Click on the images to view our comments on each topic.

Switzerland

Robust

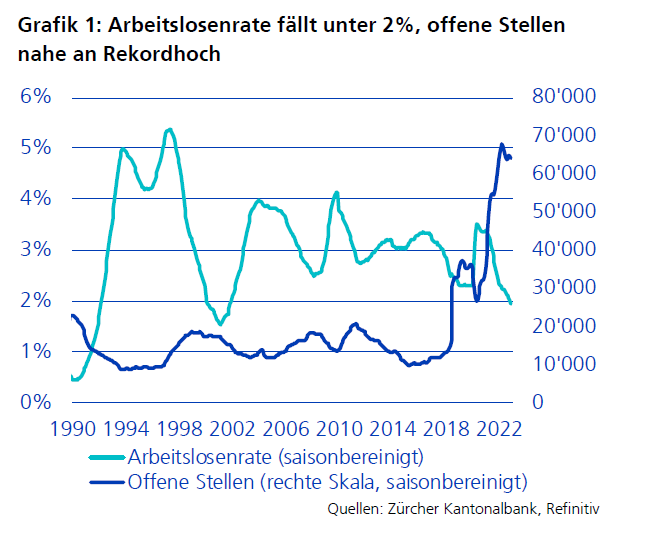

The Swiss labour market continues to be extremely robust. In January, the seasonally adjusted unemployment rate remained at 1.90%, at its lowest level in more than 20 years. However, due to the economic uncertainties in the domestic market and abroad, SECO experts see unemployment figures to rise slightly in the coming months. On a seasonally adjusted basis, the unemployment rate for 2023 as a whole should increase to 2.30%. Still low enough to support consumer spending. Meanwhile inflation rose more than expected in January from 2.80% to 3.30%, to its highest level in four months. The main driver of this higher annual rate was government-administered electricity prices rise by 25.00% at the beginning of the year. Core inflation, excluding energy and fuel, increased from 2.00% to 2.20%. In March, the SNB is expected to raise key interest rates by a further 0.50% to 1.50%. Finally, companies have been able to report encouraging year-end figures in recent weeks. And for 2023, the majority of CEOs also expect moderately growing sales and earnings.

SECO economic forecast

GDP 2023: +1.00% (E)

Inflation 2023: +2.20% (E)

SNB interest rate: +1.00%

Our Conclusion: Positive

Supported by stable consumer spending and a further increase in exports, the Swiss economy is set to perform positively. The SECO expert group reaffirms its previous estimates. For 2023, it is forecasting growth of 1.00% in the Swiss economy, followed by 1.60% in 2024. Swiss equities are trading slightly below their historical average price and offer long-term potential.

Dino Marcesini, Partner

Source: OECD and SECO

European Union

Economic growth surprises positively - no recession

Real GDP growth in the European Union (EU) surprised positively in Q4 2022 with a slight increase of 0.10%, although the erosion of purchasing power due to record high inflation has left clear marks. Last summer, the economy had still grown by 0.30%. Nevertheless, the EU economy performed a lot better than predicted and avoided the expected downturn. The annual GDP growth rate for 2022 was 3.50% in both the EU and the Eurozone.

The EU labour market continues to perform well, with the unemployment rate at an all-time low of 6.10% in the EU and 6.60% in the Euro area at the end of 2022. The strongest labour market in the EU for decades, it will continue to remain stable in the future. Since its peak of 7.80% in July 2020, the unemployment rate in the European Union has steadily declined.

The headline inflation rate has fallen for the third year in a row and inflation has peaked. In January 2023, the Eurozone inflation rate fell to 8.50% from 9.20% in December due to a fall in energy prices. Its all-time high had been reached in October at 10.60%.

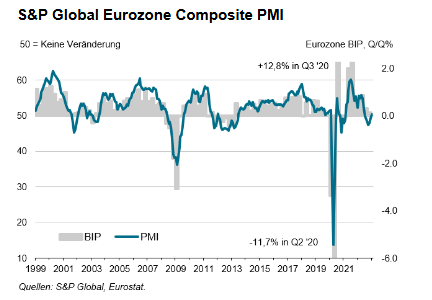

The Eurozone's economic output recorded a mini-growth in January for the first time since a six-month decline. Standing at 50.3 points, the S&P Global Flash Eurozone Composite PMI was above the neutral 50.0 mark in January, indicating growth for the first time since June 2022, a minimal positive sign.

EU Inflation 2023: +6.40% (E)

Current 3 month Libor: +2.66%

GDP growth 2023: +0.80% (E)

Our Conclusion: Positive

The European economy has noticeably stabilised in the last few months. The diversification of energy supply, the rapid build-up of energy reserves and the mild winter have ensured a secure energy supply and a significant decline of the previously high energy prices. Supply bottlenecks are also dissolving. All this is relieving the pressure on both businesses and consumers. Surveys in January point at this and leave us confident that the feared economic downturn will not occur in the first quarter of 2023. However, economic activity will remain weak for the time being.

In its winter forecast for 2023, the European Commission projects growth of 0.80% in the EU and 0.90% in the Eurozone, down from 0.50% and 0.60% for the Autumn forecast. The EU economy is likely to avoid recession, but headwinds and uncertainties will persist. Growth expectations for 2024 remain unchanged at 1.60% in the EU and 1.50% in the Euro area.

ECB President Lagarde said the ECB will stick to its course of raising the key interest rate and, due to underlying inflationary pressures, will raise rates by a further 50 basis points in March at its next meeting. After that, the ECB will assess the further course of monetary policy. This rate hike will then lift the key interest rate to 3.50%. Inflation in the Eurozone has fallen steadily over the last three months, but still remained at 8.50% in January. Thus, the inflation target of 2.00% appears to be far away. Core inflation recently remained at 5.20%, which is of particular concern to the Euro guardians. Fortunately, the European Commission has slightly lowered its expectations in comparison to the previous autumn, mainly as a result of developments on the energy market. It expects inflation to fall to 6.40% in the EU in 2023 and to 2.80% in 2024, while in the Eurozone it is projected to fall to 5.60% and 2.50%. Amid this environment, there are signs that interest rate hikes may come to an end in the course of this year.

Daniel Beck, Member of the Executive Board

Source: European Commission, Statista and S&P Global

United Kingdom

USA

‘No landing’?

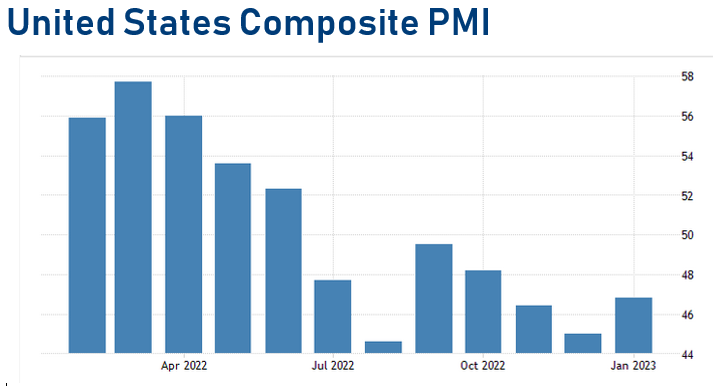

According to Markit Economics, the S&P Global US Composite PMI rose to 46.8 points in January, up 1.8 points from December. This improvement is mainly due to the services sector, which rose from 44.7 to 46.8 points in January compared to December. However, the manufacturing sector also rose in this period from 46.2 to 46.9 points. The 3 to 6 months ahead index thus indicates stagnating but not contracting economic activity despite the sharp interest rate hikes (only a value of 43 and below indicates a recession). At the end of January, the US Bureau of Economic Analysis reported its first estimate of US gross domestic product (GDP) for the last quarter of 2022, an annualised rate of +2.90%. For the whole year 2022, GDP was +2.10% (2021 +5.90%). The IMF recently even expects further economic growth of +1.40% for 2023 (slightly higher than their October 2022 forecast).

The inflation rate in the USA rose to 6.40% in January (December 6.50%). However, a decline to 6.20% was expected. The core rate also declined in this period from 5.70% to 5.60% (a decline to 5.50% was expected). The main drivers were housing and energy costs, while wage pressures, despite the record low unemployment of a seasonally adjusted 3.40% in January, were surprisingly low. The Survey of Professional Forecasters (SPF, February 2023) expect now the unemployment rate to rise only to 4.10% by end of 2023.

After a more optimistic view on the Fed Fund Rate peak than the one of the Fed had prevailed in the market in the course of January, markets started to converge again with Fed expectations with a peak rate of 5.25% after the release of the January inflation figures on 14 February.

More than 80.00% of the S&P 500 companies have already published their financial figures for the 4th quarter of 2022. Out of these, 68.00% of companies have exceeded earnings expectations and 65.00% have beaten revenue expectations. The price/earnings ratio of the S&P 500 based on expected 2023 corporate earnings is 18, slightly below the 5-year average of 18.5 and above the 10-year average of 17.2.

Fed Fund Rate: +4.75%

GDP 2023 (IMF): +1.40% (E)

Inflation 2023 (SPF): +6.40% (E)

Our Conclusion:

Inflation will continue to decline. However, it may take a little longer before the inflation target of 2.00% is reached. Due to the resilience of the economy, it now looks as if there will be even no (soft) landing - mild recession - of the US economy. This will continue to provide a tailwind for corporate profits and thus for the markets in the medium term, even if higher interest rates will still provide a headwind in the short term.

Dr. Patrick Huser, CEO

Source: Statista, Survey of Professional Forecasters and FactSet

China

From Zero Covid to Covid for All

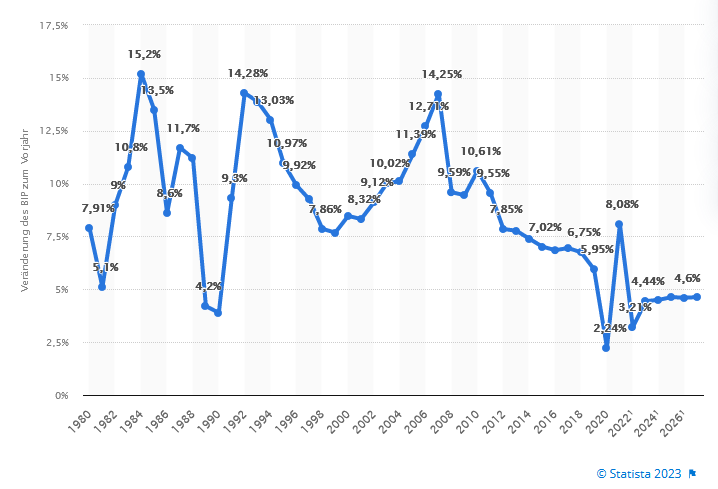

The abrupt turnaround in the handling of the coronavirus initially weighed on the Chinese economy in December. The high sickness rate led companies to cut production and consumers to be somewhat cautious, but the losses were much lower than expected. Overall, GDP grew by 3.00% last year. The economic low point has meanwhile been passed. As the recovery rate rises, absenteeism from work and fears of infection are reduced. The catch-up potential in the contact services sector is high and consumer sentiment is starting to recover, with Chinese consumers also having considerable savings.

IMF economic forecast

GDP 2023: +5.20% (E)

Inflation 2023: +2.20% (E)

3 months Shibor: +2.42%

Our Conclusion:

China's structural problems are still there. The real estate market is only tentatively bottoming out. The provinces have built up high debts in recent years. The protectionist attitude of the industrialised countries towards China could slow down exports. Economic growth for 2023 is estimated at 5.20%, which is remarkable. Due to the complex risk factors, we do not recommend direct investments in China, but rather investments in European companies that benefit from the opening of China.

Source: IMF and LLB

Japan

Recent developments in Asia positive for Japan and its companies

Japan and its economy are in a different cycle than Western countries. There have been a number of challenges in recent years, which are now gradually subsiding and may even provide an upswing.

The head of Japan's central bank, Kuroda, has pursued a completely different monetary policy over the past year than has been common in the rest of the world. As a result, inflation is not an issue in Japan and the Yen is low against the major Western currencies. The massive hike in interest rates in Europe and especially the US is hitting companies with high levels of debt. However, thanks to their overcapitalised balance sheets, Japanese companies are mostly unaffected. And Japan is a leader in many structural growth areas, e.g. digitalisation, semiconductors and gaming.

The end of the "covid-zero" policy in Asia is particularly supportive of Japan. The economy, coupled with moderate inflation, is expected to outperform. Tourism has already picked up strongly, the opening of the borders to foreign visitors was not before October 2022, and there is a huge catch-up effect.

GDP 2023: +1.60% (E)

Inflation 2023: +1.40% (E)

3 months Tona rate: -0.01%

Our Conclusion:

Japan is still undervalued and underrepresented in international portfolios. The market offers a good opportunity for medium-term investors.

Mimi Haas, Lic. Rer.pol. HSG, M.A. in Banking and Finance HSG, Partner

Sources: F&W, Reuters and Bloomberg

Emerging Markets

Handbrake applied in Latin America

Outside of Asia, Brazil is one of the most important economies among the Emerging Markets. Recently, the Brazilian economy has lost momentum. The economic slowdown is slowly becoming reflected in the labour market. The unemployment rate rose slightly for the first time in December. Political uncertainty has increased since the new government has taken over. The extension of social programmes will increase the debt. In addition, President Luiz Inacio Lula da Silva has called into question the independence of the central bank. Even though inflation is not yet under control, interest rate cuts are envisaged in the course of the year. Overall, the economic outlook for 2023 is lower for Brazil than for emerging Asia. GDP growth in Latin America is expected to be 2.00%, while GDP growth in Asia is forecast at over 5.00%.

Our Conclusion: Negative

The momentum in this emerging market segment is much higher in Asia than in Latin America or Eastern Europe. In economically and politically uncertain times, we do not recommend new equity investments in emerging markets.

Dino Marcesini, Partner

Source: IMF and LLB

Stocks

In Europe, the glass is half full!

If one looks at a plethora of objective data, the world economy today can be seen as the famous half-full or half-empty glass. The often contradictory and confusing data leads investors to believe that they have made it through the worst of the bear market. Still, with an eye on global challenges, they are on guard and reluctant to invest in equities. Nevertheless, global equity and credit markets - in particular those investments with higher credit or price risk - rallied significantly in January. However, they did not provide relief for investors. Under the leadership of the Fed, many central banks continue to tighten interest rates to combat inflation. This controlled slowdown of the economy is likely to be prolonged somewhat by the surprisingly good economic data, continuing strong employment and only marginally lower consumer spending, even in the USA in (Consumer Confidence Index - CCI). Another positive aspect is that inflationary pressure is slowly decreasing and having a stabilising effect globally. This also led to the fact that Europe has recovered from its energy supply panic and as a result energy prices have fallen significantly.

On the other hand, the slowdown in manufacturing, housing, imports and goods shipments is particularly striking and points to a different, less rosy direction. Fitting into the same picture, corporate profits were slightly weaker and some companies have reduced their own expectations for this year. The consensus of analysts' estimates also suggests that the recession is already over, which the bears interpret as a sign that share prices are too high. For they expect growth to weaken significantly or central banks to remain restrictive until the labour market eases again.

Our Conclusion: Positive

We have a view of the glass half full and remain positive particularly for European equities!

On this basis, we are positive for the European stock markets over the next 12 months. Based on our valuation tool (CAIB), we estimate the economy in Europe to be more stable. The negative effect of the central banks' restrictive monetary policy is being offset by the massive politically motivated spending worldwide on infrastructure, defence and humanitarian equipment. Mainly the continental European stock exchanges have a significantly lower valuation than the US stock exchanges. Hence, chances of profit are higher. We believe that equities of "peripheral" stock exchanges such as Italy or Austria in particular are favourably valued. But Swiss equities are also attractive despite the current PE valuation and could surprise this year. Moreover, we expect shares of companies that belong to one of the following trends may outperform: Silver Society, Global Diversity, Security and Innovative Health.

Sources: S&P, Citigroup, MarketMap, IMF and Chefinvest

Interest

Hope in the bond market!

The fixed coupon payments of the bonds were mostly lower than the price losses of the corresponding bond last year. Investors had to accept losses and cope with strong fluctuations. But especially in the last months of 2022 and since the beginning of the year, a turnaround can be seen.

Government bonds

It is very likely that central banks will continue to raise key interest rates, but to a much lesser extent and at a slower pace than was the case in 2022. Falling inflation is the reason for this. Europe has slightly more room to tighten than the US. Market conditions for government bonds are generally favourable.

Our Conclusion: We are slightly positive on government bonds.

Investment grade bonds (IG)

Corporate bonds can cover a wide range of investors' risk appetite. The lower the issuer rating category, the higher the yield. Corporate bonds in EUR and USD with shorter maturities are now attractively valued again.

Our conclusion: We are neutral on investment grade bonds (IG) at the moment and favour bonds with short-term maturities.

High yield bonds (HY)

Default risk in HY bonds has risen in line with market developments. Volatility remains high and ratings could be lowered. This trend will continue this year.

Our conclusion: For HY bonds in a bond portfolio, investors are advised to focus on higher quality in the segment and shorter duration. We remain neutral.

Emerging Markets (EM) bonds

EM offer a yield premium for higher default and currency risk. This asset class is supported by robust fundamentals and the expectation of no severe recession. The higher coupons of this asset class may compensate the investor for the higher risk. EM bonds benefit from lower inflation in the US and easing pandemic policies in Asia.

Our conclusion: For riskier investors, we consider investments in EM Bonds denominated in hard currencies to be attractive. However, to reduce the risk of default, ETFs should be considered and credit quality should be closely monitored.

Mimi Haas, Lic. Rer.pol. HSG, M.A. in Banking and Finance HSG, Partner

Sources: MarketMap, Bloomberg and F&W

Currencies

Currencies continue to be a plaything of interest rates in 2023

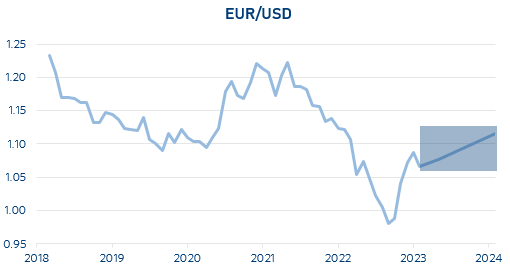

EUR/USD (20.02.2023: 1:07)

The USD has consolidated since the beginning of 2023. Higher than expected labour market figures in the US have reassessed policy rate expectations. The USD still has a higher interest rate advantage over the EURO. The legitimate question is to what extent this spread will be closed by the ECB rate hikes in 2023. This will influence the currency pair.

Our conclusion: We are cautious against the USD.

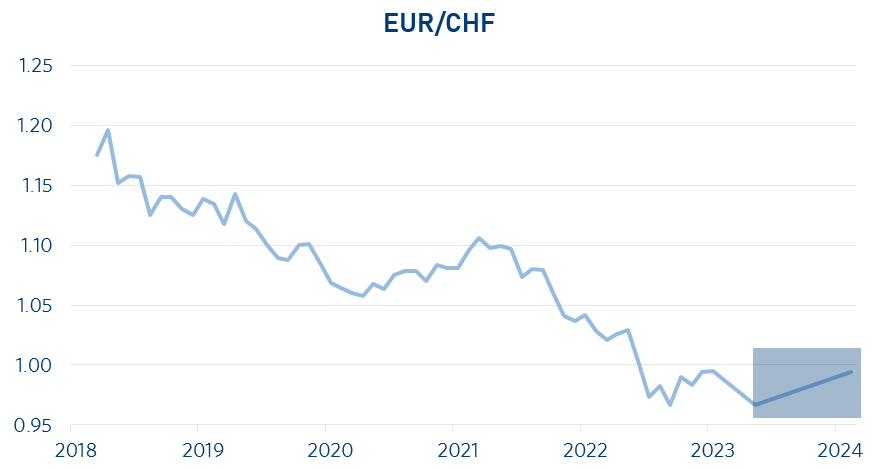

EUR/CHF (20.02.2023: 0.99)

The downward trend of the EUR against the CHF will not change in the medium term. Key interest rates in Switzerland were raised less than in the Euro area. The SNB is allowing the Swiss franc to strengthen because part of the fight against inflation is conducted via the exchange rate. The economic outlook in the Euro area has improved, but the inflation problem is still higher here, and thus there is a greater need to raise interest rates, with all that this entails for the currency.

Our conclusion: We expect a positive impulse for the CHF in the medium term.

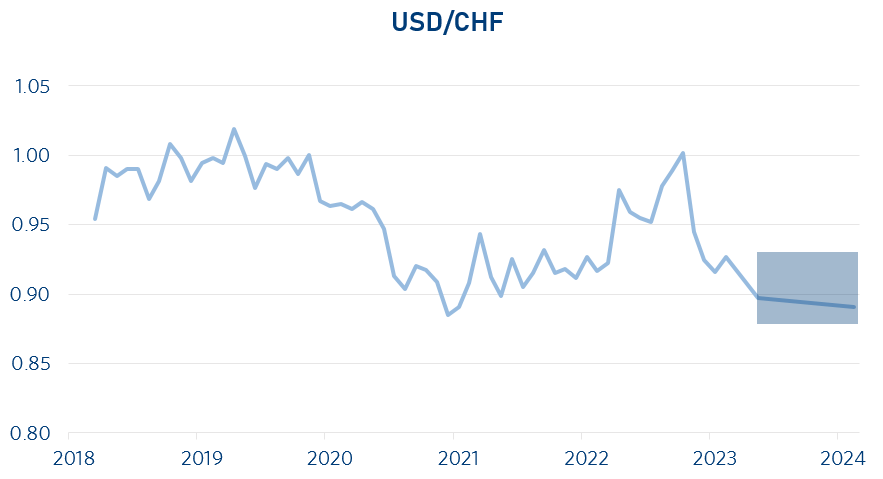

USD/CHF (20.02.2023: 0.92)

Since the SNB also controls inflation via exchange rates, it has sold less foreign currency than expected in recent months. Inflation in Switzerland is much more moderate. The interest rate spread between the US and Swiss key rates is high and will remain so in 2023.

Our conclusion: We expect the USD to move sideways against the CHF in the short and medium term, unless the Swiss National Bank changes its policy.

Mimi Haas, Lic. Rer.pol. HSG, M.A. in Banking and Finance HSG, Partner

Sources: F&W, Market Map and Bloomberg

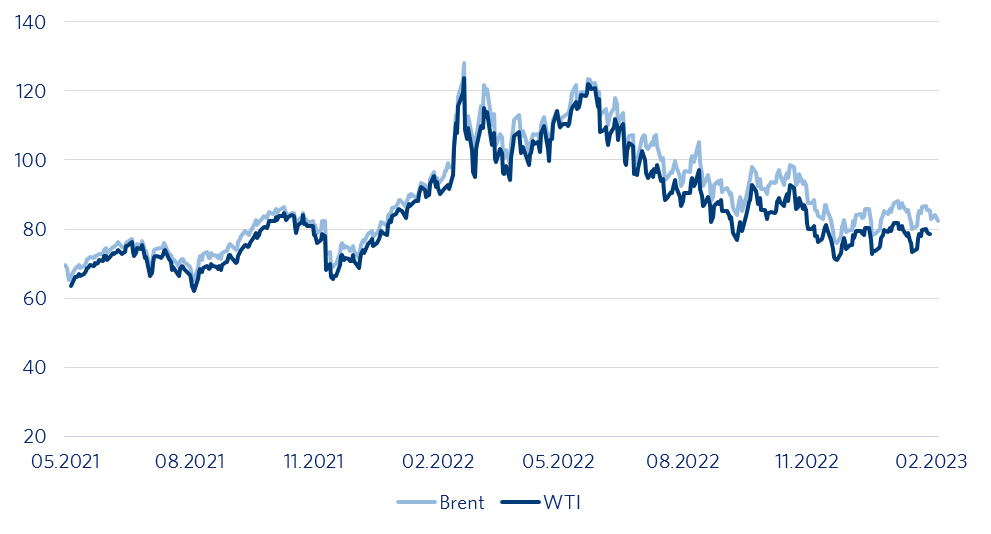

Oil

OPEC expect a bottleneck

Oil prices have moved sideways in recent weeks. The end of China's zero covid policy will increase oil demand. The International Energy Agency estimates that global oil demand will rise by 1.9 million barrels per day to 101.7 million barrels per day in 2023, thus slightly exceeding existing supply. According to OPEC+, however, the increased demand is not matched by sufficiently large reserve capacities. On the other hand, the (subdued) global economic growth of 2.90% for 2023 (IMF estimate) is having a dampening effect on demand and prices.

Our conclusion: We expect a continued sideways movement at prices around USD 80 per barrel of WTI oil

Dr. Patrick Huser, CEO

Source: F&W

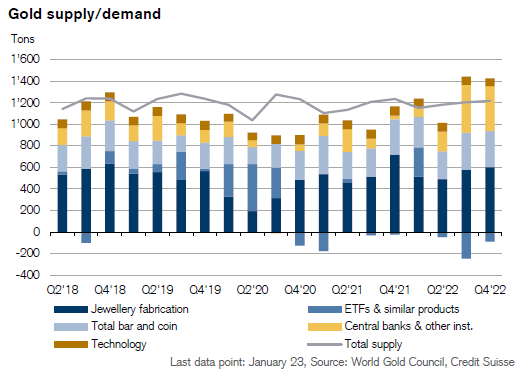

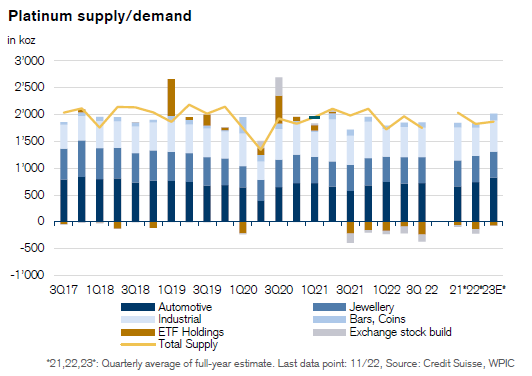

Precious Metals

Upward trend in gold and platinum

Gold is currently moving in a narrow price band slightly below USD 1,850 oz. Although continued high interest rates are dampening buying interest, a weaker US dollar and ongoing geopolitical problems are supporting the gold price.

The jewellery industry continues to be the biggest buyer of gold, but central banks also continue to stock up. Turkey alone was the largest buyer with almost 400 tonnes in 2022.

Platinum should continue to develop well in 2023 and remain in demand in the automotive industry as well as for jewellery production. Production will certainly continue to lag slightly behind demand in 2023, but should improve from 2024/25 onwards.

Our conclusion: Neutral

The ongoing geopolitical problems and the weak US dollar continue to leave room for gold and platinum as good diversification options in a balanced portfolio.

Andreas Betschart, Business Manager

Source: Credit Suisse

Abbreviations and explanations

bbl: 1 Barrell = 158,987294928 Litre

Bp: Basis points

GDP: Gross domestic products

BIZ: the Bank for International Settlements is an international financial organization. Membership is reserved for central banks or similar institutions.

EM-Bonds: Emerging market bonds. An emerging market is a country that is traditionally still counted as a developing country but no longer has its typical characteristics.

HY-Bonds: Fixed-income securities of poorer credit quality. They are rated BB+ or worse by the rating agencies.

IG-Bonds: Investment grade bonds are all bonds with a good to very good credit rating (Ra-ting). The investment grade range is defined as the rating classes AAA to BBB-.

IHS Markit: Listed data information services company

IWF: The International Monetary Fund (also known as the International Monetary Fund) is a legally, organiza-tionally, and financially independent specialized agency of the United Nations headquartered in the United States of America.

KOF: Business Cycle Research Centre at ETH Zurich

LIBOR: London Interbank Offered Rate is a reference interest rate determined in London on all banking days under certain conditions, which is used, among other things, as the basis for calculating the interest rate on loans.

OPEC: Organization of the Petroleum Exporting Countries

OPEC+: Cooperation with non-OPEC countries such as Russia, Kazakhstan, Mexico and Oman.

oz: the troy ounce is used for precious metals as a unit of measurement and is equal to 31.1034768 grams

Saron: The Swiss Average Rate Overnight is a reference interest rate for the Swiss franc

Seco: Swiss State Secretariat for Economic Affairs

Spread: Difference between two comparable economic variables

WTI: West Texas Intermediate. High-quality US crude oil grade with a low sulfur content.

Disclaimer:

The information and opinions have been produced by Chefinvest AG and are subject to change. The report is published for information purposes only and is neither an offer nor a solicitation to buy or sell any securities or a specific trading strategy in any jurisdiction. It has been prepared without regard to the objectives, financial situations or needs of any particular investor. Although the information is derived from sources that Chefinvest AG believes to be reliable, no representation is made that such information is accurate or complete. Chefinvest AG does not assume any liability for losses resulting from the use of this report. The prices and values of the investments described and the returns that may be received will fluctuate, rise or fall. Nothing in this report is legal, accounting or tax advice or a representation that any investment or strategy is appropriate to personal circumstances or a personal recommendation for specific investors. Foreign exchange rates and foreign currencies may adversely affect value, price or yield. Investments in emerging markets are speculative and involve considerably greater risk than investments in established markets. The risks are not necessarily limited to: Political and economic risks, as well as credit, currency and market risks. Chefinvest AG recommends investors to make an independent assessment of the specific financial risks as well as the legal, credit, tax and accounting consequences. Neither this document nor a copy of it may be sent in the United States and/or in Japan and they may not be handed over or shown to any American citizen. This document may not be reproduced in whole or in part without the permission of Chefinvest AG.