Click on the images to view our comments on each topic.

Switzerland

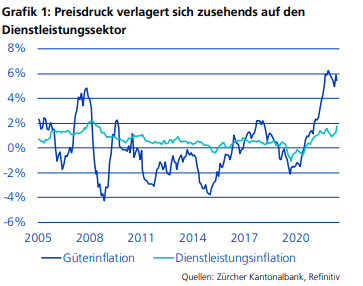

No all-clear for inflation

At 3.40%, inflation continued to rise in the first two months of the year, contrary to expectations, only to correct again rather surprisingly to 2.90% in March. The pressure on prices has increased across the board and has also become noticeable in the service sector. In mid-March, the SECO expert group raised the expected average annual inflation for 2023 from 2.20% to 2.40%. Economic growth was also slightly increased, somewhat surprisingly, from 1.00% to 1.10%. Supported by the good situation on the labour market and nominal wage increases, private consumption should rise moderately in the coming quarters. On the other hand, investment growth is expected to be below average in view of the international economic environment. As expected, the Swiss National Bank has raised the key interest rate by 50 basis points to 1.50% due to higher inflationary pressures and emphasised that further rate hikes may be necessary to ensure price stability. The SNB is likely to make another increase in June and then pause on interest rates. The labour market remains extremely robust and average unemployment is forecast at a record low 2.00% this year.

SECO economic forecast

GDP 2023: +1.10% (E)

Inflation 2023: +2.40% (E)

SNB interest rate: +1.50%

Our conclusion:

The latest economic data have been mostly encouraging. The collapse of Silicon Valley Bank led to turbulence in the global banking system in March. This was followed by the emergency takeover of Credit-Suisse by UBS. Markets have recovered somewhat from the negative headlines about the sector. The majority of published Q1 corporate results were positive and the outlook for the year was confirmed. The Swiss equity market is undervalued by historical standards and offers good long-term potential.

Sources: OECD and SECO

European Union

Resilient economy in a difficult environment

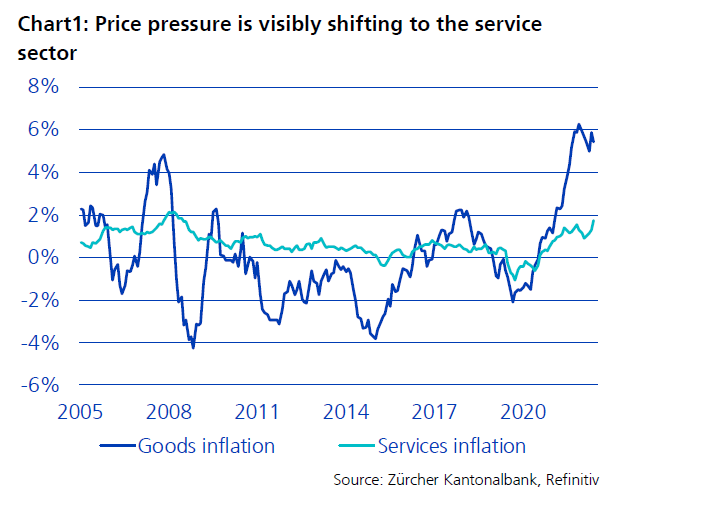

For Q1 2023, we expect the economy in Europe to be close to stagnation. Due to falling energy prices, following historical price peaks in Q3 2022, import costs for energy fell significantly, which supported foreign trade. In contrast, consumption and investment are weighing on growth.The EU labour market remains robust despite the economic slowdown. The average unemployment rate at the end of February was at an all-time low of 6.00% in the European Union (EU) and 6.60% in the Euro area. Germany, Poland and the Czech Republic have almost full employment with unemployment rates between 2.40% and 2.90%, while Spain has 12.80% registered as unemployed. Inflation in the Eurozone slowed significantly to 6.90% in March due to falling energy prices. In February it was still at 8.50% and last autumn over 10.50%, thus considerably higher. However, there is still no sign of an all-clear, as the core rate, which excludes volatile energy and food prices, continued to rise in March to a new record level of 5.70%. In March, the Eurozone recorded its strongest economic growth since May 2022 - a significant increase compared to the final quarter of 2022. The decisive growth impetus came from the services sector, while industrial production only increased minimally. The S&P Global Flash Eurozone Composite PMI stood at 53.70 points in March, up from 52.00 points in February and above the neutral mark of 50.00 points above which growth is indicated, for the third time in a row.

EU Inflation 2023: +4.60% (E)

Current 3 month Libor: +3.17%

GDP growth 2023: +1.00% (E)

Our Conclusion:

In the course of Q1 2023, the economy in the Euro area gained some momentum. We expect economic growth to be close to stagnation, followed by slight growth from the 2nd quarter onwards. With the recent turbulence in the global financial system, uncertainty for the global growth outlook has increased. In particular, declining inflation rates with lagging wage increases should support consumption. The development on the labour market with solid employment growth and a low unemployment rate as well as the leading indicators such as the purchasing managers' indices encourage us to be optimistic. This is contrasted by the restrictive financing conditions resulting from the restrictive course of the European Central Bank (ECB) and the associated rise in interest rates. The European Commission has raised its growth forecasts for 2023 to an average of 1.00% due to lower energy prices and the economy's greater resilience to the difficult environment. For 2024 and 2025, the ECB experts expect growth of 1.60%. At its March meeting, the ECB decided to raise the three key interest rates by 50 basis points each and to continue on its chosen path. The key interest rate for main refinancing operations now stands at 3.50%. Due to the recent turmoil in the banking sector, ECB President Lagarde stressed that the monetary guardians continue to operate on sight for the time being and did not present an interest rate outlook for the next meetings. The general expectation is that a quarter percentage point increase to 4.00% can be expected at the next two meetings. Headline inflation in the Euro area fell significantly in March to 6.90%, but is still far from the target of 2.00%. This confirms the trend reversal that has been apparent since the beginning of the year. However, core inflation rose to 5.70%, which shows that the fight against inflation has not yet been won. The food category alone contributed a good 3.00% to March inflation. The ECB expects inflation to average 4.60% in 2023. According to forecasts, it will fall to 2.50% in 2024 and to 2.20% in 2025.

Daniel Beck, Member of the Executive Board

Source: European Commission, Statista and S&P Global

United Kingdom

USA

Inflation continues to fall

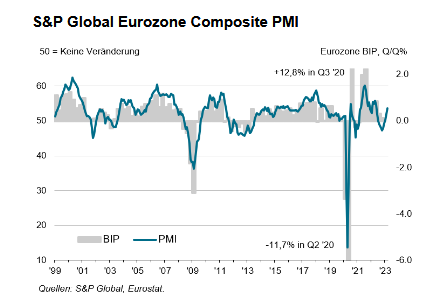

According to Markit Economics, the S&P Global US Composite PMI reached a value of 52.30 points in March (in February it was still at 50.10). This improvement was mainly due to the services sector, which rose from 50.60 to 52.60 points in March compared to the previous month. The manufacturing sector also increased in this period, but remained below the expansion threshold of 50.00 at 49.20 points. The 3 to 6 month leading economic index thus indicates expanding economic activity again, despite the sharp interest rate hikes. According to its April forecasts, the International Monetary Fund (IMF) now expects the US economy to grow by 1.60% (+ 0.20% compared to its January forecast) this year and by 1.10% next year. It warns that global growth rates could also be below average in the coming years. Inflation fell further in January to 5.00% (February 6.00%). The core rate (excluding food and energy), on the other hand, rose slightly in March from 5.50% to 5.60%. Almost half of this core inflation is due to rental costs. However, the 3-month average of core inflation, extrapolated to a year, also indicates an easing of inflationary pressure.The seasonally adjusted unemployment rate in March was a low of 3.50% (February 3.60%). The expected slowdown in job creation (excluding agriculture) occurred in March. There were still 236,000 new jobs created. The increase is still robust, but much lower than in January (+472,000) and February (+326,000). This has lowered market expectations of further interest rate hikes by the Fed. The central bank is expected to make a final rate hike of 0.25% to 5.25% at its next meeting on May 3rd, 2023. In 2023, earnings growth of 0.90% and revenue growth of 2.10% is expected for the S&P 500 companies. Negative (earnings) or slightly positive (sales) rates are expected for the first two quarters and positive rates again for the last two quarters. According to FactSet, the price/earnings ratio of the S&P 500, based on expected 2023 corporate earnings, is 18.30, slightly below the 5-year average of 18.50 and above the 10-year average of 17.30. The turbulence in the financial sector has subsided again. This is also evidenced by the fact that the Fed's discount window and its Bank Term Funding Programme, which was created in March, are being used less by banks again. However, the banks' reluctance to lend to the private sector could weaken economic growth. We expect that despite a possible 'showdown' between the Republicans and Democrats in the US Congress on raising the debt ceiling, a corresponding decision will be taken by June.

GDP 2023 (IMF): +1.60% (E)

Inflation 2023 (SPF): +4.50% (E)

Fed Fund Rate: +5.00%

Our Conclusion:

The probability of a soft landing has increased again. As inflation rates continue to decline, the Fed will have more leeway in the second half of the year to lower interest rates again - if necessary. Rising corporate profits will have a positive impact on equity valuations in the medium term, while higher interest rates are still a headwind in the short term.

Sources: Markit Economics, IMF World Economic Outlook April 2023, FactSet

China

Economy on the rise

The economic recovery is being driven in particular by catch-up effects in contact-related services. Retailers are recording an increase in turnover for the first time since autumn. Targeted government measures have continued to stabilise the faltering real estate sector. Prices for new buildings have already picked up again. Better financing conditions and renewed demand are encouraging real estate developers to push ahead with new projects and investments. The Purchasing Managers' Index for the service sector, compiled by the private survey institute Caixin, unexpectedly rose strongly in March. The PMI rose from 55.00 to 57.80 points, the highest reading since the end of 2020, and the index is now well above the 50.00 growth threshold for the 3rd consecutive month since the zero-tolerance approach to the virus was lifted. Businesses remain optimistic about the months ahead. The PMI Composite, which combines the industrial and services sectors, rose from 54.20 to 54.50 points in March, signalling a continued recovery. Last month, the National People's Congress (NPC) set the stage for increasingly open competition between China and the US. Xi Jinping was officially confirmed for a third term as president of the People's Republic. It is about power and influence, but also about security policy in the military and civilian spheres, including energy security. China wants to find a new balance between globally interconnected supply chains and less dependence on other countries for critical technologies.

IMF Economic Forecast

GDP 2023: +5.20% (E)

Inflation 2023: +2.00% (E)

3 Month Shibor: +2.42% (E)

Our conclusion:

The Chinese service sector is currently recovering rapidly from the drastic virus containment measures of previous years. Thanks to major catch-up effects, we expect the recovery to continue in the coming months. The government has set a feasible economic growth target of 5.00%. International political risks have increased significantly, which is why we do not recommend direct investments in China. We prefer Western companies that will benefit from China's reopening.

Sources: IMF and LLB

Japan

Recent developments in Asia positive

Unfortunately, this year is starting again with some hefty price increases. Numerous manufacturers have announced that several thousand products will become more expensive - quite a few of these products were already made more expensive last year. Most affected are flour and flour products, as well as coffee, gas, paper goods, electricity and even public transport tickets. In other words: No one can avoid it. A cold winter so far is also causing fruit and vegetable prices to rise. In short, Japan is also struggling with inflation. So far, the Bank of Japan has stuck to its policy of negative interest rates and the new candidate for the post at the Bank of Japan is not worried. But there are voices in the market that we will see the first interest rate hikes this year. The JPY is expected to appreciate. The combination of monetary policy normalisation and mild inflation may give the stock market a decent boost. As real interest rates are likely to remain negative, this means a boost to economic growth and corporate earnings will be positive. Companies are well endowed with liquidity.

GDP 2023: +1.70% (E)

Inflation 2023: +1.40% (E)

3 Month Tona Rate: -0.03% (E)

Our conclusion: Positive

Japan is still undervalued and underrepresented in portfolios. The market offers a good opportunity for medium-term investors.

Mimi Haas, Lic.rer.pol. HSG, M.A. in Banking and Finance HSG, Partner

Sources: F&W, JP Morgan and Bloomberg

Emerging Markets

Macroeconomy improves

Supported by the economic expansion in China, demand should pick up in the emerging markets. The highest growth rates are expected in Asian countries, led by China, Korea and Thailand, while Latin American countries are lagging behind in economic growth. Recent corporate results show a recovery in earnings. Equity market valuations are fair by historical standards. Key risks include a further increase in US interest rates, a strong USD and a significant escalation of geopolitical tensions. A recession in the US was a much bigger risk for emerging equity markets in previous decades than it is today. In recent years, dependence on the US economy has been reduced, but China's share has grown strongly. The share of Chinese stocks in the MSCI Emerging Market Index now accounts for one third of the market capitalisation.

Our conclusion:

At the moment, we prefer investments in Western equity markets, which are also benefiting from the economic recovery in the emerging markets.

Sources: IMF and LLB

Stocks

The Sleeping Beauty approach is out

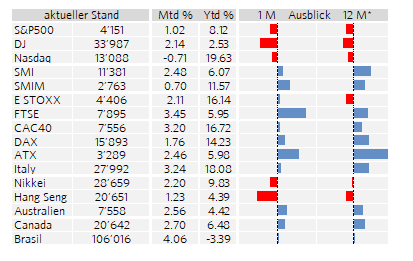

Most equity markets held their ground during the month of March, despite high volatility, and ended the quarter with a positive performance. Defensive and interest rate-sensitive equity sectors, such as non-cyclical consumer goods or the IT sector, were among the winners, while financial stocks lost a lot of value. Thus, the uncertainties surrounding Silicon Valley Bank led to a money run, especially in the USA, and several billion dollars in deposits were withdrawn from American custodian banks: Deposits at the depository bank State Street and the regional bank M&T Bank both fell by 3.00%, while deposits at Charles Schwab dropped by 11.00% compared to the previous quarter. For the current year, the latest outlook points to subdued growth in the global economy amid persistent pressure from core inflation. Nevertheless, the International Monetary Fund's economic forecast of 2.80% growth for 2023 was a positive surprise. This is because it is becoming increasingly visible that the Fed's aggressive interest rate hike policy is causing skid marks in the economy and cracks in the financial system in the fight against primarily supply-side driven inflation risks. The fear of interest rates continuing to rise globally is also pushing the surprisingly good Chinese economic growth of 4.50% in the first quarter into the background and has hardly been appreciated on the Chinese stock markets this year. Only Japan escaped this interest rate pressure: Here, the commitment of the new Japanese central bank governor Kazuo Ueda to further low interest rates provides support. Due to unexpectedly strong US economic data, interest rate speculation has slowed demand for US equities. In addition, analysts are rather pessimistic about the business figures for US companies and are expecting another quarter of declining profits for the S&P 500 companies in total.

Our conclusion:

Even if things remain somewhat turbulent in the short term, we are still positive for the equity markets! Most economies around the globe are still on course for growth. The recent further rise in leading and sentiment indicators even signals a revival. Pessimism is therefore out of place. However, as is well known, a restrictive monetary policy only affects the real economy with a delay of several months. Against this background, caution is therefore still advisable in investment policy, especially since the effects of the banking turmoil and the associated worsening economic outlook have so far only had a limited impact on the stock markets. Looking ahead over the next 12 months, however, we remain positive on the European stock markets in particular. Based on our valuation tool (CAIB), we continue to assess the risk/reward ratio in Europe as attractive. The continental European stock markets still have a significantly lower valuation than the US stock markets. But Swiss equities are also attractive and could surprise, especially in the second half of the year. The current supply factors and production constraints are causing an increasingly visible reorganisation of world trade and geo-economic block formations. A shrinking labour force or the green transformation of the economy are also leading to a change in existing market relationships and competitive positions of enterprises. This calls for a reassessment of the portfolio composition that has been conventional practice until now.

The traditional "Sleeping Beauty" investment approach ("buy and forget") is increasingly giving way to a more dynamic and flexible handling of the equity portfolio. The company's ability to adapt to rapidly changing conditions ultimately determines their stock market value. Trends play a major role in this: find out more about our Trendinvest Approach!

Sources: S&P, Citigroup, MarketMap, IMF, and Chefinvest

Interest

Paradigm shift

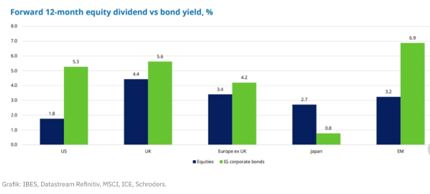

The phenomenon of the two main asset classes moving in parallel continued in 2023. Share prices rose and fell, yield curves moved analogously and volatility has increased. This development can be observed in the following months. Together with continued growth, e.g. in the labour market and the service sector, inflation has been stronger than expected. Key interest rates have been raised longer and higher than expected at the beginning, but it can still be assumed that the peak of interest rate hikes has been reached within 2023 and that the financial markets are pricing in the final level. Bond yields are again higher than dividend yields, with one exception in Japan. Here, an alternative has opened up for investors in recent months.

Government bonds

Economic data and inflation have surprised with their strength. Markets have reassessed risks and the yield curve has steepened overall and the peak of policy rates has shifted, yet we see this process coming to an end. This is highly likely to occur first in the US.

Our conclusion: We are rather positive on global government bonds and prefer US Treasuries.

Investment grade bonds (IG)

Corporate bonds can cover a wide range of investors' risk appetite, depending on the issuing company and its figures and rating. Investors can again generate good returns with high-quality bonds in USD and EUR.

Our conclusion: We are positive on investment grade bonds (IG) and favour them with shorter maturities.

High yield bonds (HY)

The main risk for the bond market at the moment is an economic slump. HY bonds are particularly affected. The default risk for HY bonds has increased with the market development and there is a risk of a further rating downgrade. The higher coupons do not compensate for this additional risk.

Our conclusion: We recommend avoiding this segment in the coming months.

Emerging Markets (EM) bonds

EM bonds offer a yield premium for higher default and currency risk. Robust fundamentals and the expectation that there will not be a severe recession support this asset class. The higher coupons of this asset class compensate the investor for the higher risk. The coupons are around 8%, which is well above global inflation levels. EM bonds are benefiting from the expectation that there will not be a deep recession and from the easing of pandemic policy in Asia.

Our conclusion: We consider it attractive for riskier investors to invest in EM in hard currencies. To reduce the risk of default, ETFs should be considered and credit quality closely scrutinised.

Mimi Haas, Lic.rer.pol. HSG, M.A. in Banking and Finance HSG, Partner

Sources: MarketMap, Bloomberg and F&W

Currencies

Still a pawn in the politics of national banks in 2023

Although the importance of the US in the world economy is declining, the dollar continues to meet the criteria of a reserve currency. To be a reserve currency, a currency must be fully exchangeable into other currencies. This currency is globally dominant as a foreign exchange reserve, transaction, invoicing and also investment and issuing currency. The USD has all these characteristics and thus dominates over many other currencies and there are clear advantages for the USA associated with it. Among other things, it realises considerable money creation profits as the issuer of the world currency. There is always criticism of this, which is mainly political.

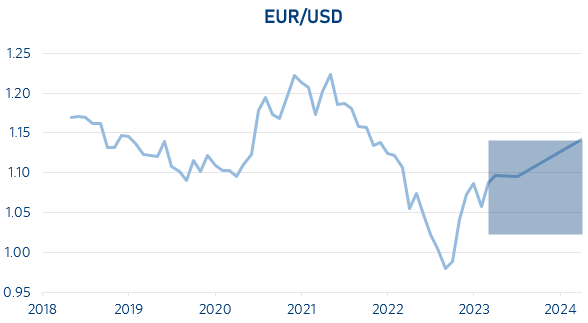

EUR/USD (18.04.2023: 1.10)

The USD has continued to recover some of the losses from 2022 since the beginning of the year. The current economic data from the US continues to be good. The FED has continued to raise US key interest rates despite turbulence in the financial market and has put it in place to continue to do so in order to fight inflation. The ECB has also experienced this phenomenon, but key interest rates in Europe are significantly lower than in the USA.

Our conclusion: We expect the currency pair to settle and find its level around 1.05.

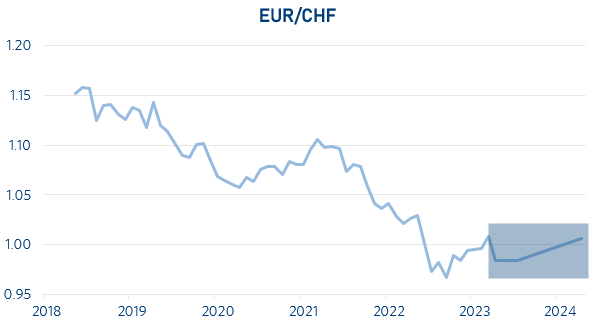

EUR/CHF (18.04.2023: 0.98)

In the Eurozone, the economic outlook has improved recently, but we still rate the CHF positively against the EUR. Although higher inflation in Switzerland is causing the SNB to raise interest rates further (the key rate is now expected to be 2.25%), the ECB has to fight much higher inflation with its rate hikes and the key rate in the Euro area is significantly higher than in Switzerland. Moreover, the SNB is prepared to intervene in the market with further monetary policy interventions.

Our conclusion: We continue to expect a positive impulse for the CHF.

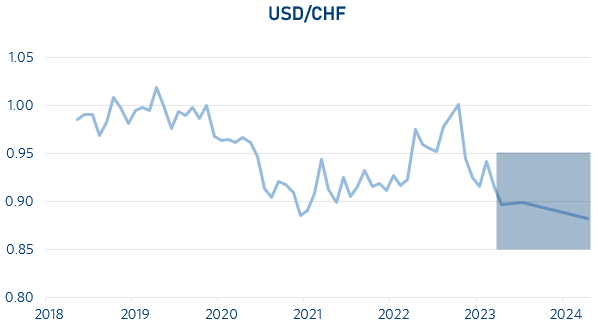

USD/CHF (18.04.2023: 0.89)

Inflation in Switzerland also rose in the first quarter of 2023, but nevertheless much more moderately than in the USA. The reasons for this are that the SNB did not push economic stimulation too excessively during the pandemic, unlike the USA and the Eurozone. As a result, there was also no completely excessive inflation of the money supply or monetary liquidity in Switzerland as in many other countries. This means that Switzerland has caused far fewer inflation drivers in 2020 and 2021 than the Eurozone and the USA. The interest rate spread between the US and Swiss key interest rates is high and will remain so in 2023.

Our conclusion: We expect the USD to move sideways against the CHF unless the Swiss National Bank changes its policy.

Mimi Haas, Lic.rer.pol. HSG, M.A. in Banking and Finance HSG, Partner

Sources: MarketMap, Bloomberg and F&W

Oil

OPEC further cuts production

After oil prices retreated towards USD 70.00 per barrel in March, they rose slightly above USD 80.00 per barrel again in April. Due to the falling prices, OPEC+ surprisingly cut oil production by another 1.16 million barrels per day at the beginning of April. With this measure, it is protecting its (short-term) interests. For the global efforts (above all those of the USA and Europe) to fight inflation, this step - since it is counterproductive - seems like an affront. In the long run, this measure - if implemented - could prove to be a boomerang for OPEC+.

Our Conclusion:

We continue to expect a sustained sideways movement at prices around USD 80.00 per barrel of WTI oil.

Sources: F&W, MarketMap

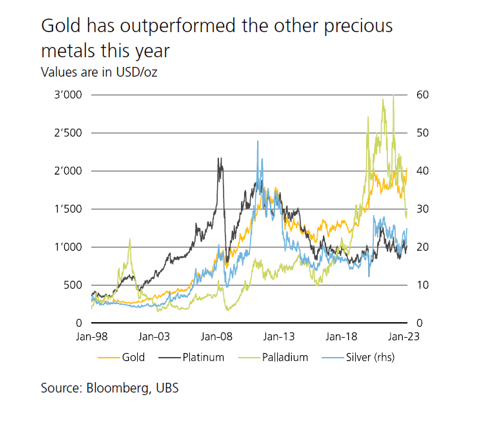

Precious Metals

Upward trend confirmed

The gold price was able to rise above the USD 2,000/oz. mark due to the banking crisis and has also broken through it several times and is holding slightly above it. This is a sign that the interest rate hikes could be coming to an end, but the uncertainties regarding recession will continue. Gold has held up very well against other precious metals in 2023 (see chart). Platinum can maintain its market position, as it is used as an alternative to palladium by catalytic converter manufacturers and will also be needed for the production of fuel cells after 2035.

Our Counclusion: Neutral

The ongoing geopolitical and banking problems continue to give gold and platinum a diversifying place in a balanced portfolio.

Andreas Betschart, Business Manager

Sources: UBS, Bloomberg

Abbreviations and explanations

bbl: 1 Barrell = 158,987294928 Litre

Bp: Basis points

GDP: Gross domestic products

BIZ: the Bank for International Settlements is an international financial organization. Membership is reserved for central banks or similar institutions.

EM-Bonds: Emerging market bonds. An emerging market is a country that is traditionally still counted as a developing country but no longer has its typical characteristics.

HY-Bonds: Fixed-income securities of poorer credit quality. They are rated BB+ or worse by the rating agencies.

IG-Bonds: Investment grade bonds are all bonds with a good to very good credit rating (Ra-ting). The investment grade range is defined as the rating classes AAA to BBB-.

IHS Markit: Listed data information services company

IWF: The International Monetary Fund (also known as the International Monetary Fund) is a legally, organiza-tionally, and financially independent specialized agency of the United Nations headquartered in the United States of America.

KOF: Business Cycle Research Centre at ETH Zurich

LIBOR: London Interbank Offered Rate is a reference interest rate determined in London on all banking days under certain conditions, which is used, among other things, as the basis for calculating the interest rate on loans.

OPEC: Organization of the Petroleum Exporting Countries

OPEC+: Cooperation with non-OPEC countries such as Russia, Kazakhstan, Mexico and Oman.

oz: the troy ounce is used for precious metals as a unit of measurement and is equal to 31.1034768 grams

Saron: The Swiss Average Rate Overnight is a reference interest rate for the Swiss franc

Seco: Swiss State Secretariat for Economic Affairs

Spread: Difference between two comparable economic variables

WTI: West Texas Intermediate. High-quality US crude oil grade with a low sulfur content.

Disclaimer:

The information and opinions have been produced by Chefinvest AG and are subject to change. The report is published for information purposes only and is neither an offer nor a solicitation to buy or sell any securities or a specific trading strategy in any jurisdiction. It has been prepared without regard to the objectives, financial situations or needs of any particular investor. Although the information is derived from sources that Chefinvest AG believes to be reliable, no representation is made that such information is accurate or complete. Chefinvest AG does not assume any liability for losses resulting from the use of this report. The prices and values of the investments described and the returns that may be received will fluctuate, rise or fall. Nothing in this report is legal, accounting or tax advice or a representation that any investment or strategy is appropriate to personal circumstances or a personal recommendation for specific investors. Foreign exchange rates and foreign currencies may adversely affect value, price or yield. Investments in emerging markets are speculative and involve considerably greater risk than investments in established markets. The risks are not necessarily limited to: Political and economic risks, as well as credit, currency and market risks. Chefinvest AG recommends investors to make an independent assessment of the specific financial risks as well as the legal, credit, tax and accounting consequences. Neither this document nor a copy of it may be sent in the United States and/or in Japan and they may not be handed over or shown to any American citizen. This document may not be reproduced in whole or in part without the permission of Chefinvest AG.