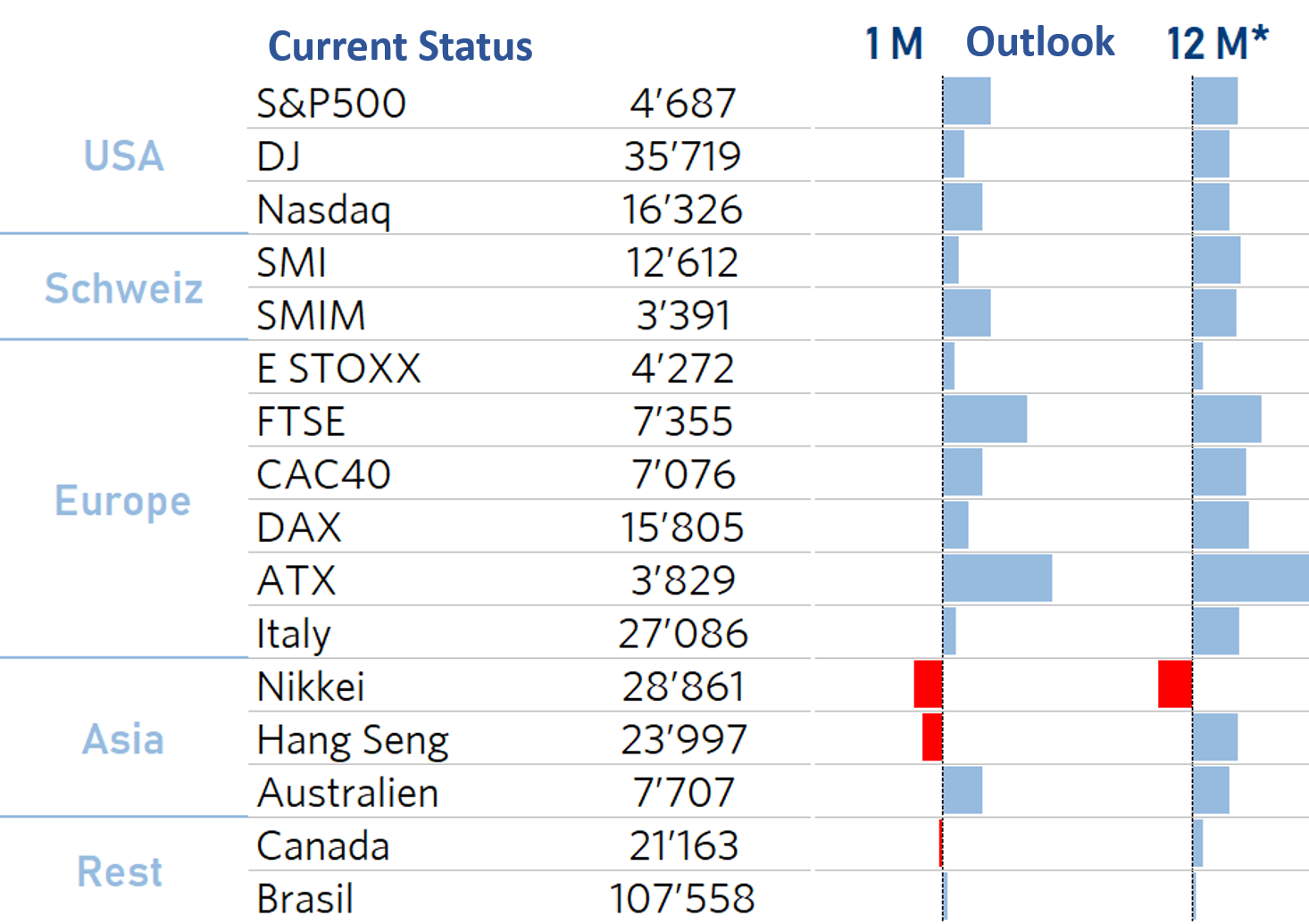

Click on the images to view our comments on each topic.

Switzerland

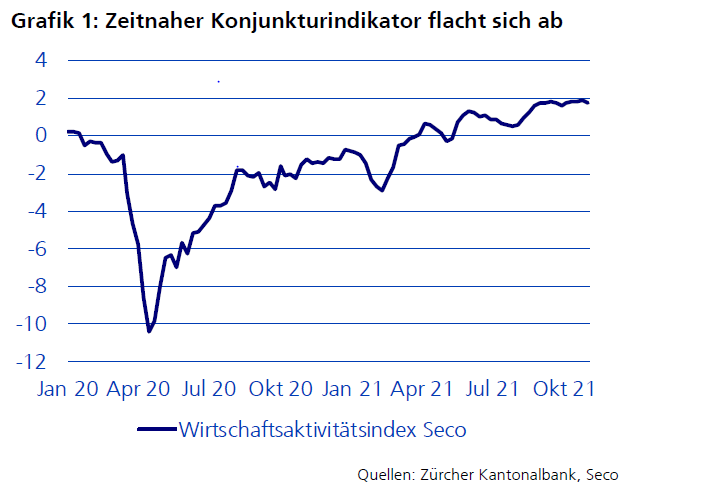

The CHF puts the brakes on inflation

In the 3rd quarter, the Swiss economy grew strongly, particularly with the private consumption accelerating. Export activity was at a considerable level in line with the encouraging global economic growth. SECO's economic activity index shows a flattening growth momentum for the final quarter of 2021. Nevertheless, according to estimates by various institutes, GDP growth is expected to remain well above the multi-year average of 1.6% in 2022. The biggest risk is the danger of another partial closure in connection with a next wave of the Corona virus. On the other hand, inflation, which has been rising since the beginning of the year, should not weigh on economic development in Switzerland.

Our Conclusion: The higher inflation seems to be controllable for the SNB. The clear differences to neighbouring countries can be explained. The average Swiss household consumes less energy from fossil fuels than a household in the EU. That is why the extreme price increases of coal and gas are not very noticeable. In addition, the strong Swiss franc inhibits import prices. The continuing good global economy, low unemployment and persistently low interest rates are a solid basis for further price increases on the local stock market.

Expected real GDP growth (IWF) 2021: 3.7%, Expected inflation (IWF) 2021: 0.4%, Current 3-month saron: -0.7%

As of: 7.12.2021, Source: Chefinvest AG, Zurich, Market Map

European Union

Europe defies inflation

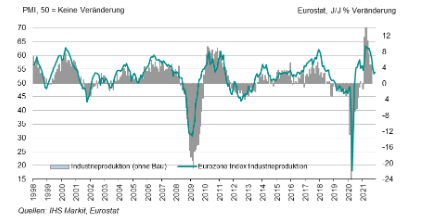

The EU Commission has slightly raised its growth forecast for the current year, whereby the further economic upswing depends on the course of the pandemic and inflation. According to the EU Commission's forecast, the economy in the European Union is recovering faster than expected. However, risk factors are new waves of corona infections, high energy prices and persistent supply chain bottlenecks. It has raised its growth forecast for this year to 5.0% from 4.8% in the forecast done in summer. For 2022, however, the Brussels-based authority is now forecasting 4.3%. In the summer, the forecast was 4.5%. After two quarters of strong growth of over 2%, GDP in the Eurozone is only half a percent below its pre-pandemic level. The inflation rate was 4.9% in November, the highest since the introduction of the euro. With an increase of 27.4% compared to the previous year, energy prices are the main drivers of inflation. Prices for services rose by 2.7%. At 2.6%, core inflation is significantly lower overall. The final IHS Markit Eurozone Composite Index (PMI) rose in November for the first time since June despite the difficult business conditions (delivery times) for industrial companies and currently stands at 58.3 points. Encouragingly, the consumer goods sector rose at an accelerated rate.

Daniel Beck, Mitglied der Geschäftsleitung, member of the board

Our Conclusion: The economic recovery in the euro area continues to be on a good track and the economic situation is generally perceived as positive. In the second and third quarter, the gradual lifting of coronary restrictions led to high growth rates (over 2% in both cases). Future growth rates will now be lower again and the government will reduce its support. The short-term outlook has deteriorated considerably due to the recent wave of pandemics, which has once again led to tighter restrictions. Encouragingly, however, the majority of leading and sentiment indicators for companies turned out to be better than expected. Companies Business Outlook is still optimistic. New orders continue to increase at an above-average rate, boosting order backlogs and triggering a strong employment surge. All this merely points to a temporary dip in growth and not an imminent downturn. ECB President Lagarde has repeatedly stressed that the ECB considers inflation to be only a temporary phenomenon. The inflation rate is expected to fall again as early as next year and an increase in key interest rates at the present time would not only be unnecessary but harmful. Interest rate hikes are not to be expected from the ECB in the foreseeable future. However, the ECB's securities purchases are likely to be successively reduced by the end of 2022. According to the EU Commission's forecast, the high inflationary pressure in the Eurozone will ease only slightly in 2022. For the current year it expects a rate of price increase of 2.4% and for 2022 of 2.2%. In 2023, price pressure is then expected to increase only moderately by 1.4%.

Expected real GDP growth (IMF) 2021: 5.0%, Expected inflation (IMF) 2021: 2.2%, Current 3-month Libor: -0. 6%

As of: 7.12.2021, Source: Chefinvest AG, Zurich, Market Map

United Kingdom

USA

Shut Down averted

S&P 500 companies Q3 2021 earnings and revenue figures beat expectations. While 75% beat sales expectations, the profit figure was an impressive 82%. After the record profit growth in 2021, growth rates are expected to return to normal in the mid-single digits in 2022.

Due to the persistently high inflation figures, the Fed is considering accelerating tapering, i.e. curbing securities purchases more quickly than previously planned, and ending the securities purchase programme as early as in spring rather than summer of 2022. The Fed is expected to announce this at the next meeting on 15.12.21. This would also allow the central bank to raise short-term interest rates earlier if needed. The market now expects three rate hikes in 2022. Inflation expectations are currently well anchored. This is not least because, on the one hand, supply chain bottlenecks due to the pandemic are seen as temporary and, on the other hand, there is sufficient production capacity to meet increased demand.

Although, contrary to expectations, only about 200,000 new jobs were created in November, the unemployment rate fell further from 4.6% to 4.2%. This brings it ever closer to the pre-Corona level of 3.5%.

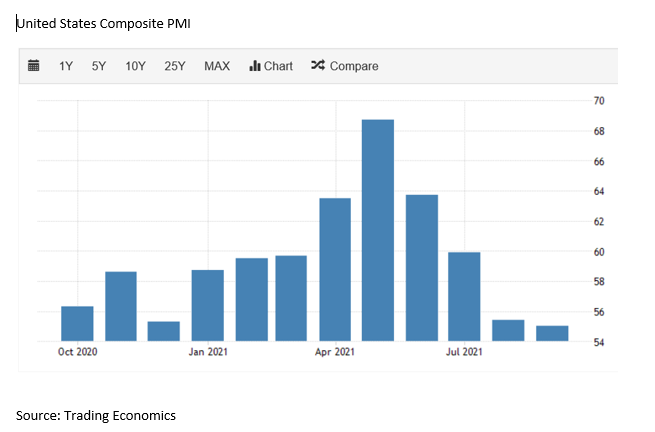

The composite PMI fell slightly from 57.6 in October to a still robust 57.2 in November. This was mainly due to supply chain problems and labour shortages.

The US Congress was able to avert a so-called 'shutdown' of the administration last week by passing another temporary funding package until February 18, 2022. For the time being, however, the debt limit increase that will become necessary in the course of December remains unresolved. The Senate is also eagerly awaiting the passage of the Biden administration's second (now slimmed-down) fiscal package (social and climate package) worth USD 1.75 trillion. The first fiscal package (infrastructure) in the amount of USD 1 trillion, which was passed a few weeks ago, will also have a positive impact on economic growth. Despite the supply bottlenecks, the IMF expects the US to grow by 6% in 2021 and to continue to expand strongly by 5.2% in 2022.

Our Conclusion: Due to the uncertainties surrounding the new Corona variant Omikron and the duration of higher inflation rates, higher volatility is to be expected. However, the outlook for the economy remains good and inflation expectations remain well anchored. We therefore remain positive on the US equity market as long as the economy is booming and medium to long-term inflation expectations remain low, corporate sales and earnings figures, and thus also the stock markets, should perform positively.

Expected real GDP (IWF) 2021: 6.0%, Expected Inflation (IWF) 2021: 4.3%, Current 3 month Libor: 1.3%

As of: 7.12.2021, Source: Chefinvest AG, Zurich,Market Map

China

The heavy hand of the state?

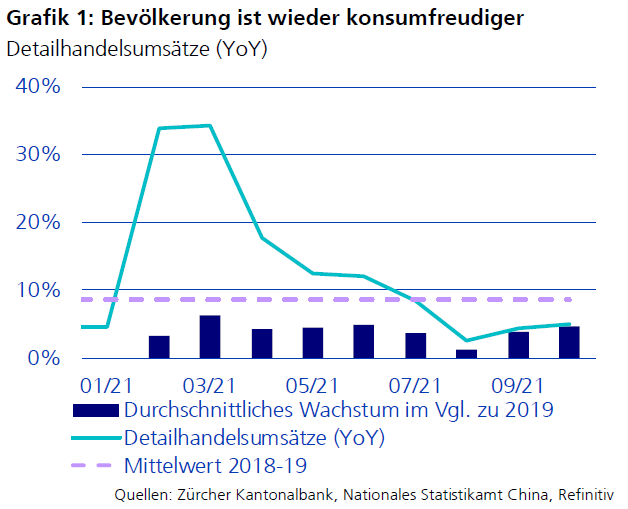

In the quarter under review, indicators suggest that the economy is recovering from the pandemic-related slowdown in Q3. Retail sales developed favourably. In addition, the energy shortage in October had less of an impact on industry than expected, so that GDP will rise by 8% in 2021. However, the ailing real estate market is likely to continue to weight on the economy for some time. The government is sticking to its restrictive course against highly indebted real estate developers. As a result, property prices have also already fallen. In general, a controlled slowdown in the growth of the real estate sector is being pursued, as evidenced by government instructions to lending banks. The government's handling of the large, listed technology companies is also a cause for concern.

Our Conclusion: Despite the expected fiscal stimuli and selective easing of monetary policy, as well as support measures in the real estate market, the economic forecasts are lowered. For 2022, the forecasts for GDP growth are a good 5%. Policy interventions in economic activity are increasing significantly, which is burdening companies listed in the USA in particular. The domestically listed companies (A-shares) developed more favourably.

Expected real GDP growth (IWF) 2021: 8.0%, Expected Inflation (IWF) 2021: 1.1%, Current 3Mts Shibor: 2.5%

As of: 7.12.2021, Source: Chefinvest AG, Zurich, Market Map

Japan

Dawn on the horizon

Also in Japan, the recent mutations of the coronavirus have influenced events across the board. The Japanese stock index has been moving in a band between 27,500 and 29,900 points in recent weeks, and has not yet found a clear trend. The new Prime Minister Kishida has been in the office for a few weeks and there have been some positive developments:

1. A fiscal policy programme was passed with the aim to support Japanese economy (about 30 trillion yen were spoken to support e.g. tourism and families with children). It is important for the economy and the country to continue with its low interest rate policy.

2. The yen is relatively weaker against the USD. This has a positive effect on exports and Japanese economy. Companies have been able to show positive earnings in the reporting season. In addition, more than half of the companies have a good liquidity/debt ratio. This is good for stock prices.

3. The job market in Japan has recovered well and is back to pre-Corona pandemic levels.

4. On the infection side, the country is also doing well, as they have very strict measures and good vaccination rates. This will have a positive impact on the recovery.

Mimi Haas, lic. rer. pol. HSG, M.A. in Banking and Finance HSG

Our Conclusion: Japan as an investment country in equities is interesting. The time to invest is still a bit too early, the trend needs to become clearer.

Expected real GDP growth (IWF) 2021: 2.4%, Expected Inflation (IWF) 2021: -0.2%, Current 3 Months Libor: -0.1%

As of: 7.12.2021, Source: Chefinvest AG, Zurich, Market Map

Emerging Markets

Risk on?

In recent weeks, numerous emerging markets have presented GDP growth rates for the third quarter. Asian countries suffered economic losses due to containment measures. Growth in Latin America and Eastern Europe was very strong, bringing the GDP of most economies back above 2019 levels. The IMF also expects a strong recovery in emerging Asia in the final quarter. The thriving economy, high commodity and energy prices are driving up inflation. Most central banks have already raised key interest rates and announced further steps. The Turkish central bank is acting in the opposite direction by continuously lowering interest rates. The Turkish lira is in free fall and has lost 70% against the USD since the beginning of the year, and inflation is getting out of control.

Our Conclusion: Most countries are developing well economically. The GDP growth rate forecast for 2022 is just under 5%, with Asian countries expected to outperform. Inflation and currency developments as well as rising debt rates and interest rates have unsettled equity investors until now. On the other hand, lower average equity valuations are now tempting. For investors willing to take risks, entry opportunities are opening up in the Asian emerging markets.

As of: 7.12.2021, Source:Chefinvest AG, Zurich, Market Map

Stocks

Is Powell letting go of the bear?

An explosive mix of a new viral variant and a more aggressive stance by the Fed on inflation, caused markets to fluctuate wildly again last week. It was extremely surprising to markets that Powell suddenly turned the Fed's attention to fighting inflation, even though Omikron had just begun its relentless global spread. The large-cap stocks were just barely keeping their heads above water in the market-weighted indices, thanks to high-quality companies with low valuations. However, 51% of the companies in the Russell 3000 are now trading in bear market territory. Growth stocks and especially companies trading at high valuations and lacking earnings, have been severely downgraded over the past two weeks.

The world regions performed differently: After a short stop, the considerable price corrections on the Chinese stock exchanges, as well as in Hong Kong, widened again and had a generally negative effect on the Asian markets. While the American markets remained almost unchanged in the reporting period, the French and English stock exchanges performed well as expected. At the sector level, energy stocks, financials and telecom stocks were downgraded.

In general, the CAIB shows an unchanged positive expectation for the coming months with an opportunity value of +0.15. The long-term value is even higher at +0.25. We recommend investors with an investment horizon of more than 12 months to buy equities. Should nominal interest rates rise above 2% next year, we expect equity sectors with a negative correlation to bond prices, as well as defensive quality and dividend stocks, to outperform.

Given current valuations, we do not see future returns being as high as in recent years. However, we do not equate this with a decline in equity prices, because when the Fed slows lending and funding the bond market, bond yields usually fall instead of rising. We expect future earnings increases and higher stock prices to coexist, even though the Fed's bond portfolio will shrink. We thus consider a gradual return to a new normal, which has taken a leap in time thanks to technologies, as likely. So the bear remains in the cage.

Preferred Trend: After the sharp corrections, we strategically recommend adding or further adding to equities in the growth areas of fintech, cybersecurity and clean energy.

As of: 7.12.2021, Source:Chefinvest AG, Zurich, Market Map

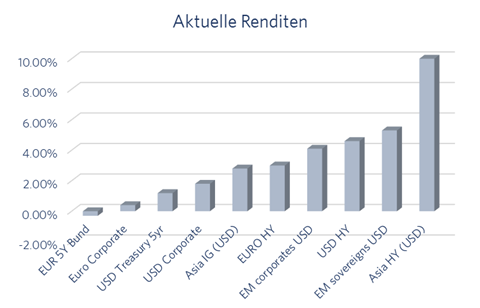

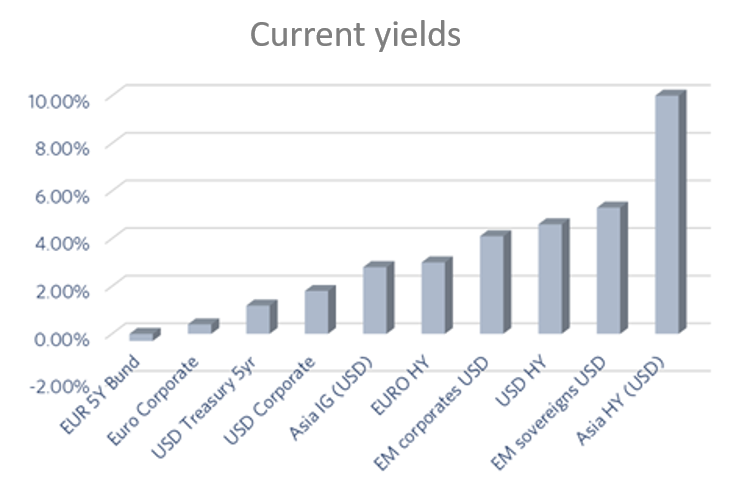

Interest

Turnaround in Asia

Government bonds

Continued fiscal policy support, vaccination programmes and the reopening of the economy in many regions will further strengthen the expected economic recovery. This should support long-term global yields. With real yields still very low, the favourable financing conditions could eventually lead to the gradual normalisation of monetary policy. If inflation remains higher than expected, the process could accelerate. After the Bank of England muted the rate hike, the UK yield curve moved down across maturities. US yields are already significantly higher than at the beginning of the year.

Our Conclusion: In the Eurozone and the Swiss franc, we remain in the short duration strategy. We expect an interest rate increase of 20 basis points in all hard currencies over 3 months. For this reason, we remain underweight in this asset class.

Investment-grade-bonds (IG)

Given the good fundamental picture, we do expect credit spreads to remain robust and narrow. However, at current levels, the buffer is too small to compensate for potential interest rate fluctuations.

Our Conclusion: After the recent broad-based sell-off in the Asian credit market, selected Asian IG bonds with shorter durations (6 years) - combined with Chinese BB stocks as a counterweight - may offer interesting opportunities. Given the current weakness in the primary market and rising default concerns, we prefer a defensive bias in the Asian credit market, despite the high yields. There could be opportunities for risk-tolerant investors.

High-Yield-bonds (HY)

High-yield credit spreads remain robust, supported by solid credit data, economic growth and the moderate default cycle. The assessment regarding low default rates is supported by low distress ratios and rating agency forecasts. However, current HY bond price spreads do not provide a sufficient buffer against interest rate fluctuations in Q4.

Our conclusion: Even though default risks exist and a fast, linear recovery of the Chinese real estate sector is not to be expected, the further downside potential of Asian spreads should be limited compared to the current elevated level. As the price spreads of Asian bonds in this asset class stabilise, the attractiveness increases due to high interest rates. We thus expect an improvement in Q1 2022.

Emerging-Markets-bonds (EM)

EM hard currency bond spreads stabilised in October. Fed tapering should not weigh on the asset class as much as in 2013, due to good Fed communication and improved EM external balances. However, in the environment of rising US interest rates, EM HW bonds do not offer an appealing risk-return ratio.

Maria Albericci, Chairman/Managing Director

Our Conclusion: Inflows into emerging market bond funds have returned in recent weeks, but inflation remains a short-term risk. Most emerging market central banks have adjusted their monetary policies to cushion the impact of price pressures on inflation expectations. We remain positive on this, as we were in our last forecast.

As of: 7.12.2021, Source:Chefinvest AG, Zurich, Market Map

Currencies

Advantage USD?

Currencies are currently in the playing field of economic policy and central banks. Currencies of countries that tighten monetary policy will appreciate against those of countries with loose policies.

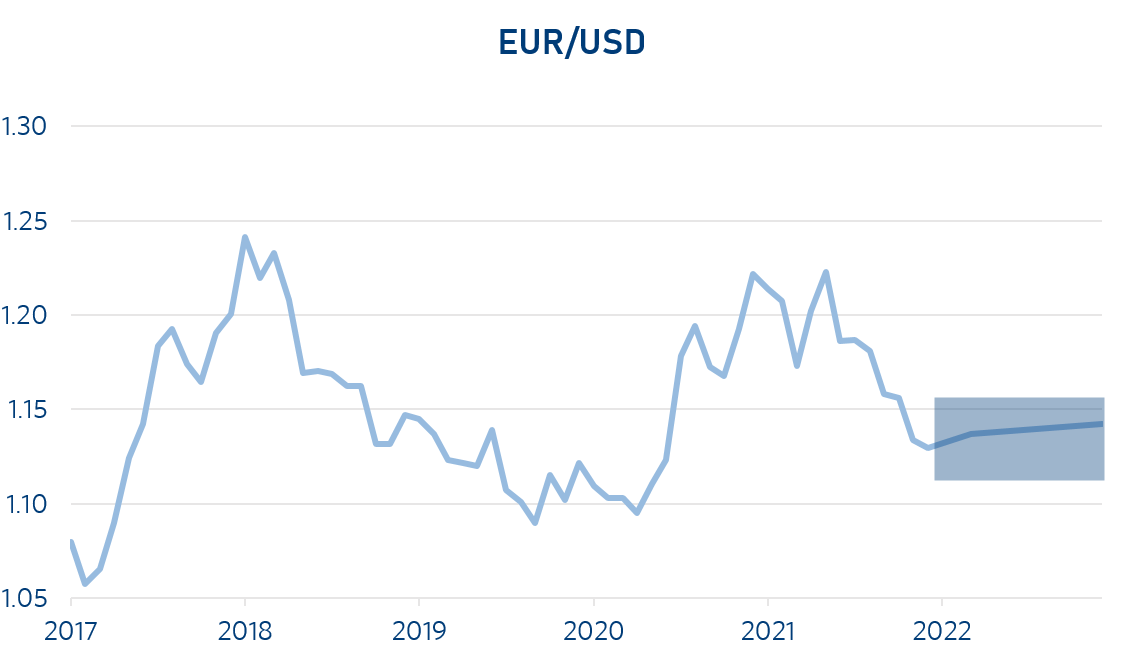

EUR/USD (Current 1.1266)

The euro continues to fall against the greenback. Due to the Fed's announced interest rate turnaround, the interest rate advantage of the dollar against the euro has continued to increase strongly. In chart terms, the resistance levels are at 1.1300, 1.1250 and 1.1200 and the support levels are at 1.1520, 1.1495 and 1.1300.

Our Conclusion: The expected interest rate differential continues to strengthen the dollar.

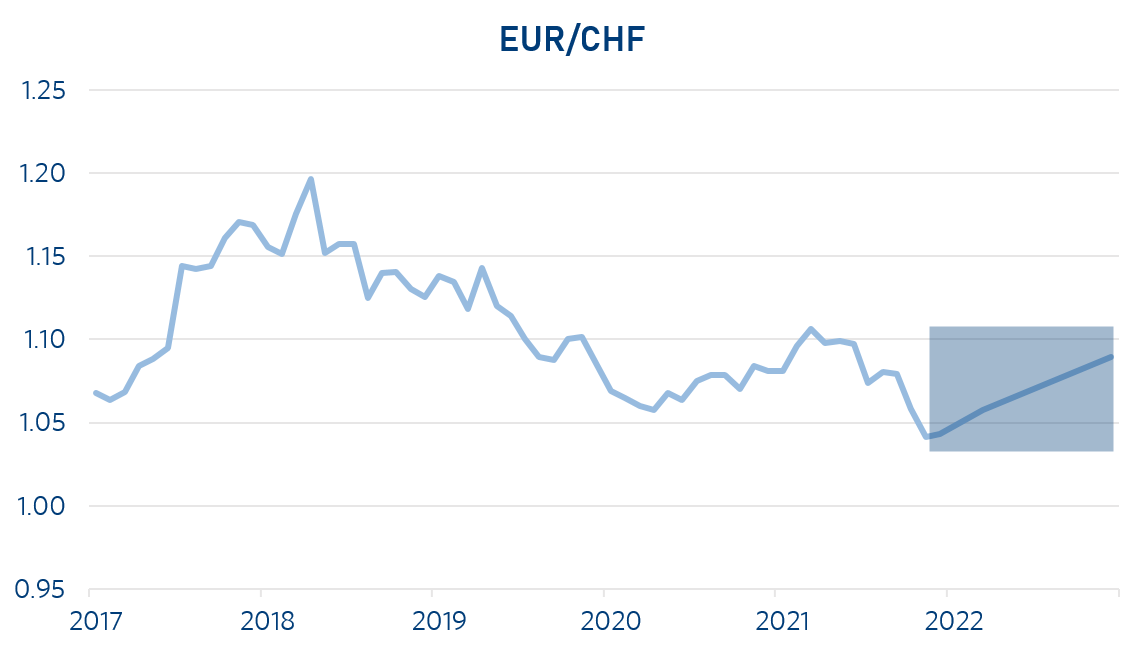

EUR/CHF (Current 1.0446)

The franc is influenced, as it has been many times before, by the monetary policy of foreign countries. The ECB will not raise key interest rates in 2022. The SNB has intervened more cautiously in the foreign exchange market this year. One reason for this is that the appreciation of the CHF is causing less damage to the economy as a whole than in the past. This is due to the lower inflation in Switzerland compared to other countries. The franc is therefore not super strong against all currencies, but primarily against the politically weakened euro. In chart terms, the resistance levels are at 1.0860, 1.0760 and 1.0690 and the support levels are at 1.0520, 1.0300 and 1.0230.

Our Conclusion: We expect a positive impulse for the CHF in the long term and the excursion below 1.05 against the euro could last longer.

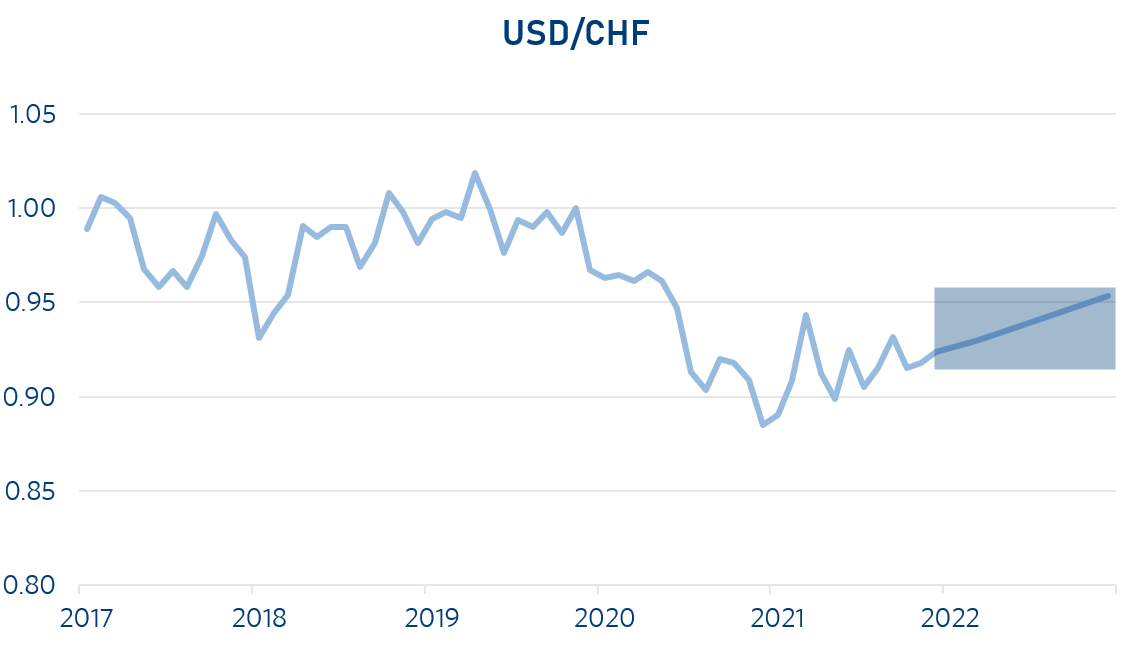

USD/CHF (Current 0.9247)

It appears that the Fed is deliberately strengthening the dollar. The reason is that this is the only way to fight goods inflation without endangering the stock markets or the economic recovery. The dollar also remains strong against the franc. In chart terms, resistance levels are at 0.9330, 0.9220 and 0.9170 and support levels are at 0.9090, 0.9020 and 0.8980.

Our Conclusion: We expect the USD to move sideways against the CHF in the short and medium term.

Mimi Haas, lic. rer. pol. HSG, M.A. in Banking and Finance HSG

As of: 7.12.2021, Source:Chefinvest AG, Zurich, Market Map

Oil

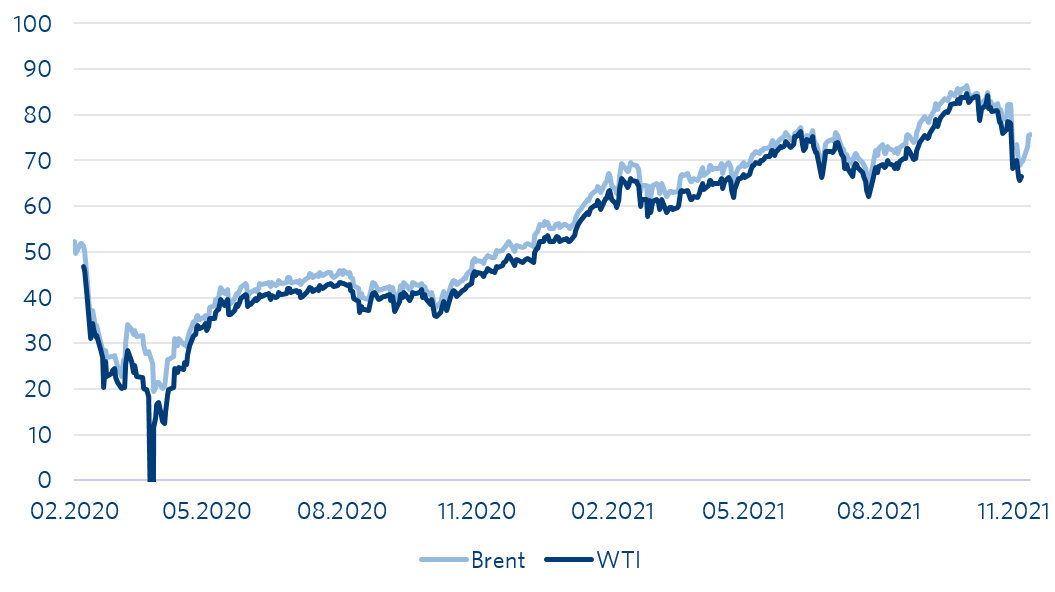

Omikron leverages OPEC+

Oil prices have corrected by 20% with the emergence of the Omikron variant of the coronavirus. The new coronavirus variant has thus achieved what the USA had unsuccessfully intended with the recent release of part of its strategic oil reserves (60 million barrels) coordinated with other countries. However, at its meeting at the beginning of December, OPEC+ decided to stick to its plan of monthly additional oil production of 400 million barrels per day for the time being.

Our Conclusion: As the recent oil price correction seems exaggerated to us, we expect WTI oil prices to stabilise at USD 70 per barrel and prices to rise slightly again in the coming months.

As of: 7.12.2021, Source:Chefinvest AG, Zurich, Market Map

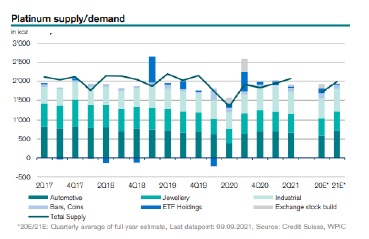

Precious Metals

A quiet turn of the year?

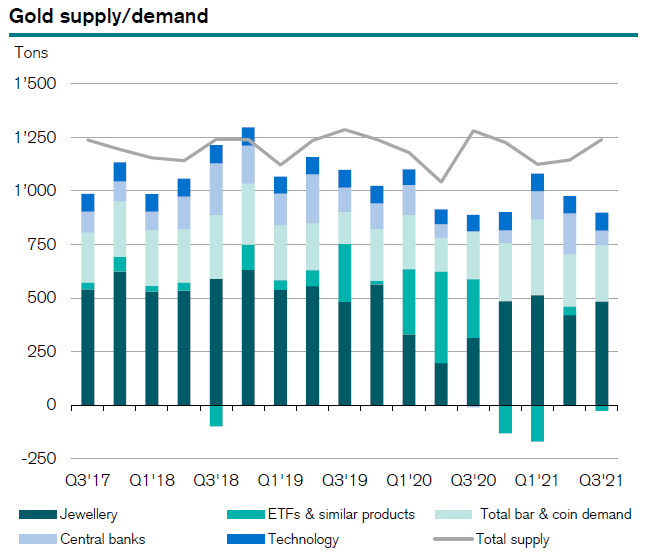

Rising Treasury yields and the policy of the Federal Reserve as well as the strength of the US dollar are lowering the appetite for investments in gold. The continuing uncertainties regarding inflation and the high Covid-19 case numbers including the Omicron mutation are not contributing to increased investment in gold at the moment.

The platinum price is stagnating due to a supply surplus and the prospect of declining diesel vehicle production in Europe. But the currently very high price of palladium makes platinum interesting again for catalytic converters in petrol engines, which could compensate for the overproduction of platinum from South Africa.

Andreas Betschart, Business Manager

Our Conclusion: At present we expect the gold price to move sideways. In the coming months, we continue to expect it to move in a range of USD 1,700 to 1,850 per ounce. For platinum, we forecast a range of USD 950 to 1'100 per ounce.

As of: 7.12.2021, Source:Chefinvest AG, Zurich, Market Map

Abbreviations and explanations

bbl: 1 Barrell = 158,987294928 Litre

Bp: Basis points

GDP: Gross domestic products

BIZ: the Bank for International Settlements is an international financial organization. Membership is reserved for central banks or similar institutions.

EM-Bonds: Emerging market bonds. An emerging market is a country that is traditionally still counted as a developing country but no longer has its typical characteristics.

HY-Bonds: Fixed-income securities of poorer credit quality. They are rated BB+ or worse by the rating agencies.

IG-Bonds: Investment grade bonds are all bonds with a good to very good credit rating (Ra-ting). The investment grade range is defined as the rating classes AAA to BBB-.

IHS Markit: Listed data information services company

IWF: The International Monetary Fund (also known as the International Monetary Fund) is a legally, organiza-tionally, and financially independent specialized agency of the United Nations headquartered in the United States of America.

KOF: Business Cycle Research Centre at ETH Zurich

LIBOR: London Interbank Offered Rate is a reference interest rate determined in London on all banking days under certain conditions, which is used, among other things, as the basis for calculating the interest rate on loans.

OPEC: Organization of the Petroleum Exporting Countries

OPEC+: Cooperation with non-OPEC countries such as Russia, Kazakhstan, Mexico and Oman.

oz: the troy ounce is used for precious metals as a unit of measurement and is equal to 31.1034768 grams

Saron: The Swiss Average Rate Overnight is a reference interest rate for the Swiss franc

Seco: Swiss State Secretariat for Economic Affairs

Spread: Difference between two comparable economic variables

WTI: West Texas Intermediate. High-quality US crude oil grade with a low sulfur content.

Disclaimer:

The information and opinions have been produced by Chefinvest AG and are subject to change. The report is published for information purposes only and is neither an offer nor a solicitation to buy or sell any securities or a specific trading strategy in any jurisdiction. It has been prepared without regard to the objectives, financial situations or needs of any particular investor. Although the information is derived from sources that Chefinvest AG believes to be reliable, no representation is made that such information is accurate or complete. Chefinvest AG does not assume any liability for losses resulting from the use of this report. The prices and values of the investments described and the returns that may be received will fluctuate, rise or fall. Nothing in this report is legal, accounting or tax advice or a representation that any investment or strategy is appropriate to personal circumstances or a personal recommendation for specific investors. Foreign exchange rates and foreign currencies may adversely affect value, price or yield. Investments in emerging markets are speculative and involve considerably greater risk than investments in established markets. The risks are not necessarily limited to: Political and economic risks, as well as credit, currency and market risks. Chefinvest AG recommends investors to make an independent assessment of the specific financial risks as well as the legal, credit, tax and accounting consequences. Neither this document nor a copy of it may be sent in the United States and/or in Japan and they may not be handed over or shown to any American citizen. This document may not be reproduced in whole or in part without the permission of Chefinvest AG.