencing strong growth, the eurozone, especially Germany, remains weak. This will affect the local export industry. Below-average growth is expected for Switzerland over the next two years. This is mainly due to the weak momentum in the eurozone. Investments could be weak due to falling capacity utilization and higher financing costs. Private consumption will have a supportive effect, although the unemployment rate will rise slightly to 2.30% this year compared to 2.00% in 2023.

Inflation fell surprisingly sharply from 3.40% in February 2023 to 1.40% in November 2023. In response, the Swiss National Bank (SNB) left the key interest rate at 1.75% and adjusted its inflation forecast downwards. The SNB expects an inflation rate of 1.90% for 2024 and 1.60% for the following year. Inflation thus remains within the SNB's target of between 0.00% and 2.00%.

SECO economic forecast

GDP 2024: 1.10%

Inflation 2024: 1.90%(E)

SNB key interest rate: 1.75%

Our conclusion:

Switzerland's political stability and neutrality contribute to its economic strength. In 2024, important topics could include digitalization, EU relations, global tax regulations and environmental protection. At company level, the Swiss franc is no longer expected to weigh as heavily on profits as it did last year. The successful implementation of artificial intelligence will make innovative companies even more productive. The Swiss equity market is attractively valued.

Sources: SECO, ZKB, IMF

As at: 15.01.2024

European Union

Slight brightening of the economic outlook

Growth of 1.40% is forecast for 2024 in the European Union (EU), while a decline of around 0.50% is expected in Germany, influenced by political uncertainties. Specific interest rate forecasts for the first quarter of 2024 are unclear, but interest rates could remain stable until the middle of the year and fall towards the end of 2024. The unemployment rate in the EU is estimated at 6.40% for 2024, with an increase expected in Germany due to economic contraction. The Purchasing Managers Index (PMI) remains an important indicator, with a value above 50 signaling a positive economic situation. Profit and sales expectations of European companies depend on economic development, with possible dampening effects in the event of a weak recovery or stagnation. The Purchasing Managers' Index rose slightly to 44.4 points in December 2023. Political decisions, especially in energy policy and financial support measures, are having a significant impact on the European economy, particularly through the rise in energy prices and the resulting economic burdens.

Inflation in Europe is slightly rising on the rise again. In December, consumer prices rose by 2.90% compared to the previous month. In November, inflation was 2.40%. This is the first time that inflation has increased again after seven months of declines. However, core inflation, which excludes the volatile energy and food prices as well as alcohol and tobacco, fell to 3.40% in December after 3.60% in November. The European Central Bank's (ECB) medium-term target of a general inflation rate of 2.00% is receding somewhat into the distance again with the new data.

In December, the final seasonally adjusted HCOB Composite PMI was below the growth threshold of 50 points for the 7th month in a row and, at an unchanged 47.6 points, signaled that eurozone economic output had contracted moderately once again. In the third and fourth quarters of 2023, the index remained consistently below the 50-point mark. Business activity, incoming orders and employment continued to decline, but the outlook is brightening. The business outlook within a year continued to recover from its recent September low and climbed to a 7-month high.

GDP growth 2024 +1.40% (E)

EU inflation 2024 +2.90% (E)

Current 3-month Euribor +3.93%

Our conclusion:

Leading indicators point to continued weak economic momentum in the eurozone in the first quarter of 2024, although industrial sentiment has remained stable. The economy is expected to stagnate in the first half of the year, followed by a recovery. Industry and private consumption are expected to provide slight growth impetus, supported by expected real wage growth and a robust labour market. The European Central Bank (ECB) has kept interest rates stable for the time being, but is probably planning interest rate cuts due to lower inflation and a weak economy. These could begin in June and September, followed by more in 2024. Despite the challenges, a positive trend on the European equity market is expected in Q2 due to an improved economic outlook and below-average valuations.

Daniel Beck, Member of the Executive Board

Sources: European Commission, Statista, HCOB, S&P Global

As at: 15.01.2024

United Kingdom

USA

Dead cat rebound?

The GDPNow model of the Federal Reserve Bank of Atlanta forecasts growth in the US economy in Q4 2023 at 2.20% (in Q3 it was still at 4.90%). According to the last FOMC meeting on December 13, GDP growth is expected to flatten further to 1.40% in 2024.

The US Composite PMI in December improved slightly by 0.20% to 50.9 points compared to the previous month, indicating a continued expansion of the US economy in 6 months. The service sector was responsible for the increase with 51.40 points (November 50.8), while the manufacturing sector weakened with 47.9 (November 49.4).

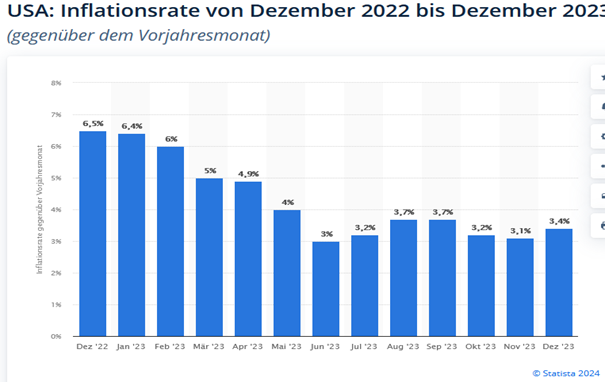

Inflation rose by 0.30% to 3.40% in December compared to the previous month (3.20% was expected). Encouragingly, however, the Fed's much-watched core inflation rate (excluding energy and food) fell by 0.10% on the previous month to a 2.5-year low of 3.90% (3.80% was expected).

The Fed left the Fed Fund Rate unchanged at 5.25 - 5.50% at its December meeting. What was new, however, was the statement by its chairman Jerome Powell that the interest rate level does not need to be raised further due to the successes in the fight against inflation.

Despite the rebound in the inflation rate in December, the market now assumes an 80.00% probability that the Fed will cut interest rates by 0.25% for the first time as early as March (the Fed in July 2024). Even the rather strong labor market report in December with 216,000 new non-farm jobs created and the still low unemployment rate of 3.70% (unchanged from the previous month) did nothing to change this.

The companies represented in the S&P 500 Index are expected to report earnings growth of 1.60% in the fourth quarter of 2023. Once again, the actual earnings figures are expected to be higher due to the downward revision of earnings estimates in advance. Based on the earnings estimates for the next 12 months, the S&P 500 Index has a price/earnings ratio of 19.5. The 5-year average is 18.9 and the 10-year average is 17.6

GDP2024 (IMF): +1.48% (E)

Inflation 2024 (IMF): +2.76% (E)

Fed Fund Rate: +5.50%

Our conclusion:

The US economy will cool down in 2024, but will remain on course for growth. Inflation will continue to weaken towards the Fed's target. The resulting interest rate cuts will have a positive impact on corporate earnings and provide a tailwind for equities.

Dr. Patrick Huser, CEO

Sources: Trading Economics, US Bureau of Labor Statistics, Statista, FuW, IMF World Economic Outlook October2023, FactSet, FMOC

As at: 15.01.2024

China

Class not mass

China faces another challenging year as the real estate market continues to look bleak despite a more than two-year slowdown. While the government has taken measures to support real estate developers and boost demand, potential buyers remain hesitant for fear that the apartments they have already paid for will not be completed. This is leading to a continued decline in property sales and putting pressure on developers. A quick solution to this dilemma is not in sight. Consumer sentiment currently gives little cause for euphoria and growth is mainly being driven by fiscal stimuli in the form of infrastructure investment. At the same time, the central bank is ensuring sufficient liquidity. In order to counteract the slowdown in growth, a further reduction in key interest rates will probably be necessary in the second half of the year. Growth of only 5.00% is therefore expected for the coming year, which is the lowest figure since official measurements began, apart from the pandemic years.

In view of the weak economic momentum, price pressure will also be low in 2024. However, fears of deflation are exaggerated. According to the IMF, inflation will therefore only average 0.70%.

IMF Economic Forecast

GDP 2024: 5.00%

Inflation 2024: 1.70%

3 months Shibor: 2.53%

Our conclusion:

The government's top priority is to build a modern industrial system with scientific and technological innovation and increase domestic demand. The high-tech industry is to be expanded and old growth pillars such as speculative house building are to be replaced. The expansion of government spending is taking place very cautiously. Due to the major political risks and the anaemic economic momentum, equity investments in China are not recommended.

Sources: Allianz, ZKB, IMF

As at: 15.01.2024

Japan

Asia's driving force

Japan expects moderate economic growth in 2024 due to the slow recovery after the COVID-19 pandemic and low inflationary pressure. Core inflation was around 3.00% in 2023, and thus only just above the target value of 2.00%. The unemployment rate is low and wage increases could support growth. Interest rates remain unchanged for the time being as the Bank of Japan is sticking to its loose monetary policy. According to SSGA Economists, average inflation in Japan is expected to fall to 2.60% in 2024. This should allow the Bank of Japan to remain relatively cautious compared to other central banks.

Big companies are forecasting growth, supported by corporate reforms, a good capital situation and positive stock market performance. Capital expenditure is expected to rise, as is private consumer spending, while exports are growing and consumption by foreign tourists is recovering moderately. The Japanese government is planning economic measures such as tax cuts and support for households in order to increase consumption. Prime Minister Kishida is calling on companies to consider wage increases over and above price rises.

This economic environment is showing positive signs of recovery and growth, despite some of the challenges Japan is facing. However, these are more likely to be found outside Japan.

IMF Economic Forecast

GDP 2024: 1.00%

Inflation 2024: 2.90%

3 months (JPY Libor): -0.03%

Our conclusion:

Japanese equities are still trading below book value and remain underweighted in international portfolios. However, the stock market has already caught up in 2023. This raises the question of whether it is the right time to enter the market, despite the positive starting position.

Mimi Haas, Lic. rer.pol. HSG, M.A. in Banking and Finance HSG, Partner

Sources: IMF, FT, SSGA Economist and AI

As of: 15.01.2024

Emerging Markets

Growth momentum despite interest rate restrictions

Although interest rates are extremely restrictive, growth prospects in the emerging markets have developed surprisingly well in 2023 and have even accelerated again recently. In the third quarter, growth rates were still below potential in many places, but the acceleration was broad-based. Economic activity in emerging economies is expected to gain further momentum in 2024, primarily as a result of monetary easing. The fall in inflation in the first half of the year gives central banks scope to cut interest rates, particularly in Asian economies. In countries that have already cut interest rates, monetary easing is likely to increase, particularly in Latin America and Eastern Europe. The cycle of interest rate cuts will become broader, peaking in the middle of the year and lasting for several quarters due to the high level of interest rates. Although some countries are still struggling with high inflation, a disinflationary trend is expected. This is likely to lead to higher real wages and a revival in consumption. In addition, important elections are imminent in several countries, making fiscal policy stimuli likely in advance and thus supporting the economy. Growth is increasingly shifting to emerging markets outside of China. Favorable demographic trends, supply chain diversification and global economic rebalancing are attracting investment in infrastructure in countries such as India, Vietnam and Indonesia.

Our conclusion:

Supported by monetary policy measures, expected disinflationary trends and upcoming fiscal stimulus, emerging markets are well positioned for continued growth. Equity valuations in Brazil, Mexico and India appear attractive.

Dino Marcesini, Partner

Sources: ZKB, IMF

As at: 15.01.2024

Stocks

Japan and Switzerland celebrate while Europe and the UK mess up the global economic dance?

In 2023, the US equity markets, especially the S&P 500, experienced a strong recovery with a 24.00% rise, driven by AI-based technology companies. In 2024, profitable growth stocks of small and medium-sized companies with solid balance sheets are expected to gain in popularity. Although growth could slow at the beginning of 2024, no synchronized collapse of the global economy is expected. Sustained economic momentum and an improvement in corporate earnings are expected in the second half of the year, pointing to stronger global economic growth in 2025.

The European economy is showing a cautious recovery, with expected GDP growth of 1.40% in 2024 and an acceleration to 2.10% in 2025. The UK is expected to see growth of 0.60% in 2024 and 2.00% in 2025, supported by easing credit standards and falling government bond yields. Both European equities excluding the UK and UK equities are seen as relatively inexpensiv and could remain so.

However, some EU companies could face challenges due to the slowdown in global economic activity and rising costs. Nevertheless, the earnings outlook for European companies is positive overall. Experts' estimates for earnings per share growth in Europe excluding the UK are around 8.00% in 2024. However, these estimates are a little too optimistic for our taste.

In Asia, different countries have seen different developments. Japan and India benefited from diversified supply chains and posted positive returns, while Hong Kong and China faced economic challenges. Taiwan, on the other hand, surprised with high returns. China remains an uncertainty factor due to a real estate crisis and structural challenges. Macroeconomic challenges in Asia are expected to ease in 2024, especially if US monetary policy is loosened, which could lead to more moderate US interest rates and a more stable US Dollar.

Our conclusion:

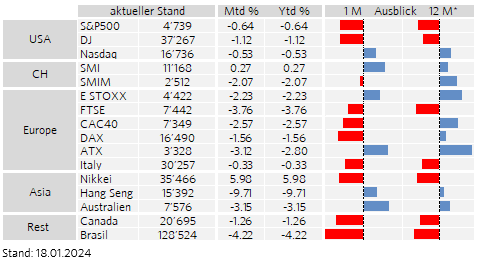

The year 2024 will bring diverse developments on the global stock markets. The Japanese Nikkei and the Swiss SMI record good starting gains of 7.20% and 0.90% respectively. In contrast, Europe and the UK start the year with losses, indicating a mixed situation on the markets.

Our internal assessments, based on our CAIB scoring model, show that the global equity markets present a slightly negative picture in the short term, but with a positive outlook in certain areas. Swiss equities, the US Nasdaq and the STOXX 50 are rated positively. The recovery in the healthcare sector at the start of 2024 is particularly striking. After challenges in the previous year, the sector is experiencing a revival, mainly due to mergers and acquisitions. This points to a broader recovery in the healthcare sector, with earlier concerns diminishing and more positive trends becoming visible.

Interestingly, Japanese equities are still trading below book value and are underweighted in international portfolios, however, we are cautious and do not believe the current timing is ideal to enter as equity markets have already seen significant gains in 2023 and 2024.

Rico Albericci, CEFA

Sources: S&P, Citigroup, MarketMap, IMF, and Chefinvest

As of: 15.01.2024

Interest

Back to normality

In 2023, the decline in inflation made progress and continued in the direction of the core inflation target of the individual central banks, albeit faster in the USA than in Europe. This should continue in 2024 if geopolitical tensions do not escalate.

As a result, the combination of weaker growth and lower inflation may cause interest rates to fall in 2024. However, caution is required here, the question is whether the market's optimistic view that this is more likely to happen in the first half of 2024 will prove to be correct.

Our conclusion: Overall, bonds appear attractive in 2024 due to their yield and the economic environment, although the risk varies depending on the bond type.

Government bonds

We expect yields on this bond class to fall. Weaker growth is likely to contribute to lower interest rate expectations. Nevertheless, this bond class will continue to benefit from safe-haven buying if the outlook becomes more volatile in the world.

Investment grade bonds (IG)

Due to attractive yield premiums on quality bonds and an improvement in creditworthiness, an overweighting of this asset class in the medium duration range is recommended.

High yield bonds (HY)

The current yields of 7.00% offer a good buffer against defaults. A possible widening of spreads in 2024 could result in attractive entry points. High-yield bonds with higher BB ratings are better equipped for a possible economic downturn due to lower debt. However, we recommend this asset class more to investors who can bear the risk and should be allocated to an ETF.

Emerging markets bonds (EM)

Emerging market bonds in local currency offer a high yield of about 9.00% and are relatively safe from currency losses and credit defaults, especially if US yields are forecast to fall. However, we only recommend this asset class to investors who can bear the risk and as an investment in an ETF.

Our conclusion: Overall, bonds appear attractive in 2024 due to their yield and the economic environment, although the risk varies depending on the type of bond.

Mimi Haas, Lic. rer. pol. HSG, M.A. in Banking and Finance HSG, Partner

Sources: F&W, JP Morgan and Bloomberg

As of: 15.01.2024

Currencies

What will the world look like after the big inflation shock?

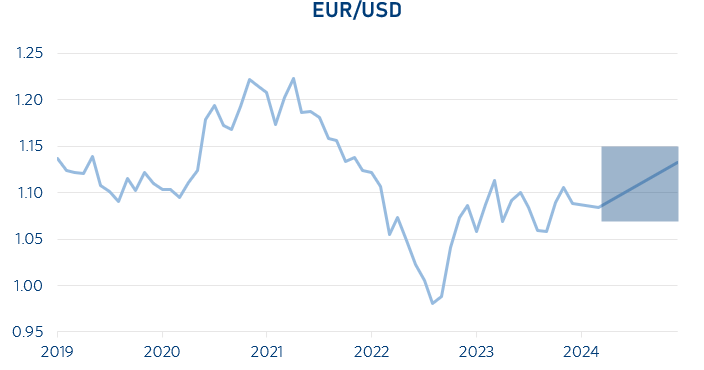

EUR/USD (17.01.2024: 1.09)

It can be assumed that some central banks will be able to cut their key interest rates in 2024, as the market currently expects the Fed and the ECB to do. Especially where central banks have massively raised their interest rates in recent years and especially where recession is looming, central banks will use the success of the fight against massive inflation from 2021 to 2023 to cut interest rates again. The market view that the Fed will start to cut is therefore quite realistic in our view. The reasons for this are: That is where a recession is likely in the course of 2024, that is where the decline in inflation begins, and that is where the Fed's interest rate policy is typically hyperactive, with more massive rate hikes in inflationary periods, but also with stronger rate cuts when it seems appropriate. The only question is when.

For the ECB, on the other hand, we expect significantly less scope for interest rate cuts than the market is currently pricing in.

Our conclusion: The currency pair will therefore remain volatile, as in 2023, and will develop depending on the central banks and their actions. Until this happens, we see a slight sideways movement.

EUR/CHF (17.01.2024: 0.94)

The Swiss Franc is likely to remain strong in 2024, influenced by geopolitical and economic developments. Short-term corrections are possible, but the franc is likely to maintain its strength and continue its "safe haven" function. The franc began to appreciate in the final weeks of 2023, driven by the central bank's measures. The SNB will certainly reconsider its monetary policy, as this has far-reaching consequences for the Swiss economy.

Our conclusion: We forecast that the Swiss Franc will weaken slightly against the euro in the short term, but strengthen again over the course of the year.

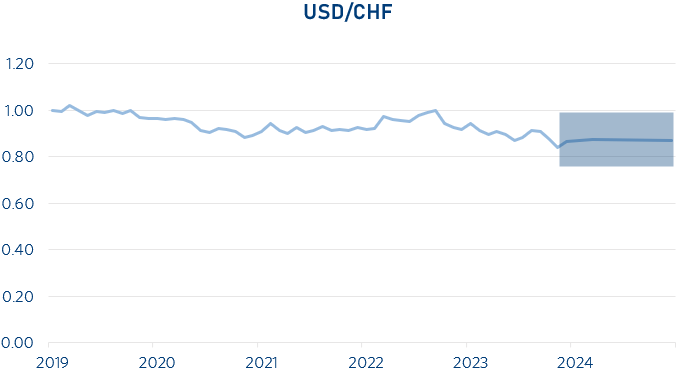

USD/CHF (17.01.2024: 0.86)

A further strengthening of the Swiss franc against the US dollar is possible, although uncertainties remain. The positive interest rate differential between the US Dollar and the Swiss Franc could continue to boost the exchange rate.

Our conclusion: We expect the currency pair to trend sideways until it becomes clearer how the central banks will shape their interest rate policy.

Mimi Haas, Lic. rer.pol. HSG, M.A. in Banking and Finance HSG, Partner

Sources: F&W, Market Map and Bloomberg

As of: 17.01.2024

.png)

Oil

Equilibrium restored?

The WTI oil price has moved in a rather narrow range between USD 70 and USD 80 per barrel in recent weeks. Doubts about continued production cuts by OPEC+ as well as higher US inventories have outweighed fears of a supply shortage due to the ongoing geopolitical tensions in the Middle East.

In the long term, a potential decline in demand for fossil fuels is expected, which could lead to lower oil prices in 10 years' time. However, the IEA is still forecasting an average Brent oil price of $73 per barrel in 2030 (currently at USD 78 per barrel).

Our conclusion: We expect WTI oil to move in a range between USD 70 and USD 80 per barrel.

Dr. Patrick Huser, CEO

Sources: F&W, MarketMap,International Energy Agency (IEA)

as at: 15.01.2024

Precious Metals

Gold and platinum as diversification anchors

In the last three months, the price of gold rose from around EUR 58.03 per gram (EUR 1,805.00 per ounce) on November 14, 2023 to around EUR 60.09 per gram (EUR 1,869.01 per ounce) on January 12, 2024. The current price of 999 gold is EUR 60.16 per gram, and an ounce of gold costs around EUR 1,871.08.

The forecasts for 2024 vary: some experts expect the price of gold to rise to up to USD 2,200 per ounce. These predictions are influenced by geopolitical events such as the ongoing war in Ukraine, the political situation in China and Taiwan, the energy crisis in Europe and the US presidential election in 2024. Other forecasts see the price of gold ranging between USD 2,000 and USD 2,100 per ounce, with some analysts even predicting a peak of almost USD 2,500 per ounce by the end of 2024. These forecasts take into account macroeconomic factors and the global economic situation.

Information on the price development of platinum is currently not available

Our conclusion: Neutral

The continuing turbulent global political situation is keeping gold at a high level, currently at USD 2,040 per ounce; platinum is also holding up well at USD 916 per ounce. In the event of prolonged crises, both precious metals should remain in portfolios.

Andreas Betschart, Business Manager

Sources: UBS

As at: 15.01.2024

Abbreviations and explanations

bbl: 1 Barrell = 158,987294928 Litre

Bp: Basis points

GDP: Gross domestic products

BIZ: the Bank for International Settlements is an international financial organization. Membership is reserved for central banks or similar institutions.

EM-Bonds: Emerging market bonds. An emerging market is a country that is traditionally still counted as a developing country but no longer has its typical characteristics.

HY-Bonds: Fixed-income securities of poorer credit quality. They are rated BB+ or worse by the rating agencies.

IG-Bonds: Investment grade bonds are all bonds with a good to very good credit rating (Ra-ting). The investment grade range is defined as the rating classes AAA to BBB-.

IHS Markit: Listed data information services company

IWF: The International Monetary Fund (also known as the International Monetary Fund) is a legally, organiza-tionally, and financially independent specialized agency of the United Nations headquartered in the United States of America.

KOF: Business Cycle Research Centre at ETH Zurich

LIBOR: London Interbank Offered Rate is a reference interest rate determined in London on all banking days under certain conditions, which is used, among other things, as the basis for calculating the interest rate on loans.

OPEC: Organization of the Petroleum Exporting Countries

OPEC+: Cooperation with non-OPEC countries such as Russia, Kazakhstan, Mexico and Oman.

oz: the troy ounce is used for precious metals as a unit of measurement and is equal to 31.1034768 grams

Saron: The Swiss Average Rate Overnight is a reference interest rate for the Swiss franc

Seco: Swiss State Secretariat for Economic Affairs

Spread: Difference between two comparable economic variables

WTI: West Texas Intermediate. High-quality US crude oil grade with a low sulfur content.

Disclaimer:

The information and opinions have been produced by Chefinvest AG and are subject to change. The report is published for information purposes only and is neither an offer nor a solicitation to buy or sell any securities or a specific trading strategy in any jurisdiction. It has been prepared without regard to the objectives, financial situations or needs of any particular investor. Although the information is derived from sources that Chefinvest AG believes to be reliable, no representation is made that such information is accurate or complete. Chefinvest AG does not assume any liability for losses resulting from the use of this report. The prices and values of the investments described and the returns that may be received will fluctuate, rise or fall. Nothing in this report is legal, accounting or tax advice or a representation that any investment or strategy is appropriate to personal circumstances or a personal recommendation for specific investors. Foreign exchange rates and foreign currencies may adversely affect value, price or yield. Investments in emerging markets are speculative and involve considerably greater risk than investments in established markets. The risks are not necessarily limited to: Political and economic risks, as well as credit, currency and market risks. Chefinvest AG recommends investors to make an independent assessment of the specific financial risks as well as the legal, credit, tax and accounting consequences. Neither this document nor a copy of it may be sent in the United States and/or in Japan and they may not be handed over or shown to any American citizen. This document may not be reproduced in whole or in part without the permission of Chefinvest AG.